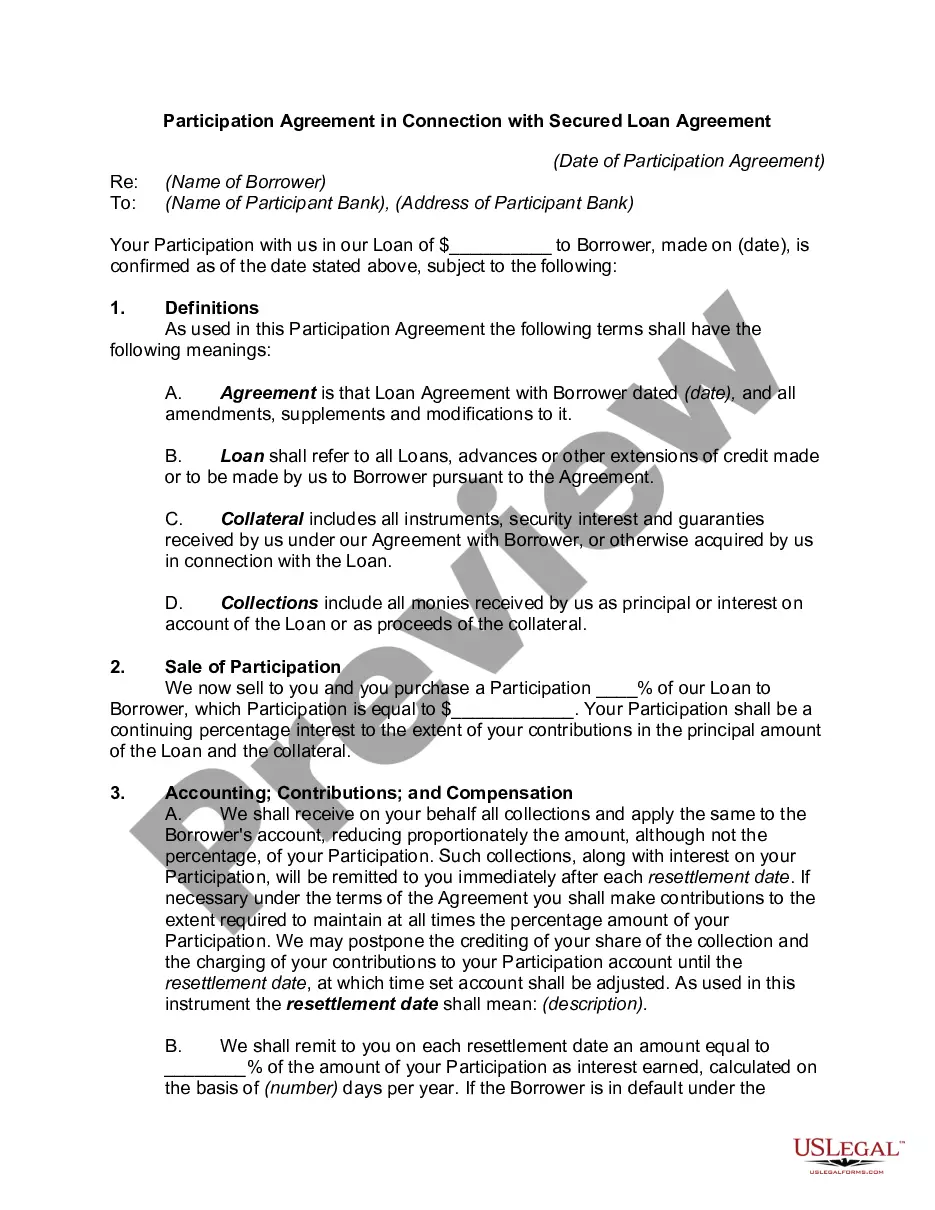

Loan Agreement Form Download With Personal Guarantee In Wake

Description

Form popularity

FAQ

For the guarantee to be enforceable it must prove that a debt is owed and provide sufficient proof of a valid obligation and enforceable debt. The creditor must prove you intended to be responsible for the debt you are being pursued for.

Personal guarantees are legally binding contracts, and breaching the terms can have serious legal consequences. Guarantors should be aware that defaulting on a personal guarantee could result in legal action. This could include judgments against personal assets, wage garnishments, or liens on property.

It can also result in the following consequences: Your personal credit declines if you can't make the payments. Your business credit declines if you can't make the payments. You could lose any collateral tied to the guarantee (e.g., equipment, home, car).

The term personal guarantee refers to an individual's legal promise to repay credit issued to a business for which they serve as an executive or partner. Providing a personal guarantee means that if the business becomes unable to repay the debt, the individual assumes personal responsibility for the balance.

Providing a personal guarantee means that if the business becomes unable to repay the debt, the individual assumes personal responsibility for the balance. Personal guarantees provide an extra level of protection to credit issuers who want to make sure they will be repaid.

Language to Use Use clear and concise language when drafting a personal guarantee. Make sure the language is easy to understand and unambiguous. Include a statement that the guarantor will be legally responsible for the debt. Specify the period of time that the guarantee is valid.