Consignment Agreement In Oracle Fusion In Queens

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

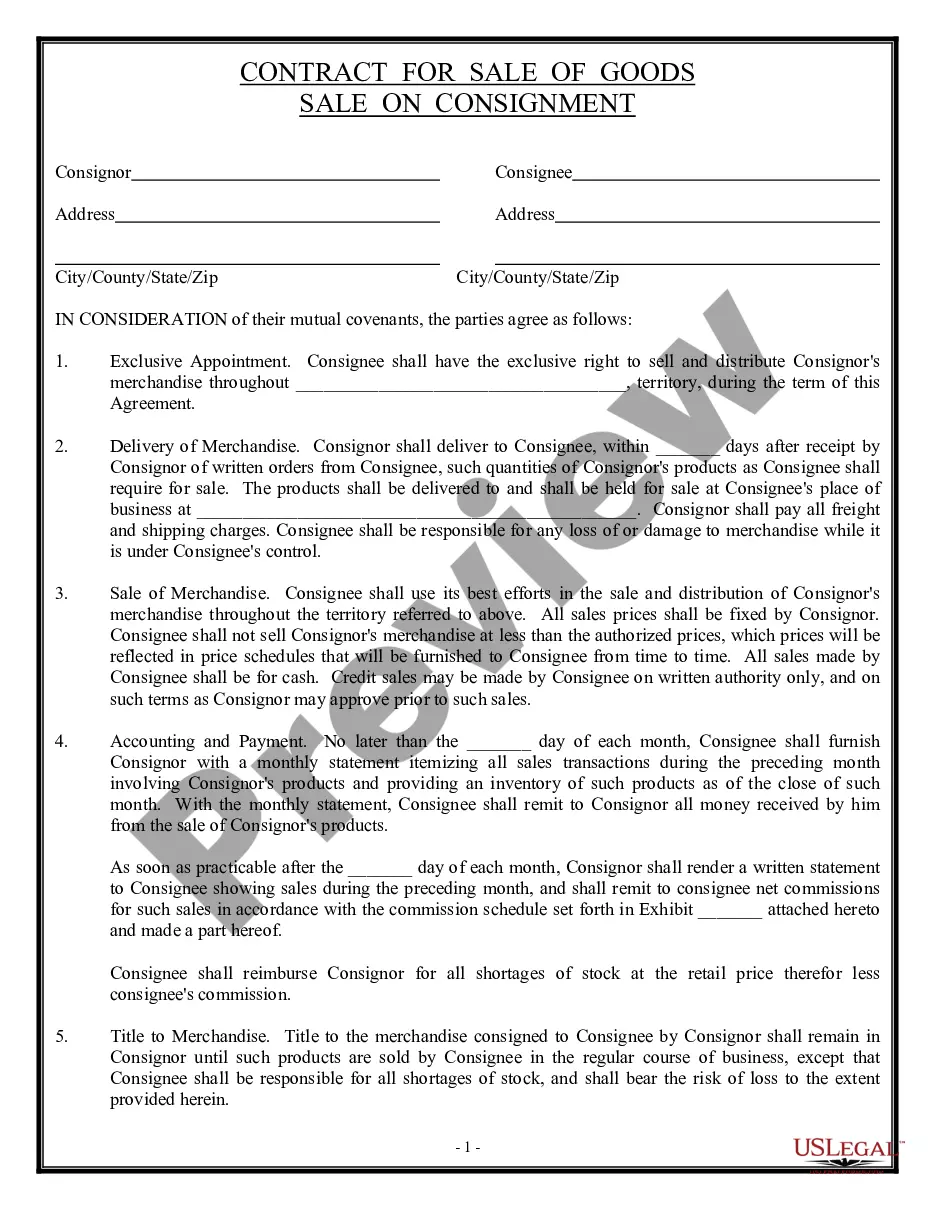

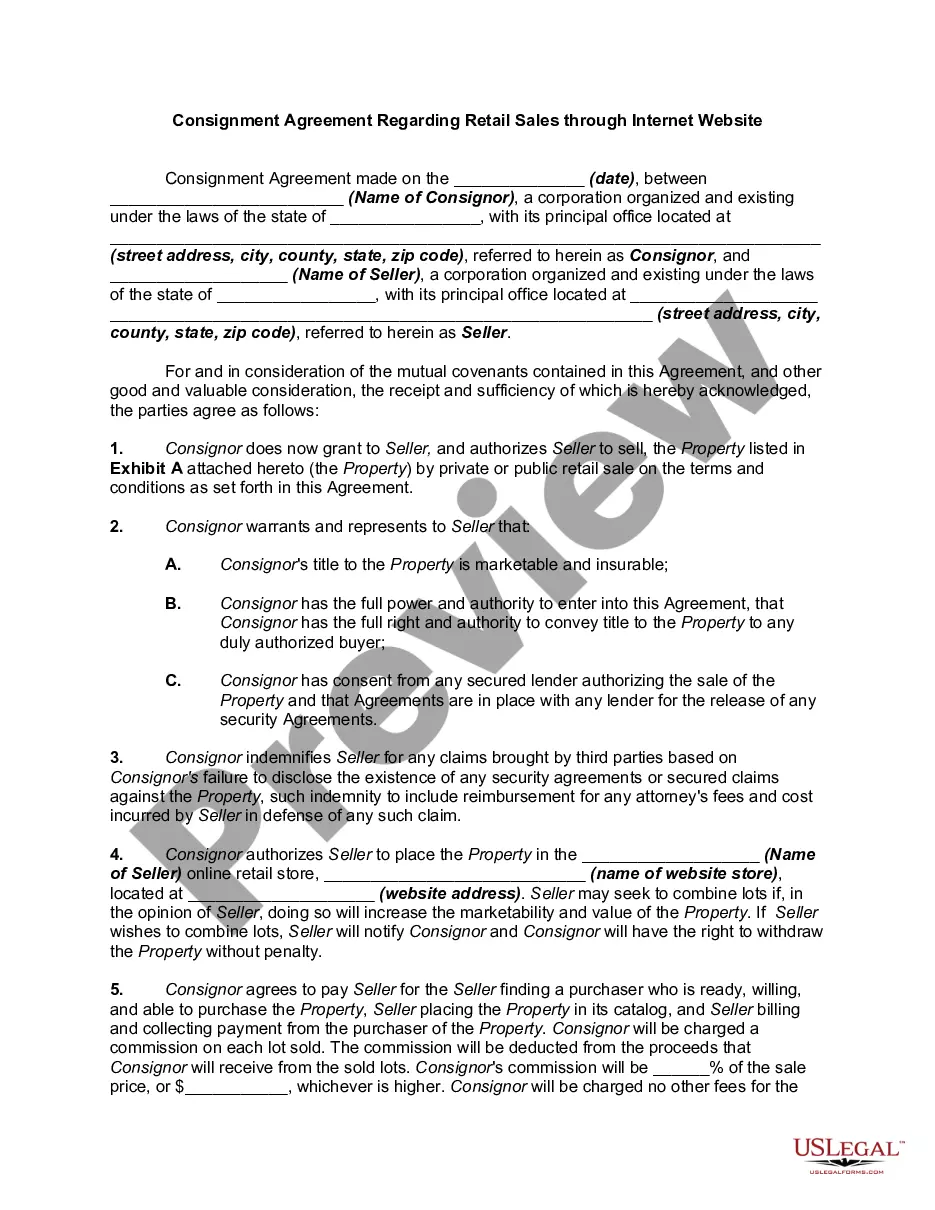

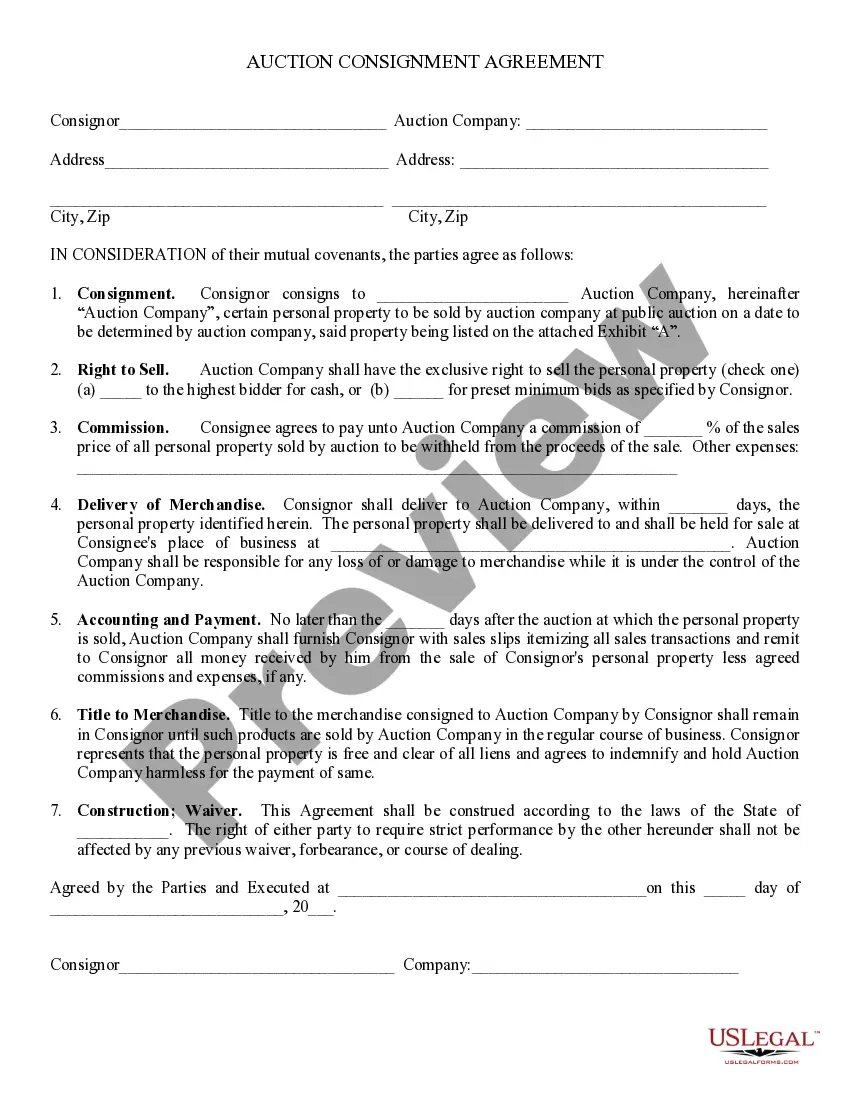

In a consignment agreement, a consignor supplies goods to a consignee, who sells them on the consignor's behalf. The consignee earns a commission from each sale and sends the remaining sales revenue to the consignor. The consignor retains ownership of the goods until they are sold.

View Supplier Details In the Suppliers work area, click the Manage SAM Trading Partners task. On Manage SAM Trading Partners, select the UEI record for which you want to view the supplier details. From the More Actions menu, click View Supplier.

Consigned inventory refers to items that are in the possession of one party, but remain the property of another party by mutual agreement. The process of consigned inventory follows steps between the buyer and seller.

