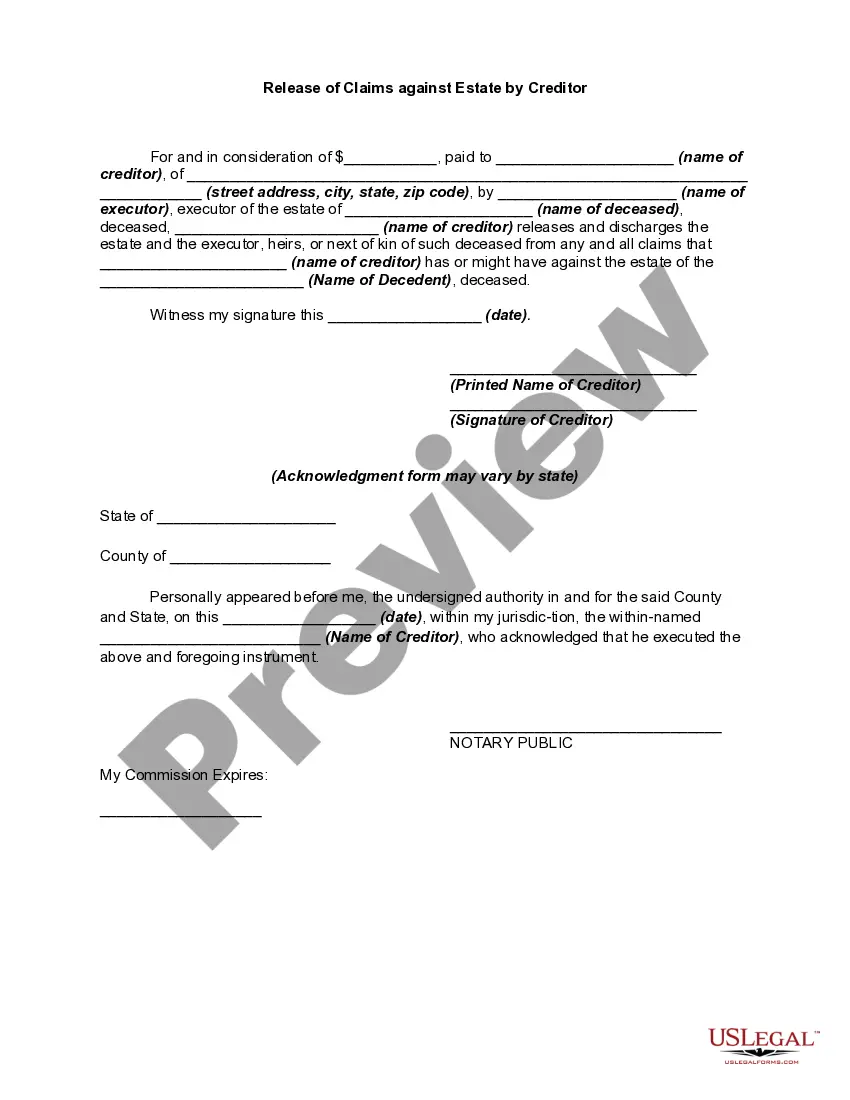

Secured Debt Shall For Bad Credit In Bronx

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

Settling is always better than going to court. A court-ordered judgment is SERIOUSLY life-affecting. Your wages could be garnished and the judgment will forever be on your record. You may even find the court case in various places on the internet.

Unfortunately, it usually means the creditor or debt collector will win the case by default. If this happens, the court will issue a default judgment against you. This court order allows for more aggressive collection measures including wage garnishment, property seizure, and/or a bank account levy.

Specifically, the rule states that a debt collector cannot: Make more than seven calls within a seven-day period to a consumer regarding a specific debt. Call a consumer within seven days after having a telephone conversation about that debt.

Effective April 7, 2022, the New York statute of limitations for debt collection lawsuits arising out of a consumer credit transaction is reduced from six years to three years.

Summary: If you're being sued by a debt collector, here are five ways you can fight back in court and win: 1) Respond to the lawsuit, 2) make the debt collector prove their case, 3) use the statute of limitations as a defense, 4) file a Motion to Compel Arbitration, and 5) negotiate a settlement offer.

Chapter 13 Eligibility Any individual, even if self-employed or operating an unincorporated business, is eligible for chapter 13 relief as long as the individual's combined total secured and unsecured debts are less than $2,750,000 as of the date of filing for bankruptcy relief.

Statute of Limitations in New York Thanks to a law passed in 2021, the statute of limitations of debt in New York is three years, which means that's how much time a debt collector has to file a lawsuit to recover the debt through the court system.

What Is the Statute of Limitations for Debt in New York? The New York statute of limitations for consumer debt is three years. This means creditors or debt collectors have three years to try to collect on an unpaid debt or sue you for a debt. After this time limit has expired, the debt is considered time-barred.

Creditors must take additional steps to obtain a default judgment against you. As of April 7, 2022, creditors cannot sue or make a threat to sue you on debts that are older than three years. Additionally, any payments you make after the three- year period, does not restart clock on the time-barred debt.

In most states, the statute of limitations for collecting on credit card debt is between three and 10 years, but a few states allow for longer periods, extending up to 15 years.