Consignment Form Of Retailing In Travis

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Sale occurrence: The consignor can recognize revenue only when the consignee sells the consigned goods to a third party (i.e., the end customer). Reliable transaction information: The consignor can recognize revenue when they have received reliable and timely reports from the consignee about sales transactions.

Instead, the supplier records them in their books under consignment inventory, keeping them separate from their regular stock. The supplier should enter into their journal: Debit: Consignment inventory (to track the value of goods sent out) Credit: Inventory (to reduce their regular stock)

For this you will need a report that includes all transactions over the tax year. This report should naturally detail the sale of consigned items, surcharges, and taxes collected or any additional revenue streams. These will all be reported under “total sales” in the tax form.

Accounting for consignment sales – before 1099-Ks The consignee just reports the commission amount as their income. In fact, if the consignor sends the consignee more than $600 in commission payments, there's a good chance of them sending the consignee a 1099.

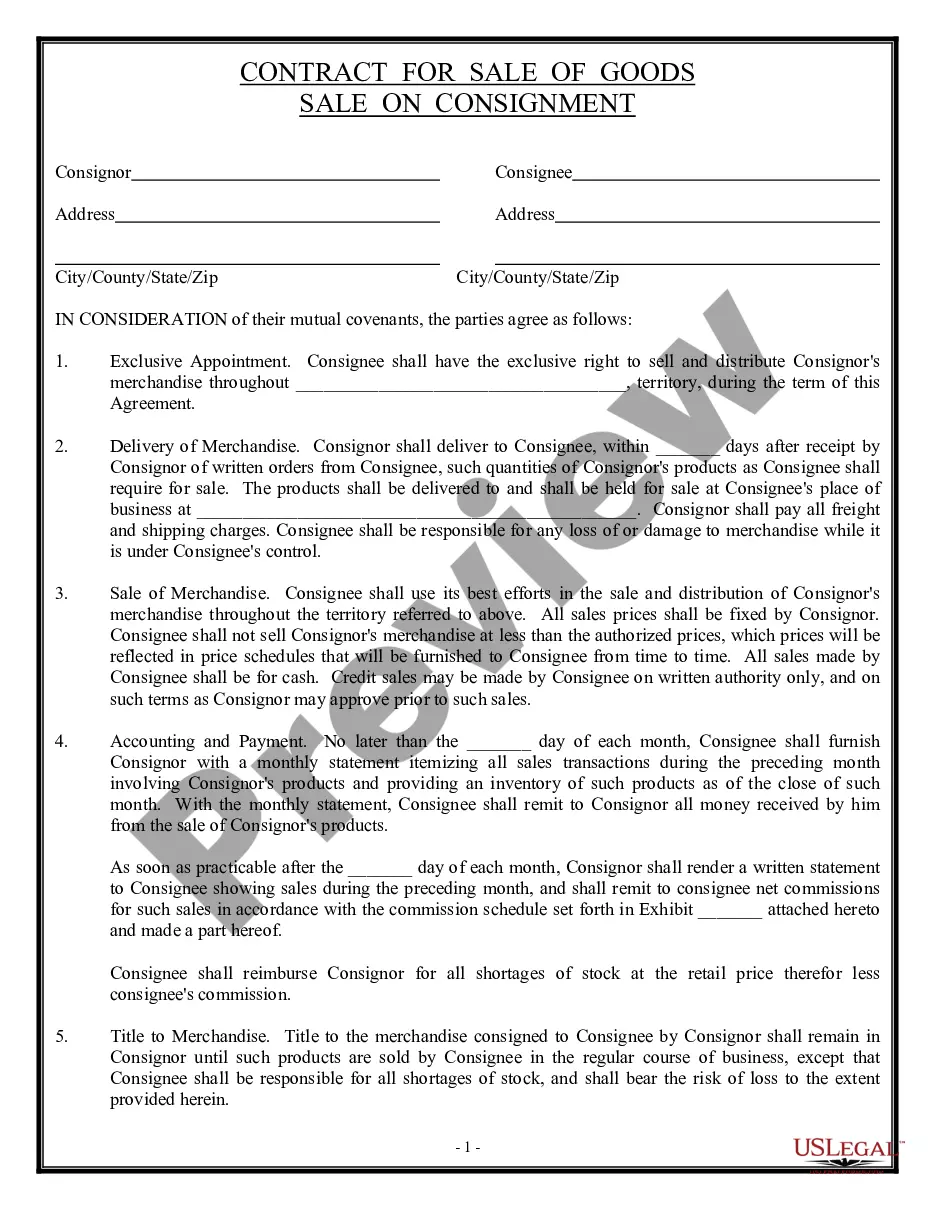

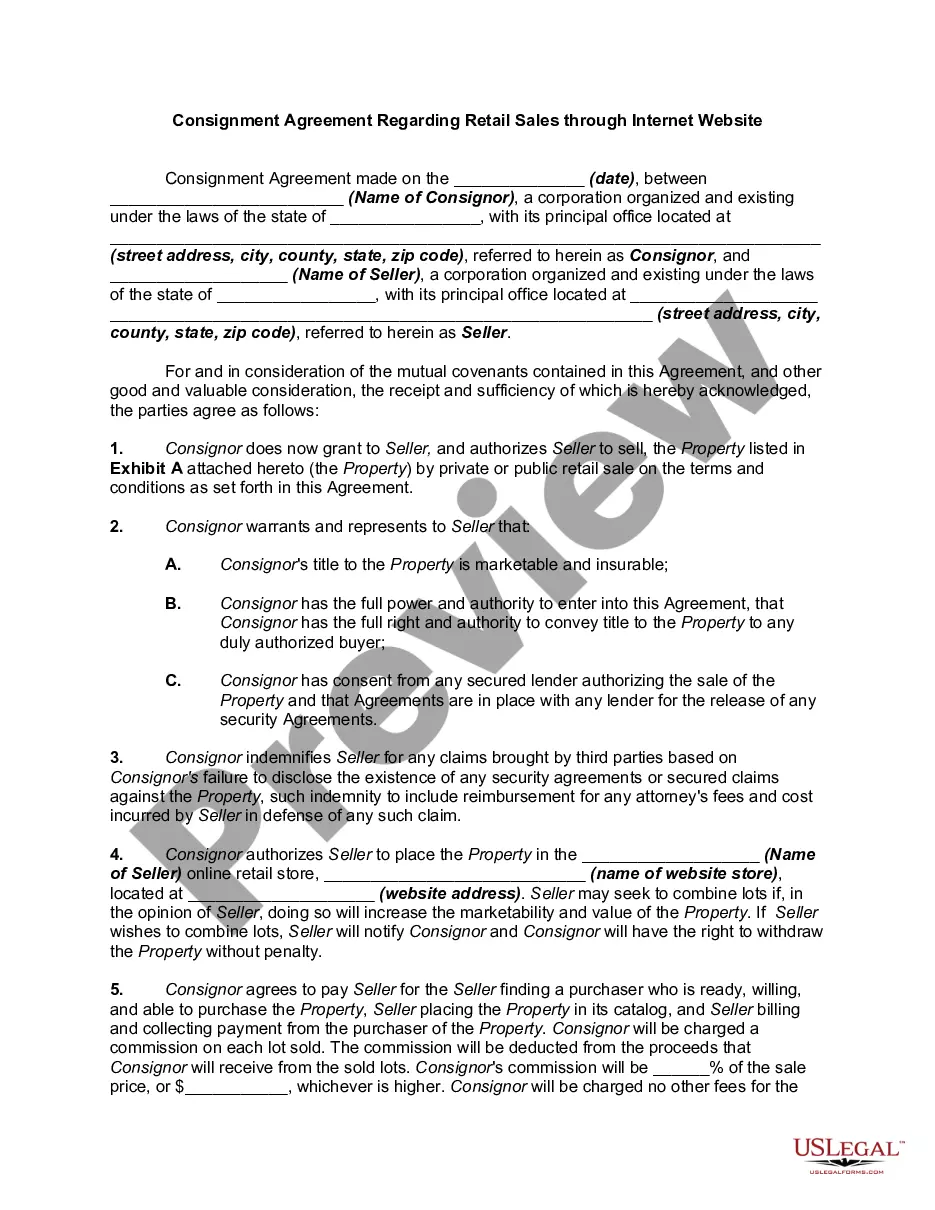

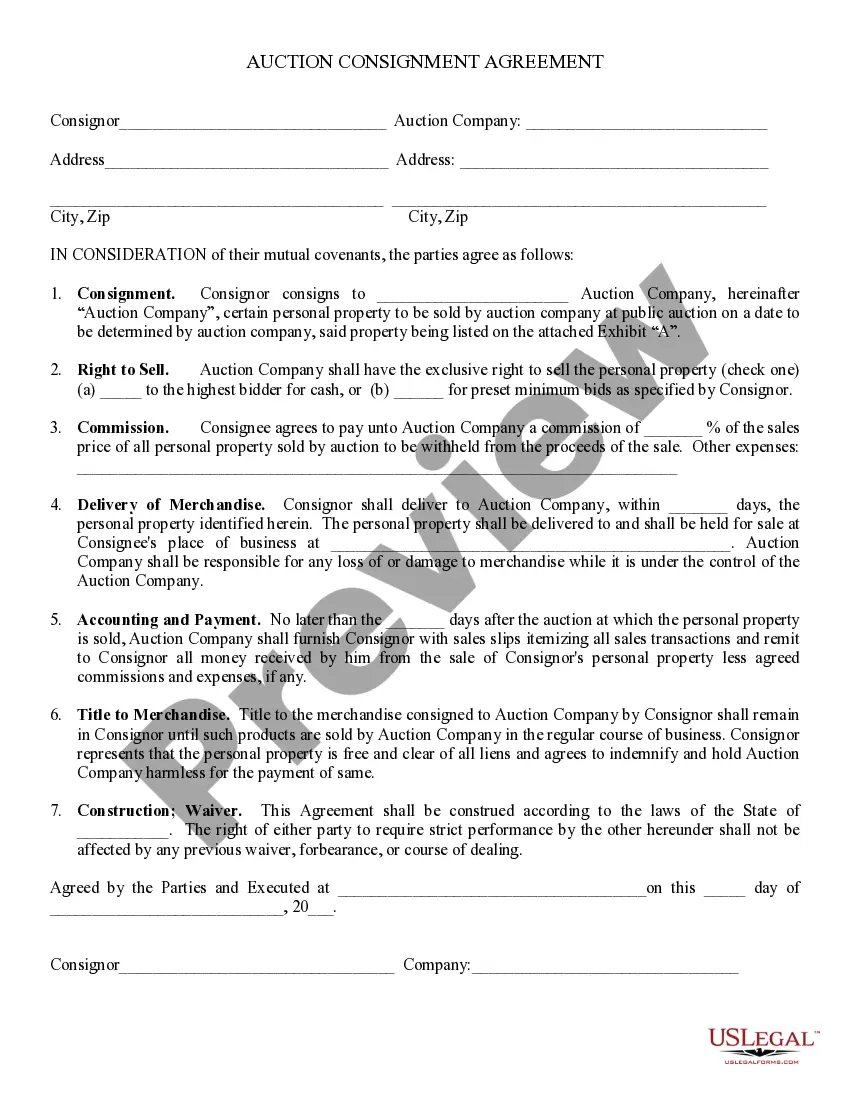

This kind of arrangement is called Consignment. Definition. The contract or an agreement of sending several goods by the producers or manufacturers of a place to their agents for the sale is known as a consignment. Types of Consignment. Outward Consignment. Inward Consignment. Consignment Processing. Sale. Features of a Sale.

Consignment is a process whereby a person gives permission to another party to take care of their property while retaining full ownership of the property until the item is sold to the final buyer. It is generally done during auctions, shipping, goods transfer, or putting something up for sale in a consignment store.

Selling goods on consignment is described as a situation whereby goods are shipped to a dealer who pays you, the consignor, only for the merchandise which sells. The dealer, referred to as the consignee, has the right to return to you the merchandise which does not sell and without obligation.

“Consignment only” refers to a unique selling arrangement, where you retain ownership of your item until it sells. You entrust your goods to a store or platform (the consignee) to market and sell on your behalf. This model is especially popular in fashion, art, and antiques.

Traditional inventory is owned by the retailer or company and must be purchased beforehand. Consignment inventory, on the other hand, belongs to the supplier until it is sold to the customer, and the retailer only pays the supplier when the merchandise is sold.

Consignment is not the same as selling goods. A consignment is an agreement between the owner of goods and the consignor. The consignee stores and sells goods on behalf of the consignor and earns a profit. A sale, on the other hand, is a simple transaction, with goods being traded between two parties.