Shares For Resolution In Clark

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

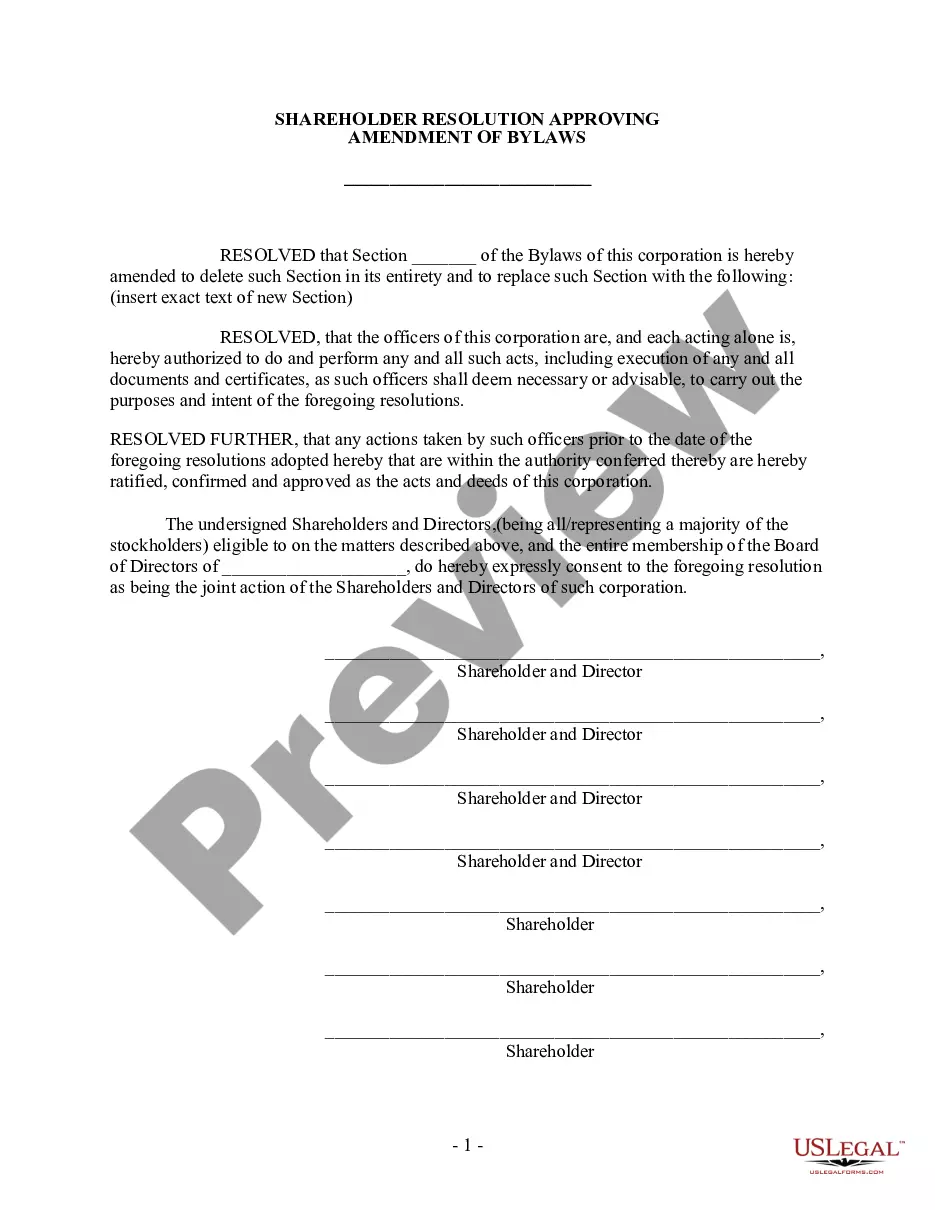

Class A shares generally have more voting power and higher priority for dividends, while Class B shares are common shares with no preferential treatment. Class C shares can refer to shares given to employees or alternate share classes available to public investors, with varying restrictions and voting rights.

