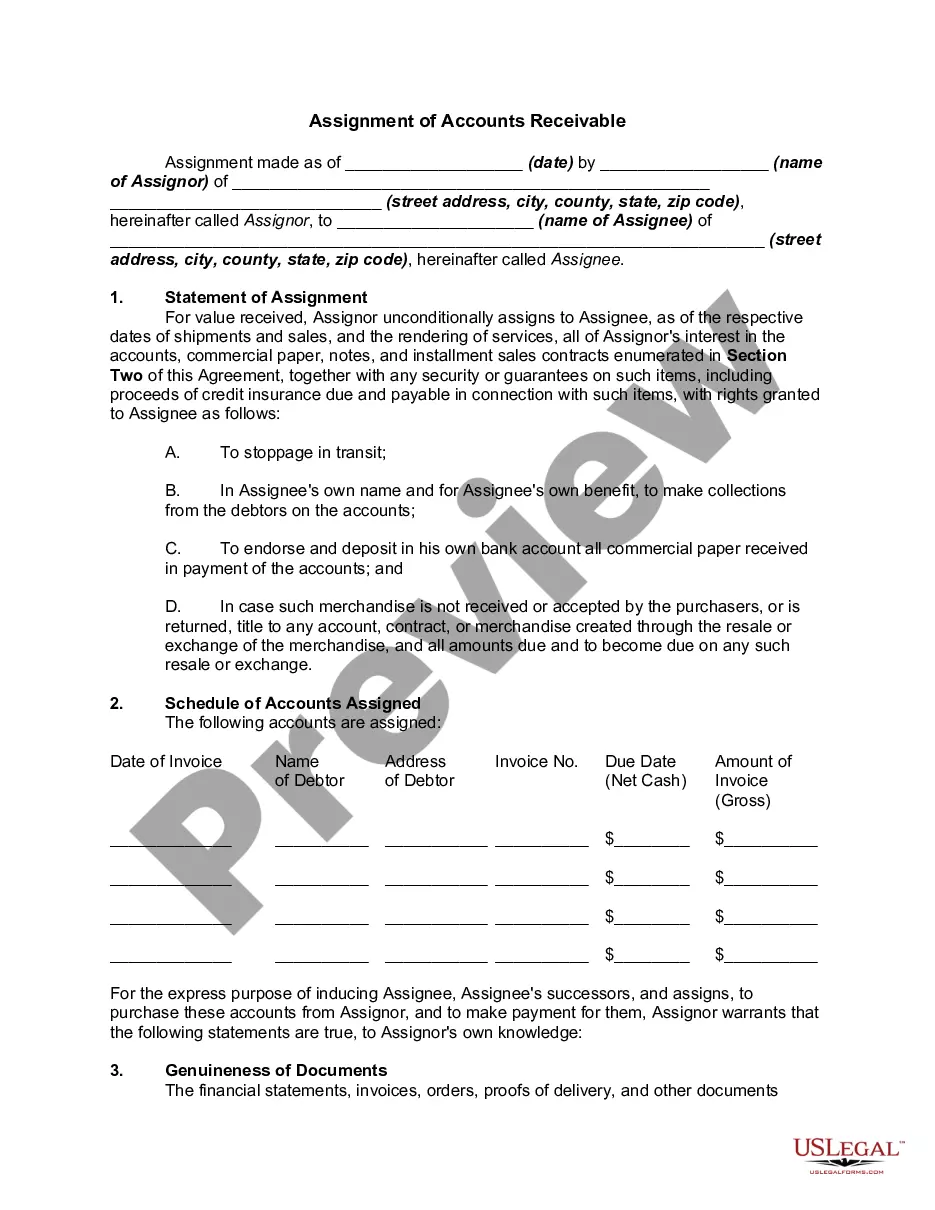

Accounts Receivable Contract For Dummies

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Accounts Receivable - Contract To Sale?

The Accounts Receivable Agreement For Beginners you see on this page is a versatile formal template created by qualified attorneys in accordance with federal and state regulations.

For over 25 years, US Legal Forms has supplied individuals, organizations, and legal practitioners with more than 85,000 validated, state-specific templates for any business and personal situation. It’s the quickest, easiest, and most dependable method to obtain the documents you require, as the service ensures the utmost level of data protection and anti-malware safeguards.

Register for US Legal Forms to have authenticated legal templates for all of life’s circumstances at your fingertips.

- Search for the document you require and examine it.

- Browse through the example you looked for and preview it or read the form description to confirm it matches your requirements. If it doesn’t, use the search feature to find the suitable one. Click Buy Now when you have identified the template you need.

- Register and Log In.

- Select the pricing plan that meets your needs and create an account. Utilize PayPal or a credit card for prompt payment. If you already possess an account, Log In and verify your subscription to continue.

- Obtain the editable template.

- Pick the format you prefer for your Accounts Receivable Agreement For Beginners (PDF, Word, RTF) and download the template to your device.

- Complete and sign the documents.

- Print the template to fill it out by hand. Alternatively, use an online versatile PDF editor to quickly and accurately complete and sign your document with a legally-binding electronic signature.

- Redownload your documents again.

- Use the same form again whenever required. Access the My documents tab in your account to redownload any previously downloaded templates.

Form popularity

FAQ

An accounts receivable contract is a legal agreement between a seller and a buyer that outlines the terms for the payment of goods or services. This contract specifies the amount due, payment terms, and any penalties for late payment. Understanding this concept can be simplified with our resource, 'Accounts Receivable Contract for Dummies', which breaks down the essential components and benefits. By using tools like US Legal Forms, you can easily create or manage these contracts to ensure clarity and compliance.

The 5 Cs of credit RBC refer to Character, Capacity, Capital, Collateral, and Conditions, similar to the 5 C's of accounts receivable management. These elements help lenders evaluate credit risk and make informed decisions. Understanding these principles will aid you in drafting an accounts receivable contract for dummies, ensuring that both parties are clear about the terms and responsibilities.

While all 5 C's are essential, Character often stands out as the most critical factor. It reflects a customer’s reliability and willingness to repay debts. By focusing on Character, you can build stronger relationships and create a more effective accounts receivable contract for dummies to ensure timely payments.

The 5 C's of accounts receivable management include Character, Capacity, Capital, Collateral, and Conditions. These factors help assess a customer's creditworthiness and inform your credit decisions. Understanding these components can enhance your ability to create an effective accounts receivable contract for dummies, ultimately supporting your business’s financial health.

The accounts receivable process starts with credit approval for new customers. Once approved, you issue invoices as products or services are delivered. Afterward, you track payments and send reminders for overdue accounts. Finally, you reconcile accounts to ensure all transactions are accurate. This structured approach can be easily understood through an accounts receivable contract for dummies.

The 10 rule for accounts receivable suggests that 10% of your customers generate 90% of your revenue. Understanding this distribution can help you focus your collection efforts on the most valuable clients. Additionally, by creating an accounts receivable contract for dummies, you can simplify the management of these key relationships and ensure timely payments.

Managing accounts receivable involves five key steps. First, establish clear credit policies to guide your decisions. Next, invoice promptly and accurately to ensure customers understand their obligations. Third, monitor accounts regularly to identify overdue payments. Fourth, follow up on late payments with reminders. Finally, review and adjust your credit policies based on performance, which can help you understand how to create an accounts receivable contract for dummies.

When explaining accounts receivable in an interview, focus on its role in a company's financial health. You can describe it as the total amount owed by customers for goods or services delivered on credit. Mention how an accounts receivable contract for dummies can help individuals understand the basics, such as tracking payments and managing collections. This approach shows your understanding of the topic and its importance in business operations.