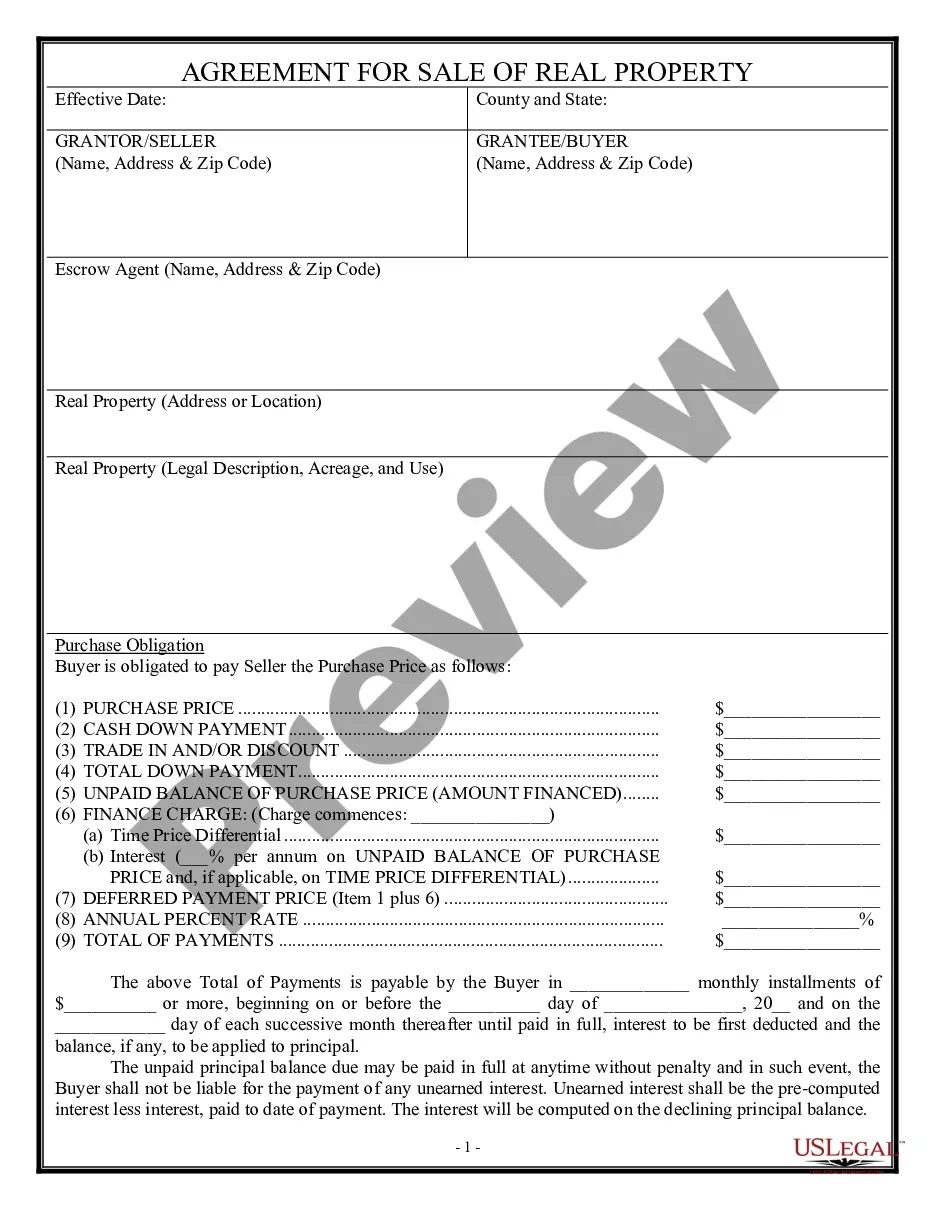

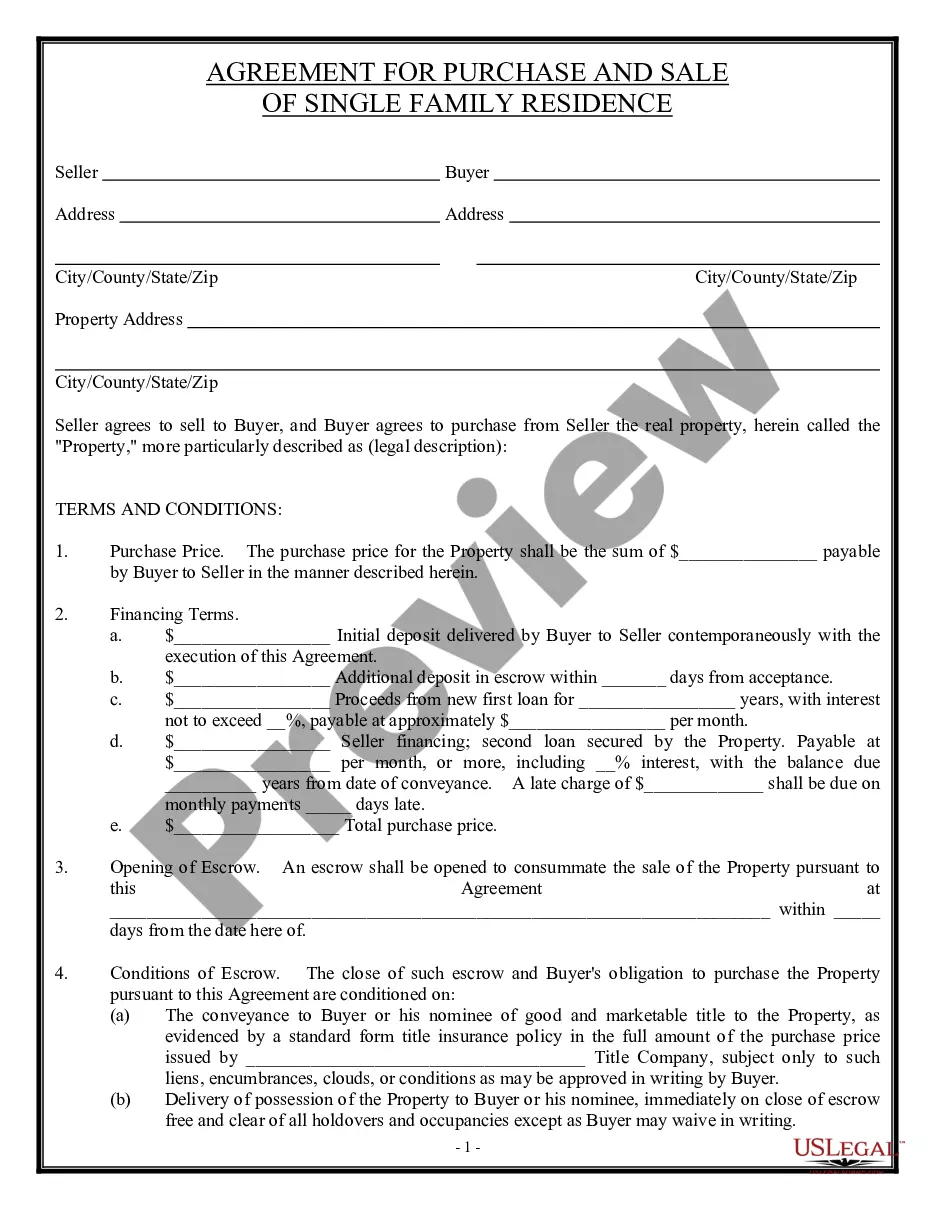

Closure Any Property Formula In Sacramento

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

A seller/transferor that qualifies for a full, partial, or no withholding exemption must file Form 593. Any remitter (individual, business entity, trust, estate, or REEP) who withheld on the sale/transfer of California real property must file Form 593 to report the amount withheld.

Tax withheld on California source income is reported to the Franchise Tax Board (FTB) using Form 592, Resident and Nonresident Withholding Statement. Form 592 includes a Schedule of Payees section, on Side 2, that requires the withholding agent to identify the payees, the income amounts, and the withholding amounts.

A seller/transferor that qualifies for a full, partial, or no withholding exemption must file Form 593. Any remitter (individual, business entity, trust, estate, or REEP) who withheld on the sale/transfer of California real property must file Form 593 to report the amount withheld.

Who needs the California Fiduciary Income Tax Return Form 541 Overview? Trustees responsible for managing the assets of a trust. Executors of estates required to file a tax return. Individuals who need to report income received from trusts or estates.

Write a note to the Sacramento County Assessor, 3636 American River Drive, Suite 200, Sacramento, CA 95864-5952. Provide your name, parcel number, property address, new mailing address, daytime telephone number, and signature. Use the Change of Address on your tax bill. The change will be forwarded to the Assessor.

Form 593, also known as the “Real Estate Withholding Certificate,” is a document used in California real estate transactions. It serves as a mechanism for the collections of state income tax on the gain from the sale or transfer of real property.

Prop. 19 would eliminate a loophole that has allowed the children and grandchildren of original property owners to avoid paying market-value taxes on a property that is not their primary residence.

In November 1978, California voters passed Proposition 8, which amended Article XIII A to allow temporary reductions in assessed value in cases where real property suffers a decline in value. Proposition 8 is codified by section 51(a)(2) of the Revenue and Taxation Code.

Transfers that will trigger a reassessment: Change in Ownership: Purchases and non-primary residence transfers among friends or family.

Property tax in California is calculated at a standard rate of 1% of the assessed property value, plus additional charges for voter-approved bonds, fees, and special charges.