Master Sales Agreement With Seller Financing In Illinois

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

How to draft a contract in 13 simple steps Start with a contract template. Understand the purpose and requirements. Identify all parties involved. Outline key terms and conditions. Define deliverables and milestones. Establish payment terms. Add termination conditions. Incorporate dispute resolution.

How to make a contract in 7 steps Step 1: Outline the basics. Step 2: Define the key terms and scope of work. Step 3: Set payment terms. Step 4: Include protective clauses. Step 5: Negotiate. Step 6: Get a contract review. Step 7: Sign and date.

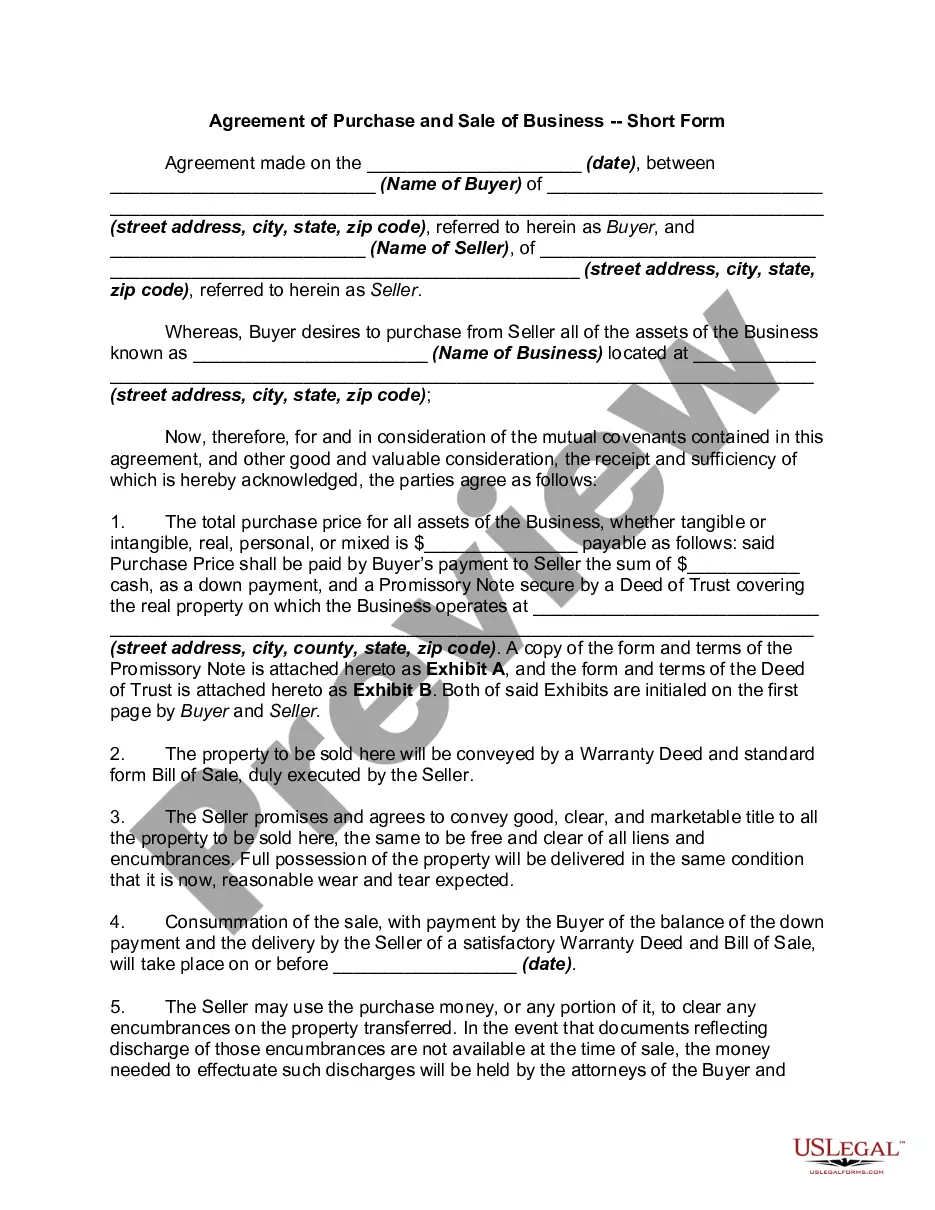

Sales agreement A sales agreement is the most fundamental sales contract. This is the document between a buyer and a seller that explains what's being purchased and the terms of the sale.

How do you write a contract for sale? Title the document appropriately. List all parties involved in the agreement. Detail the product or service, including all rights, warranties, and limitations. Specify the duration of the contract and any important deadlines.

It functions as a contract between two or more parties to guarantee that essential agreements are in place before any service commences. An MSA serves to minimize disagreements by providing an unmistakable description of what the parties can expect from one another.

