Agreement Accounts Receivable For Cash In Cook

Description

Form popularity

FAQ

The “10% Rule” is a specific guideline used in cross-aging to determine when a portion of a company's accounts receivable should be classified as doubtful or uncollectible.

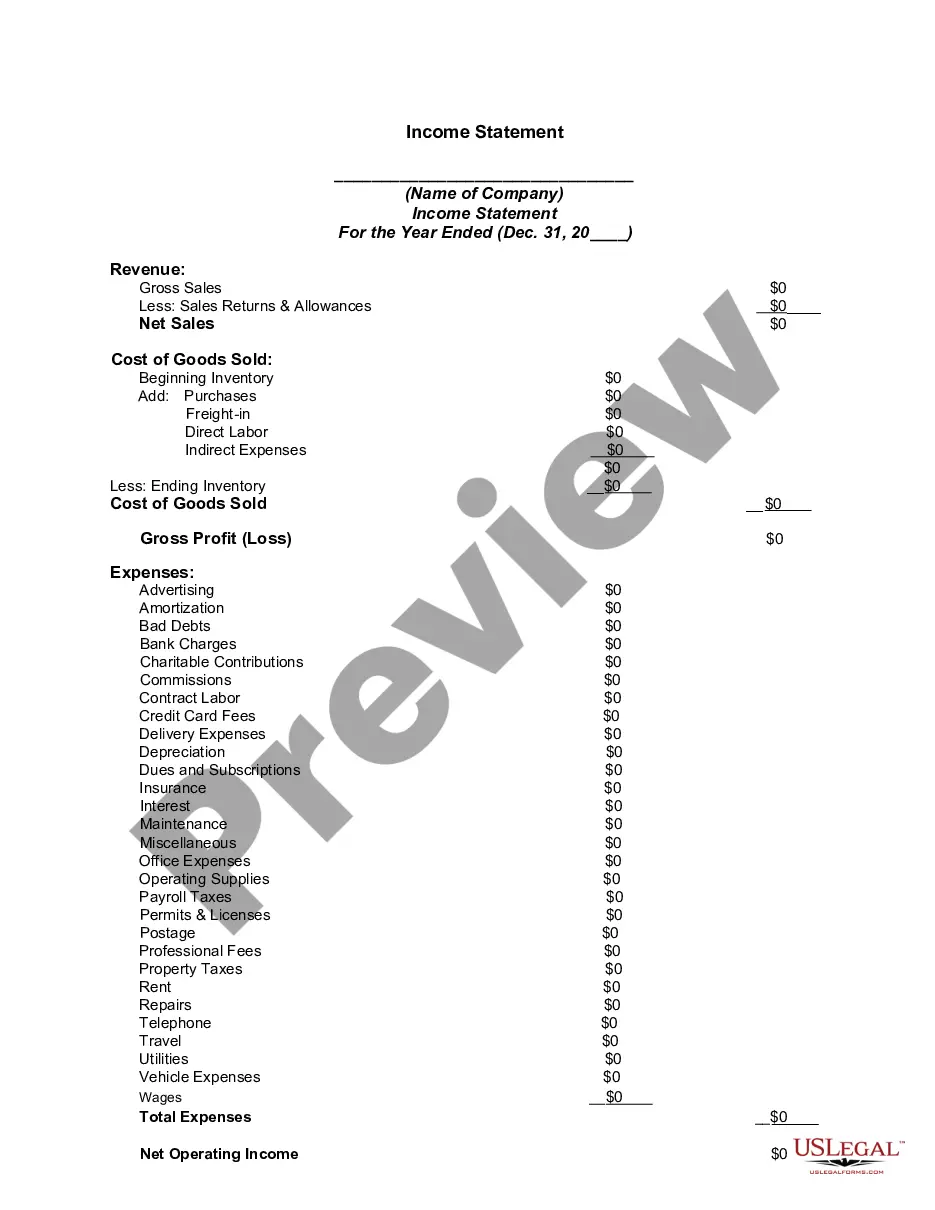

Contract. Accounts Receivable. All rights the Company has now or in the future to payments including, but not limited to, payment for goods and other property sold or leased or for services rendered, whether or not the Company has earned such payment by performance.

The 10% Rule specifically suggests that if 10% or more of a customer's receivables are significantly overdue, all receivables from that customer may be considered high-risk.

Therefore, when a journal entry is made for an accounts receivable transaction, the value of the sale will be recorded as a credit to sales. The amount that is receivable will be recorded as a debit to the assets. These entries balance each other out.

Record the total debit amount in the accounts receivable account ing to the invoice. When the customer pays the invoice in full, post a debit in the sales account. This helps balance the double-entry system, which can help you avoid accounting errors and balance books more effectively.