Secured Loan With Collateral

Description

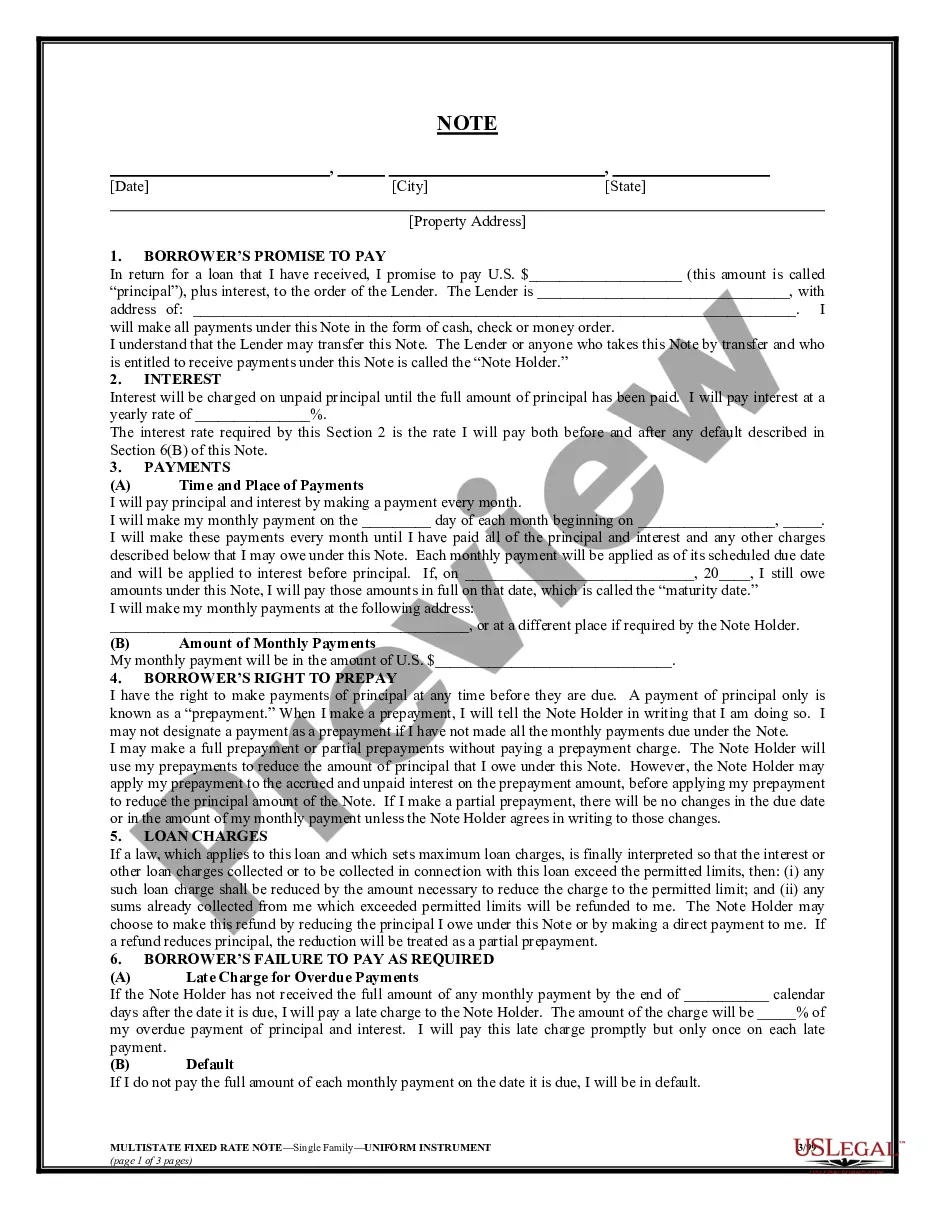

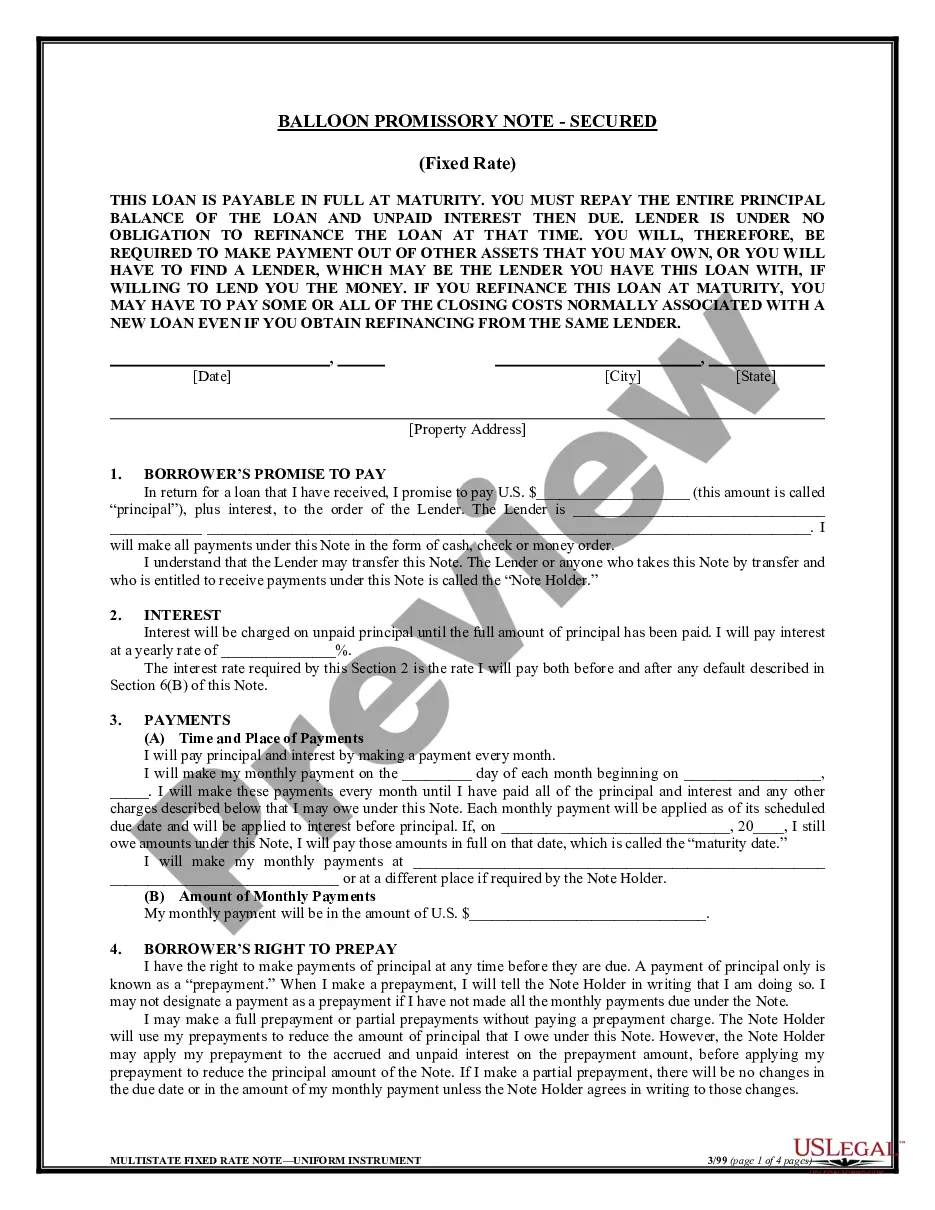

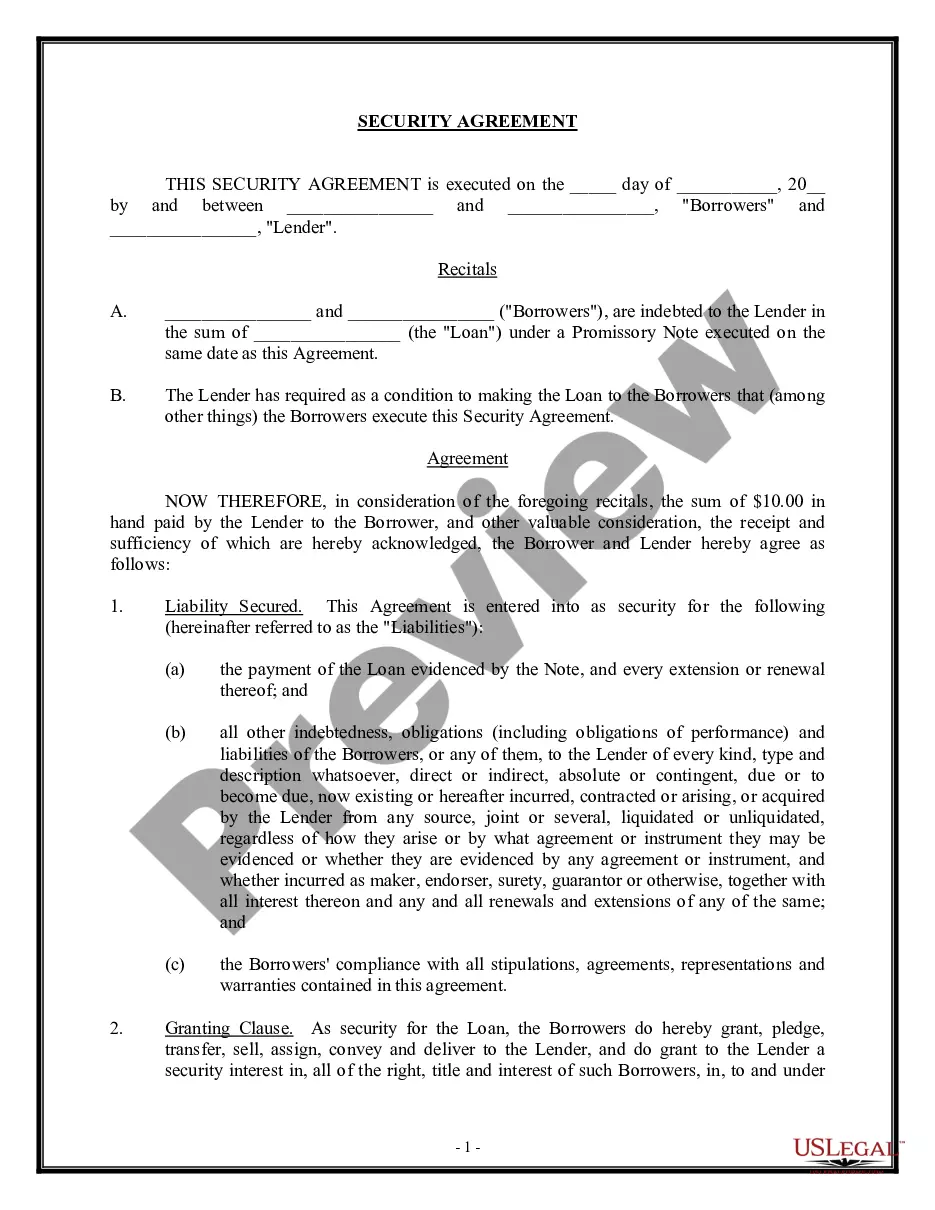

How to fill out Secured Promissory Note?

Creating legal documents from the ground up can frequently be daunting.

Certain situations may require extensive research and considerable financial investment.

If you're seeking a more straightforward and economical method of producing Secured Loan With Collateral or any other forms without unnecessary complications, US Legal Forms is readily available to you.

Our online repository of over 85,000 current legal documents covers nearly every aspect of your financial, legal, and personal matters.

Examine the document preview and descriptions to ensure you have located the form you need. Confirm that the template you choose aligns with the regulations of your state and county. Select the appropriate subscription plan to obtain the Secured Loan With Collateral. Download the document, then complete, validate, and print it. US Legal Forms boasts a strong reputation and over 25 years of expertise. Join us today and make form execution a simple and efficient process!

- With just a few clicks, you can swiftly access state- and county-specific templates meticulously crafted for you by our legal professionals.

- Utilize our platform whenever you require trustworthy and dependable services through which you can effortlessly locate and download the Secured Loan With Collateral.

