Consignment Form Template With Drop Down List In New York

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

A document that shows the details of goods that have been sent from a seller to a buyer, and that travels with the goods: rail/air/road consignment note. See also. bill of lading.

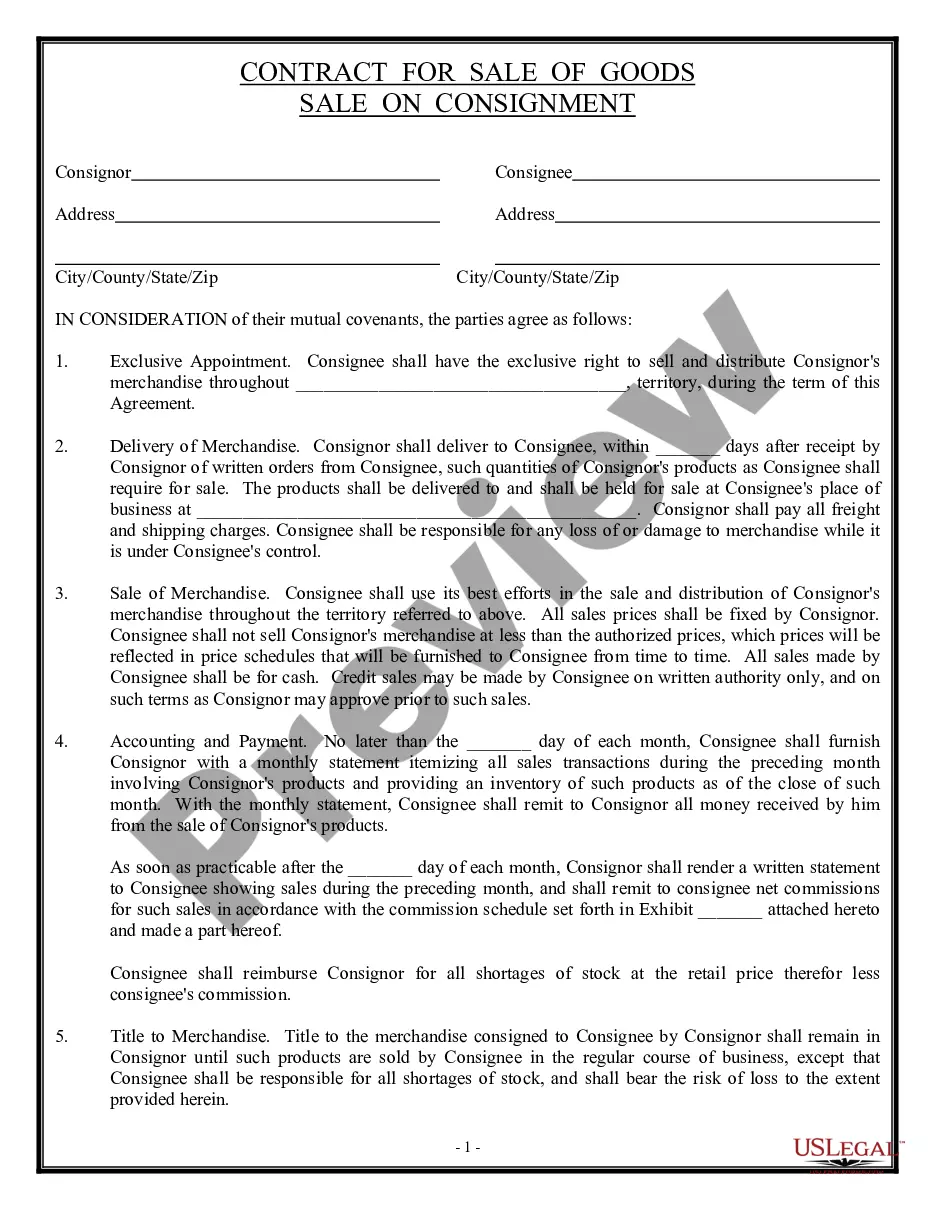

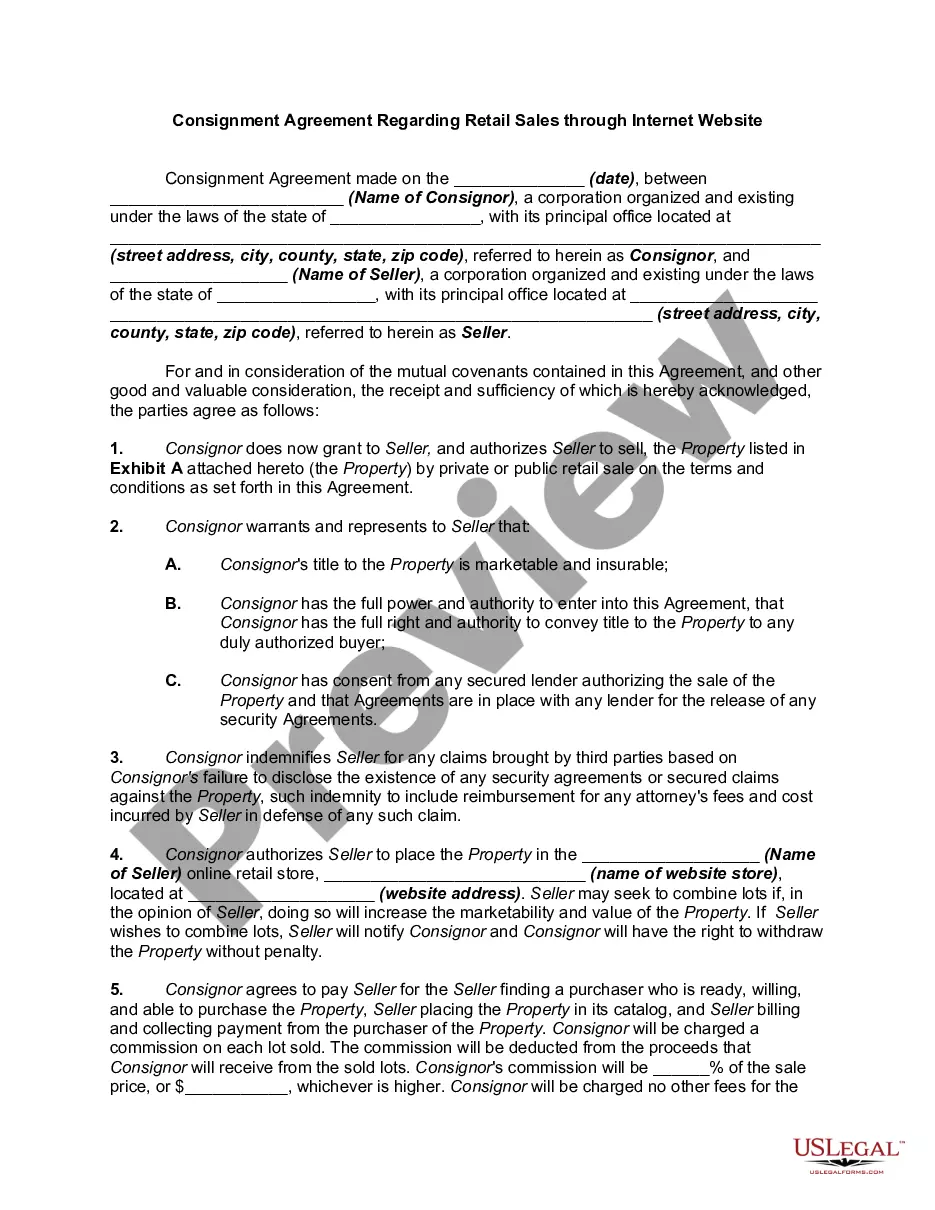

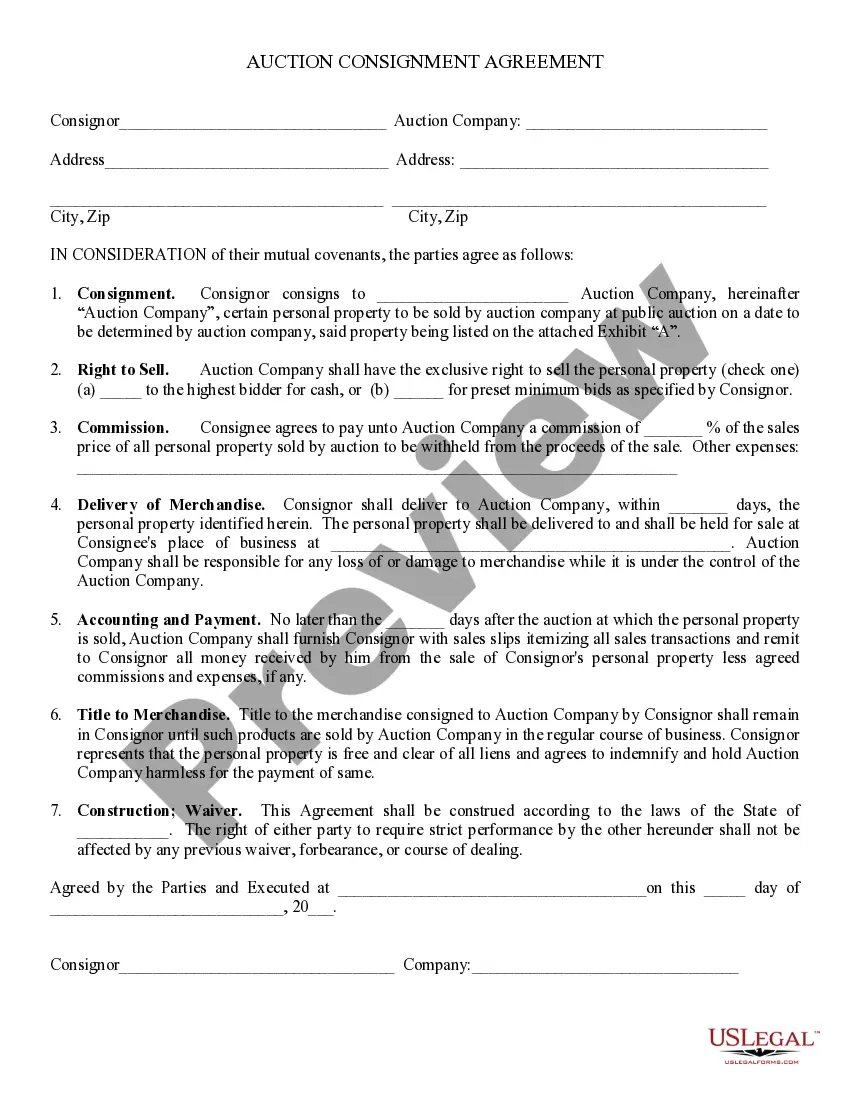

How to Write a Consignment Agreement Parties Involved: Names and contact information of the consignor and the consignee. Consigned Goods: Detailed description of the goods being consigned, including quantities and specifications. Consignment Period: Duration of the consignment arrangement.

Consignment is a type of contract in which the consignor delivers the goods to the consignee for sale . The consignee takes care of the goods and sells them. Until the goods are sold, the consignor does not lose ownership of the goods.

