Judgment Lien Foreclosure California In Georgia

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

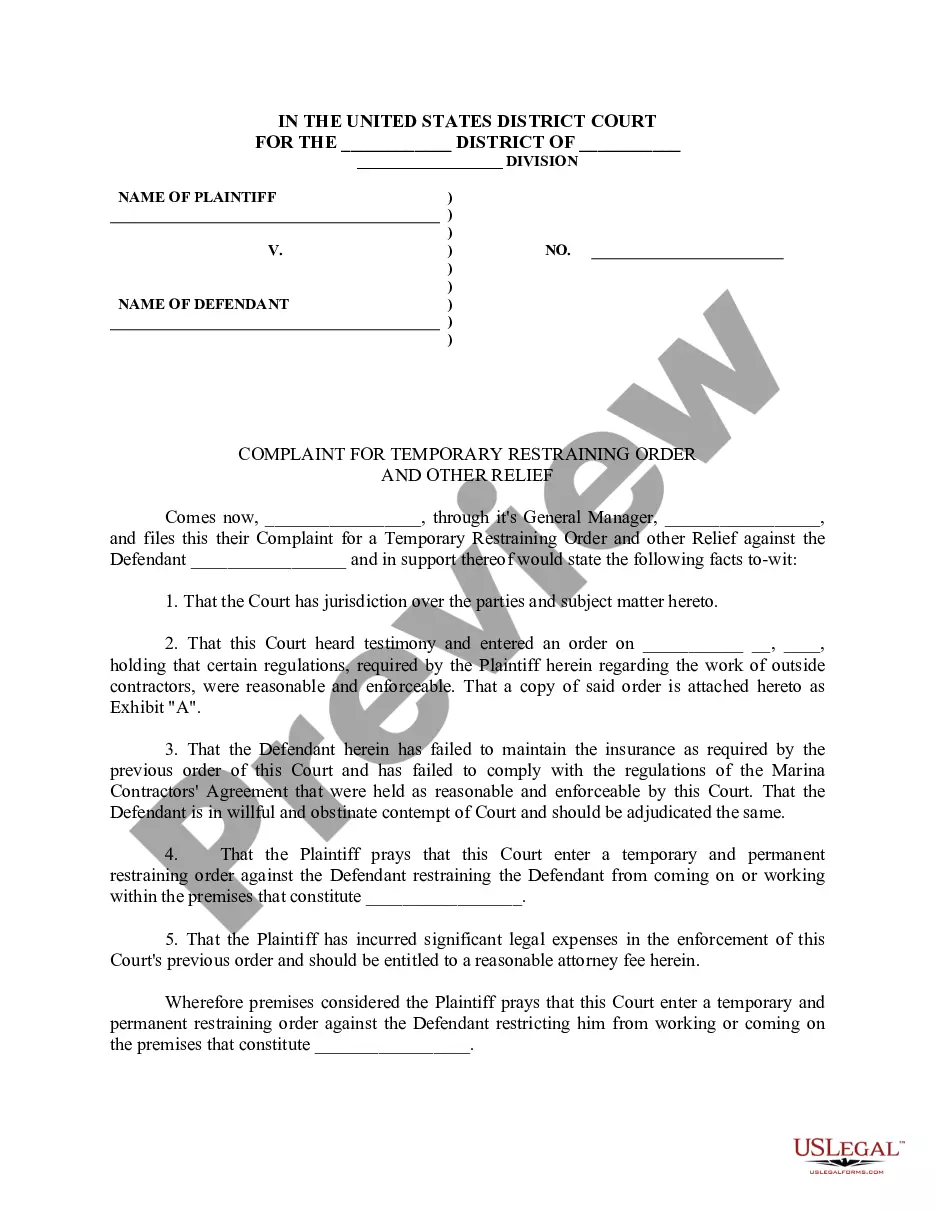

Of the three types of liens (consensual, statutory, and judgment), the judgment lien is the most dangerous form, but one which the informed business owner may be able to eliminate. A judicial lien is created when a court grants a creditor an interest in the debtor's property, after a court judgment.

With a mortgage foreclosure, a ucc lien can survive. So it is a mortgage foreclosure, yes.

A Georgia judgment becomes dormant—meaning it's unenforceable—seven years after it's issued. Georgia law lets you renew a judgment before it goes dormant, and you also have an opportunity to revive a dormant judgment.

2nd and Junior Mortgages (such as home equity loans, etc.) Credit Card Judgments (recorded after the foreclosing mortgage) Personal Judgments (recorded after the foreclosing mortgage) Mechanic's Liens (recorded after the foreclosing mortgage) Other Judgments (recorded after the foreclosing mortgage)

Following a first mortgage foreclosure, all junior liens (including a second mortgage and any junior judgment liens) are extinguished, and the liens are removed from the property's title. However, the second mortgage debt and creditor's judgment remain, even though they're no longer attached to the foreclosed property.

Here are a few ways to remove the lien: Invalidate the lien. If the lien is invalid or was obtained in a manner that doesn't follow the procedural requirements under the law, an attorney may be able to strip the lien from the property. Satisfy the debt. Negotiate a lower payoff. File for bankruptcy.

(2) A person asserting the lien, either for himself or as a guardian, administrator, executor, or trustee, may move to foreclose the lien by making an affidavit to a court of competent jurisdiction showing all the facts necessary to constitute a lien and the amount claimed to be due.

If you put liens on the other side's property, you or the other side must remove them. To remove a lien, file a certified copy of the Acknowledgment of Satisfaction of Judgment (form EJ-100) with each county recorder's office where you put the lien on their property.

Most judgments (the court order saying what you're owed) expire in 10 years. This means you can't collect on it after 10 years. To avoid this, you can ask the court to renew it. A renewal lasts 10 years.