Unlike contracts that typically apply to a one-time transaction between two parties, a Master Service Agreement is intended to outline the rights and responsibility of the parties involved in an ongoing relationship, including those that pertain to: The ownership rights of a property.

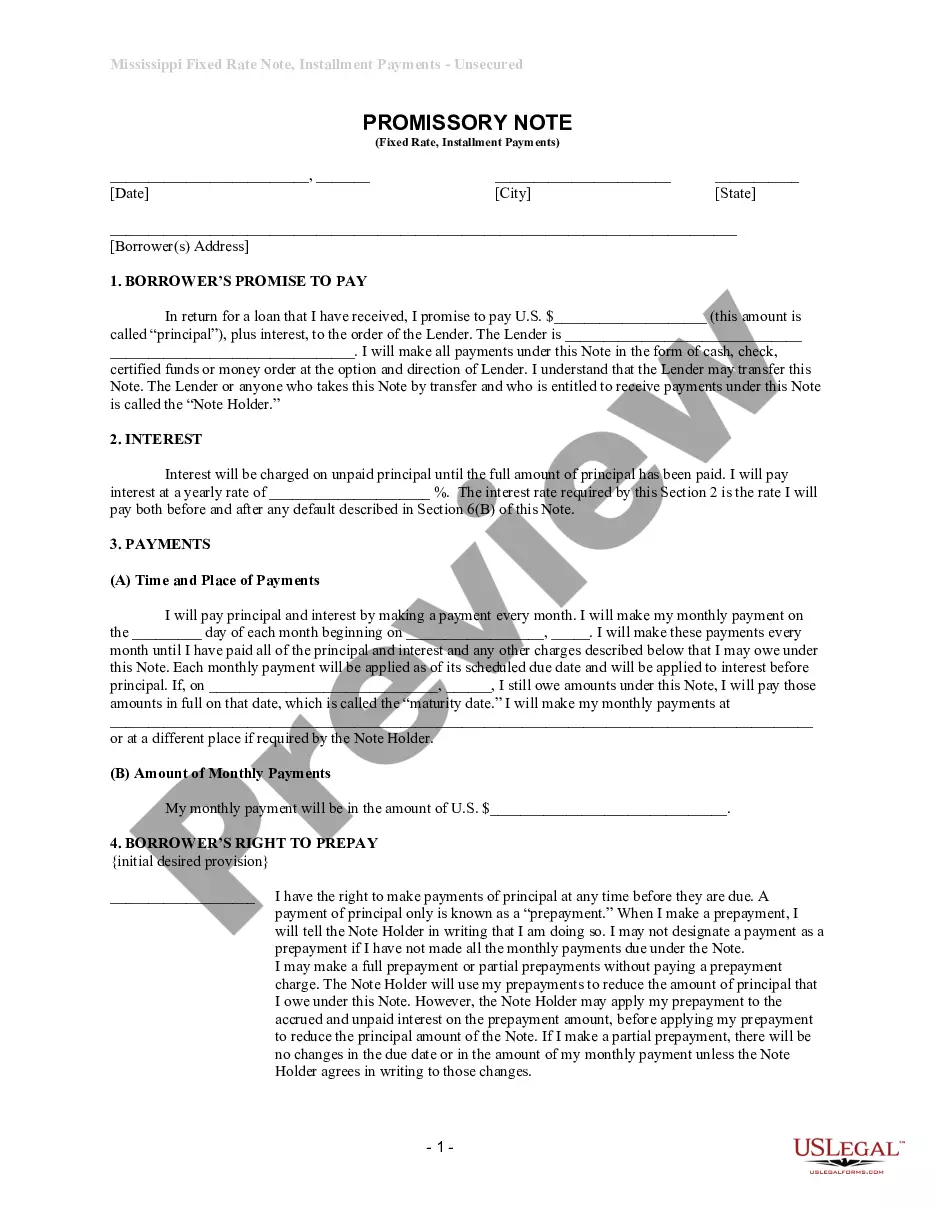

How Does Seller Financing Work? A bank isn't involved in a seller-financed sale; the buyer and seller make the arrangements themselves. They draw up a promissory note setting out the interest rate, the schedule of payments from buyer to seller, and the consequences should the buyer default on those obligations.

SELLER FINANCING UNDER DODD-FRANK This new rule also applies to sellers of residential dwellings to consumers in which the seller provides financing to the consumer secured by a mortgage on the dwelling, unless the seller is entitled to certain exclusions.

I've seen seller finance deals at 5-6% - which is attracting buyers who would normally get approved for a traditional mortgage. The down is usually 20-30% - and some are even extending terms over 15 or even 30 years.

Possible foreclosure. If the buyer stops making payments and won't leave the property, you might need to start the foreclosure process, which could take months or even years.