- If you're familiar with our services and have previously set up an account with us, simply Log In to your account, select the template, and download it, or re-download it at any time in the My documents section.

- Not registered yet? No worries. It takes minimal time to establish and navigate the library.

- But before diving straight into downloading Secured Loan With Collateral, consider these suggestions.

Form popularity

FAQ

No, a secured loan and collateral are not the same thing. A secured loan is the financial product you obtain, while collateral is the asset you pledge to secure that loan. Think of collateral as a safety net for the lender, and the secured loan as the agreement you enter into. Understanding this distinction can help clarify your borrowing options.

Yes, a secured loan is commonly referred to as a collateral loan. Both terms describe a loan where the borrower pledges an asset to back the loan amount. This connection means that if you do not repay, the lender can take possession of the collateral. Therefore, understanding these terms can help you make informed financial decisions.

When you take out a secured loan with collateral, you risk losing the asset if you fail to repay the loan. This can include your home, car, or other valuable items. If you default, the lender has the right to seize your collateral, which can lead to significant financial loss. It's important to fully understand the terms of the loan and ensure you can meet the repayment obligations.

As far as common forms of collateral go, cash in a bank account, such as a savings account or certificate of deposit, usually works well since the value is clear and the funds are readily available. Garvey says you can use a car, house, jewelry or other valuable asset as long as you're the owner.

What can be used as collateral for a personal loan? Real estate. Vehicles you own. Savings account. Money market or certificate of deposit (CD) accounts. Investments, such as stocks and bonds in an investment account. Fine art and collectibles. Jewelry, or other valuables.

Collateral can include a house, car, boat, and so forth ? really, whatever a lender is willing to hold. You may also be able to use investment accounts, cash accounts, or certificates of deposit (CDs) as collateral to get the cash you need.

A secured collateral loan requires that the borrower use their assets (such as a car, house or savings account) as collateral to ?secure? the loan. The collateral is a promise to the lender that if the borrower cannot repay the loan, the lender can take possession of that asset.

In short, secured loans require collateral while unsecured loans do not. You'll also find that secured loans are far easier to qualify for and generally have lower interest rates as they pose less risk to the lender.