In a VMI solution, vendors actively manage the supply of inventory to target levels based on the buyer's forecast and actual consumption, while consignment inventory relates to inventory owned by the vendor but held at the buyer's warehouse with the buyer determining the inventory replenishment strategy.

The VMI process is a supply chain management strategy where a supplier manages the inventory at the customer's location. The inventory is owned either by the customer (VMI without consignment) or the supplier (VMI with consignment), but maintained by the supplier.

This kind of arrangement is called Consignment. Definition. The contract or an agreement of sending several goods by the producers or manufacturers of a place to their agents for the sale is known as a consignment. Types of Consignment. Outward Consignment. Inward Consignment. Consignment Processing. Sale. Features of a Sale.

Here are the essential components to include: Parties Involved: Names and contact information of the consignor and the consignee. Consigned Goods: Detailed description of the goods being consigned, including quantities and specifications. Consignment Period: Duration of the consignment arrangement.

How to Write a Consignment Agreement Parties Involved: Names and contact information of the consignor and the consignee. Consigned Goods: Detailed description of the goods being consigned, including quantities and specifications. Consignment Period: Duration of the consignment arrangement.

The accounting treatment of consignment inventory under IAS-2 ensures accurate recognition and measurement by establishing clear principles for ownership and valuation. Consigned goods remain on the consignor's financial statements until sold, while the consignee records only commission or fees earned.

In consignment inventory, the supplier retains ownership of the goods until they are sold by the retailer, who pays the supplier only after the sale. In vendor-managed inventory (VMI), the supplier manages and replenishes the retailer's inventory levels based on agreed-upon metrics.