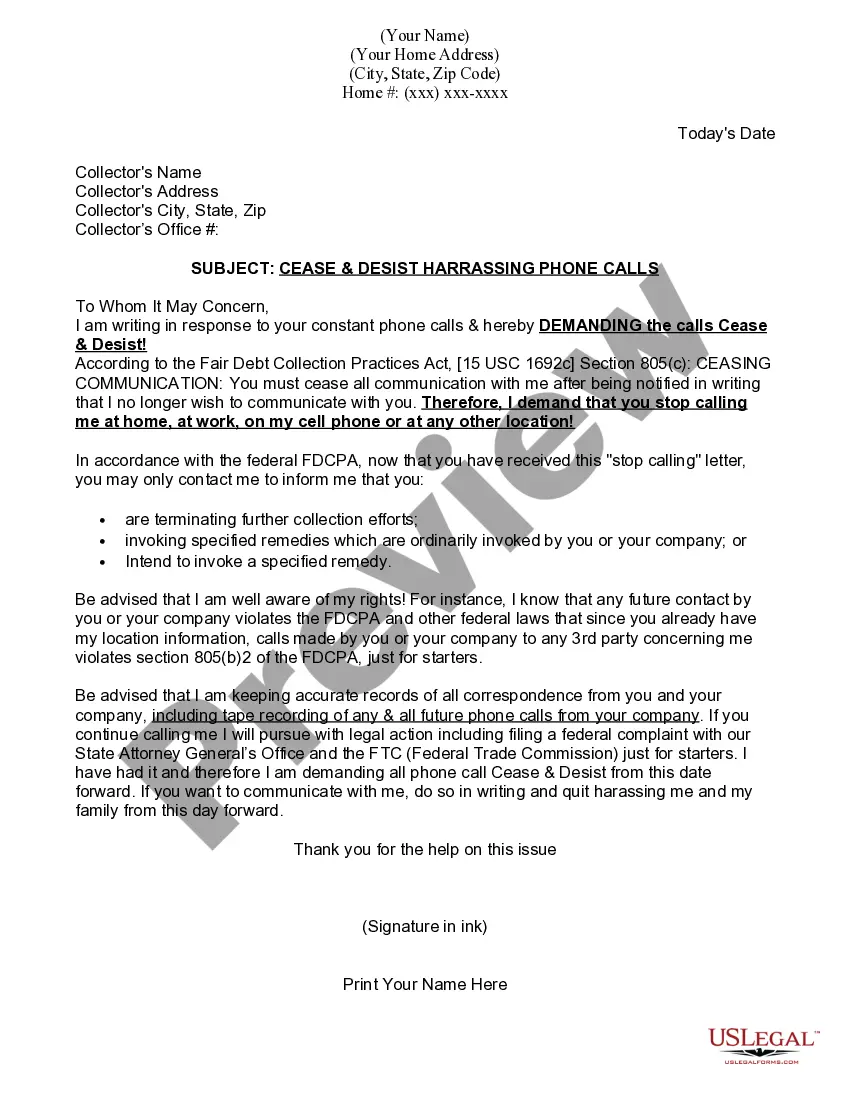

Sending A Cease And Desist Letter To Debt Collector In San Diego

Description

Form popularity

FAQ

Anyone can write a cease and desist letter without an attorney. You could write such a letter yourself requesting that certain actions stop. However, this kind of letter is not law (in Florida or any state), and it carries less impact when it comes from an individual versus a lawyer.

Once written, you can send a C&D via email, mail, or even in person. Sending it by certified mail is a good option because it requires a signature from the recipient, so you'll know when they receive it. Once sent, your C&D letter is effective for as long as the deadline you provide.

Cease and Desist Letters can be created and sent yourself, or by an attorney on your behalf, and they can be used for a wide variety of issues, including harassment, defamation (including slander or libel), or the unauthorized use of intellectual property.

You should dispute a debt if you believe you don't owe it or the information and amount is incorrect. While you can submit your dispute at any time, sending it in writing within 30 days of receiving a validation notice, which can be your initial communication with the debt collector.

In your desist letter, state a reasonable deadline by which the recipient must cease the offending activity. Evidence: If you have evidence supporting the claims of infringing activity or wrongdoing—such as photographs, screenshots, or previous communications—include it with your letter.

First, write the collection agency within 30 days of receiving the first notice, informing them that you dispute the debt and why. Make sure your letter is dated, properly addressed and shows the account number shown on the notice. It is also vital that you keep a copy of all correspondence for your records.

It depends on what you can afford. Your full and final settlement should offer equal amounts to each creditor. For example: Your lump sum is 75% of your total debt. You should offer each creditor 75% of what you owe them.

Starting Jan. 1, a new state law will prohibit health providers and debt collectors from reporting medical debt information to credit agencies. That means unpaid medical bills should no longer show up on people's credit reports, which consumer advocacy groups say is a boon for patients with debt.

“Negotiating with a collection agency can be challenging, but it is vital to reach a fair settlement,” Raymond Quisumbing, a registered financial planner at Bizreport, said. “Offering 25%-50% of the total debt as a lump sum payment may be acceptable.

It is not uncommon to settle debt with a collection agency at 30%-50% of the amount owed. An overall strategy in dealing with collection agencies depends on your circumstances and the practices of the collection agency that bought your debt.