A consignment agreement is a contract between a consignor (owner or supplier of goods ) and a consignee (who sells the goods). Its purpose is to outline the terms and conditions for the sale of goods, including payment terms, agreement duration, rights and duties of both parties.

Every consignment includes the name and address of the consignor and consignee. In the case of an interstate transfer, the place of supply has to be mentioned. Every challan includes the name and address of the consignor and consignee.

How do you handle consignment inventory? To handle consignment inventory, a supplier (the consignor) and a retailer (the consignee) agree on a contract that stipulates that the supplier retains ownership of the goods until the retailer makes a sale. A retailer can also return any unsold goods to the supplier.

The journal entry accounts for the sales and expenses of the consignment inventory. No entry is made by the consignee. It's important to note that the import duty of 200 is debited to the consignment inventory account.

Instead, the supplier records them in their books under consignment inventory, keeping them separate from their regular stock. The supplier should enter into their journal: Debit: Consignment inventory (to track the value of goods sent out) Credit: Inventory (to reduce their regular stock)

Consignment in accountancy is related to goods that are kept with an authorized third party who is called a consignee. This consignee is responsible for selling the goods on the behalf of the consignor. While the consignee sells the good in consignment, the ownership of the goods is retained by the consignor.

Goods held on consignment are included in the inventory of the supplier (consignor), not the retailer (consignee).