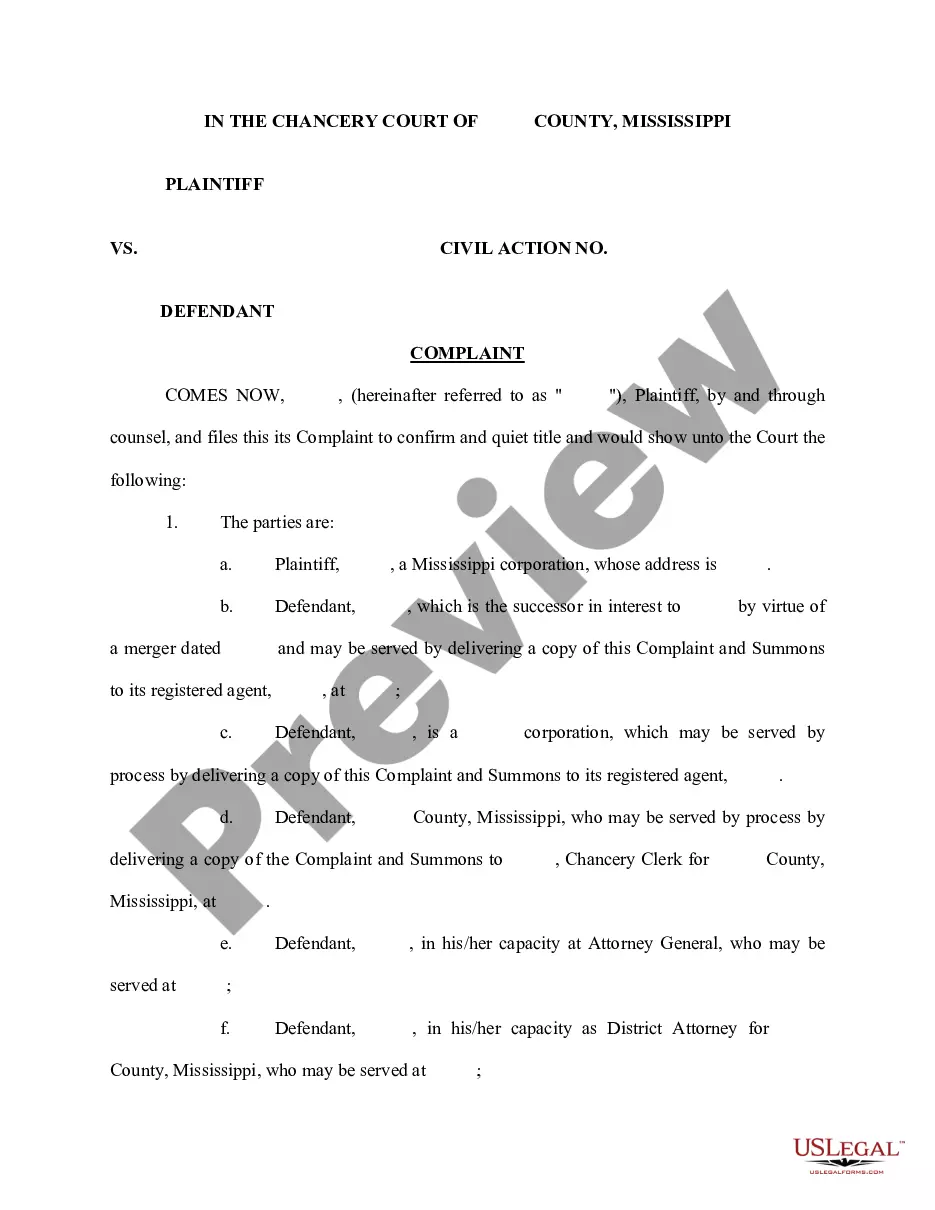

A corporate resolution stock transfer is necessary before company shares are eligible for transfer from one person to another. Generally, your company's board of directors will approve the resolution and then distribute copies of the resolution to stockholders.

If a company wishes to issue additional shares to a new shareholder, all existing shareholders within the company must pass a special board resolution to that effect.

A Directors' Resolution to Issue Shares is a resolution to be passed by the directors of a company to approve the allotment and issue of new shares.

If a company wishes to issue additional shares to a new shareholder, all existing shareholders within the company must pass a special board resolution to that effect.

You do not always need to have a meeting to pass a resolution. If enough shareholders or directors have told you they agree, you can usually confirm the resolution in writing. You must write to all shareholders letting them know about the outcome of a resolution.

An ordinary resolution requires approval by a bare or simple majority of the votes cast on the motion (that is, not less than 50% +1 votes out of all votes cast, which excludes from both the numerator and denominator all shares whose votes are not cast for whatever reason including abstention).

Board resolution is essential for the transfer of shares in case of private limited company.

Special resolution preparation If a company wishes to issue additional shares to a new shareholder, all existing shareholders within the company must pass a special board resolution to that effect.

Share buybacks – key points At least 75% of the shareholding must be bought back – this can be in one instalment or under multiple instalments. Shareholder approval is required. There must be sufficient distributable reserves. Funding for the transaction is from the company.