Assets Asset Purchase With Lease In Cuyahoga

Description

Form popularity

FAQ

Under GAAP, fixed (tangible) assets have three primary characteristics: Acquired and held for use in operations, (e.g., not held for sale); Long-term in nature (greater than 1 year); and. Possess physical substance.

CAPITALIZATION POLICY Fixed assets should be capitalized when all the following criteria are met: The asset is tangible or intangible in nature, complete in itself, and is not a component of another capitalized item. The asset is used in the operation of the Council's activities.

To qualify for capitalization of a fixed asset, the IRS states that the item must have a useful life of at least one year. It has to be productive in the operations of the business. If investments like vacant land are not used for business operations, they will not qualify.

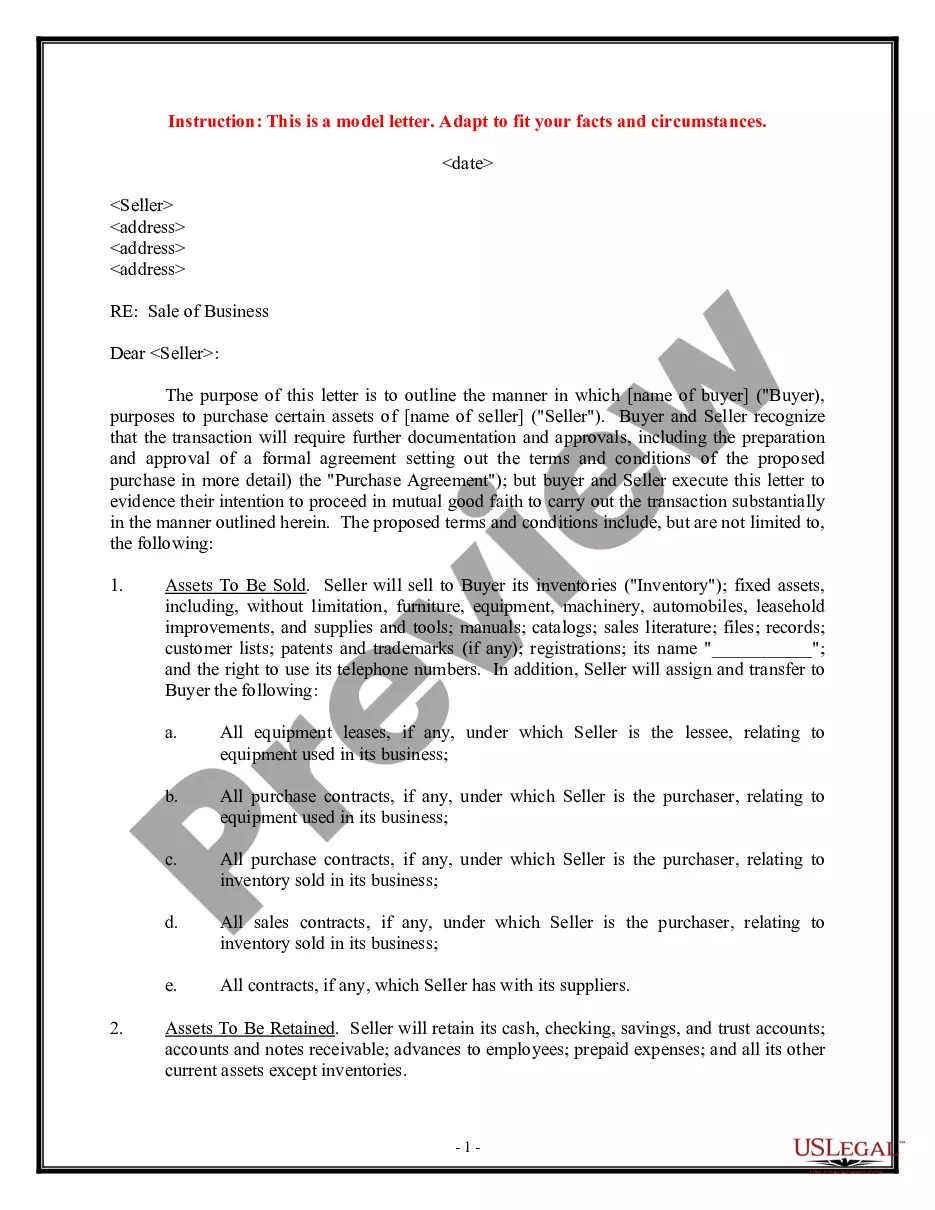

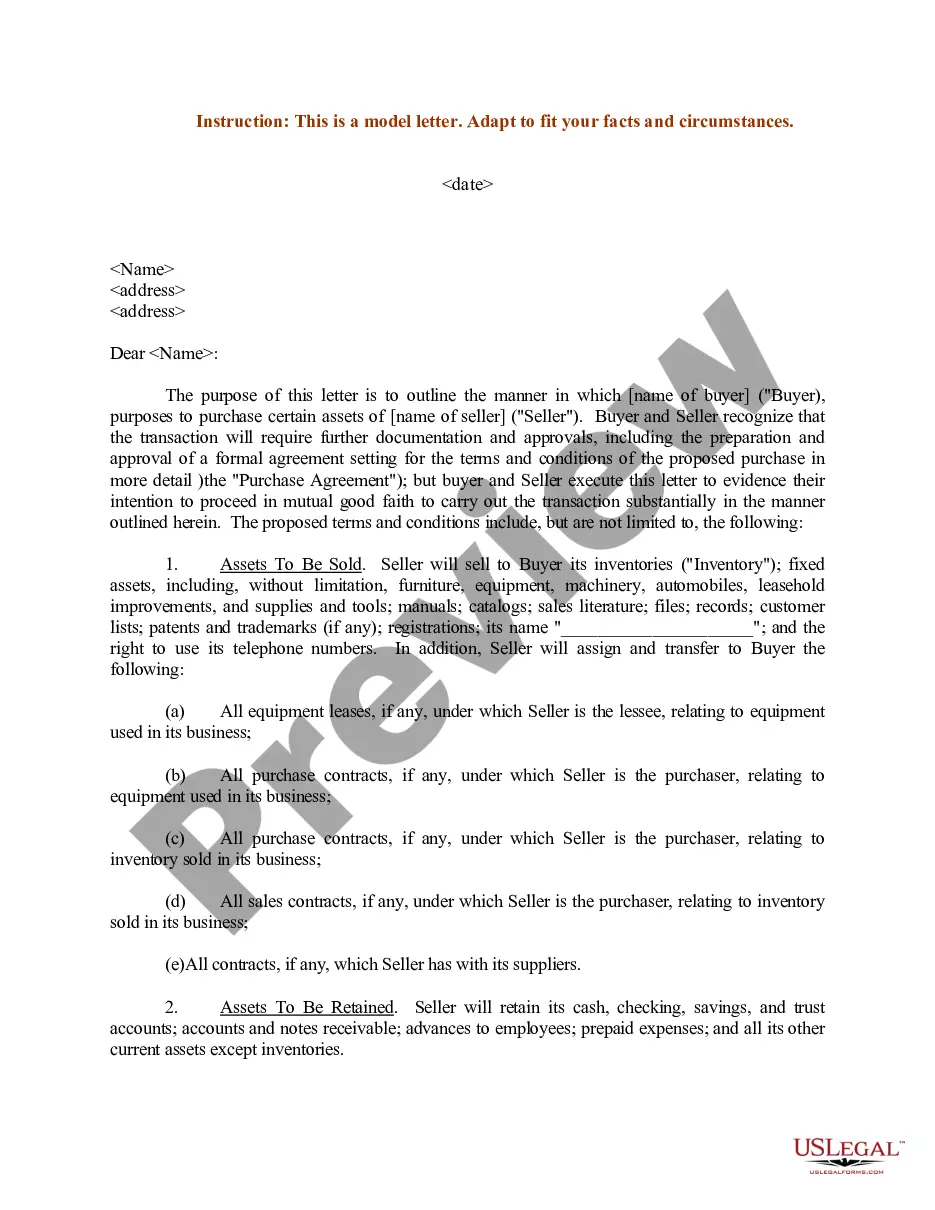

The equipment (personal property) or real estate (real property) that is the subject of a lease and currently leased is a leased asset. In general, any identifiable, tangible and nonconsumable asset to which title can be held can be leased.

Types of Leased Assets All types of equipment and machinery including heavy equipment for construction (e.g. loaders, bulldozers, excavators … etc.) All types of heavy and light transportation vehicles (trucks, buses, passenger cars). Computer devices and equipment. Medical equipment.

touse lease asset is an intangible capital asset. The asset represents the right to use an underlying asset identified in a lease contract, as specified for a period of time.

The seller retains legal ownership of the company that has sold the assets but has no further recourse to the sold assets. The buyer assumes no liabilities in an asset sale. Typically, for reasons having to do with tax benefits, buyers prefer asset sales, whereas sellers prefer stock sales.