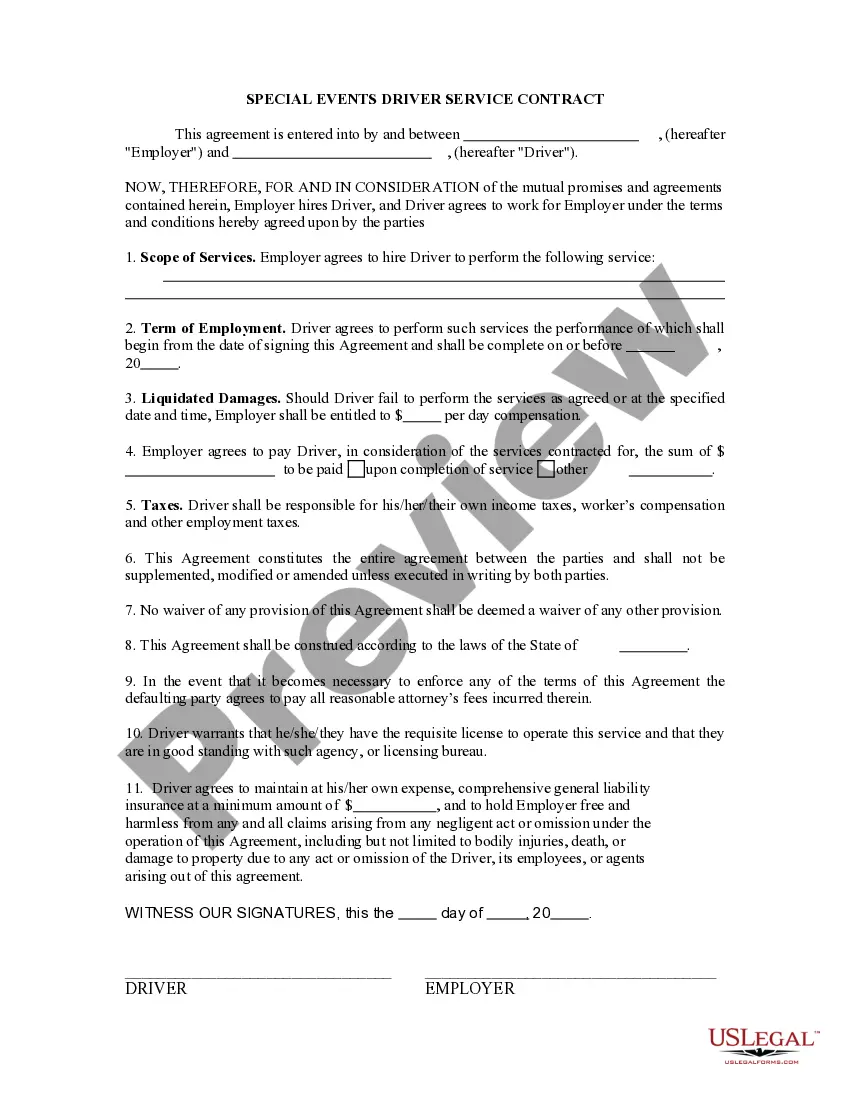

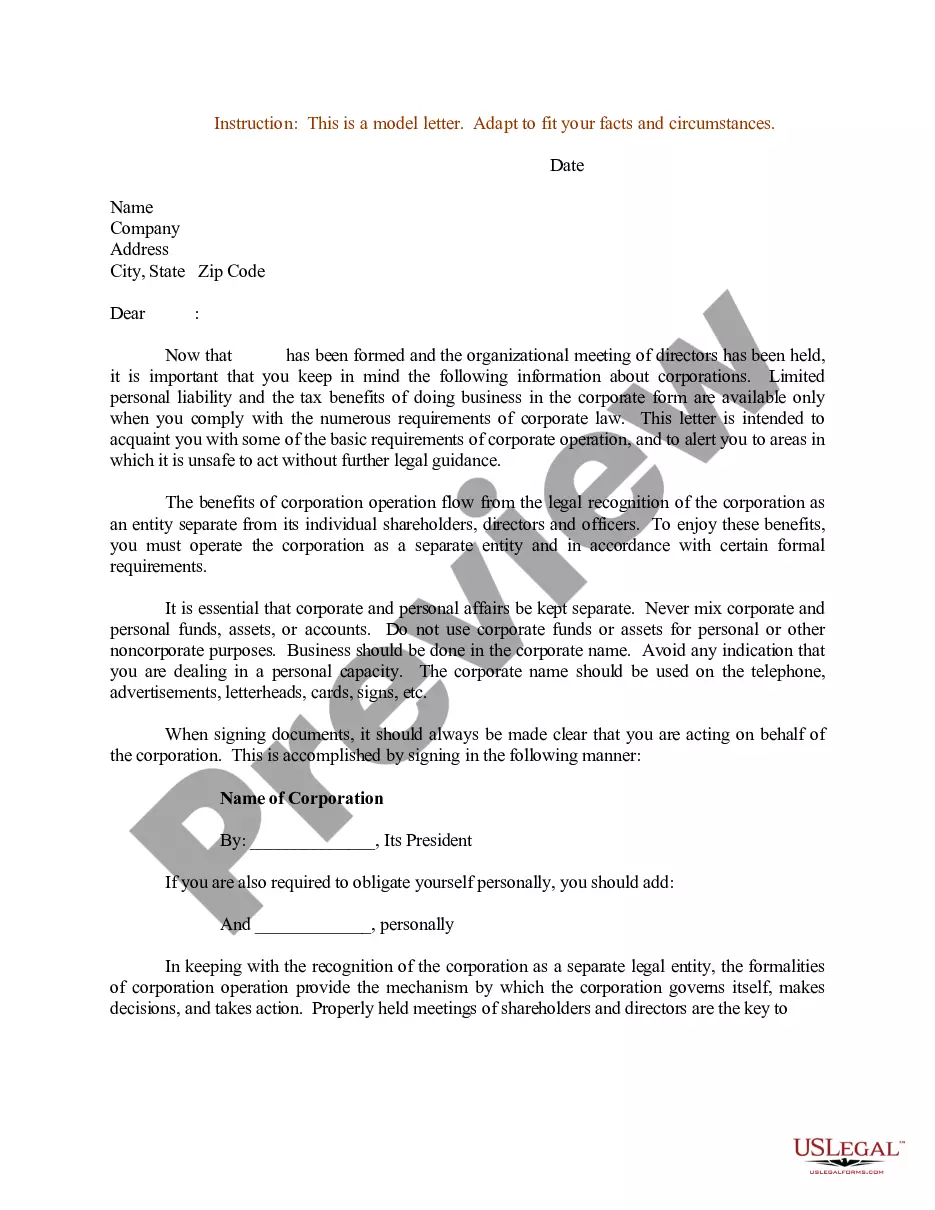

Equity Share Statement With Interest In Utah

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

To submit the Utah Corporation Franchise Tax Return, you can send it by mail to the Utah State Tax Commission at 210 North 1950 West, Salt Lake City, UT 84134-2000. You may also submit the tax return electronically through approved e-filing services.

If you have income from capital gains from equity shares, mutual funds, or house property, you need to show it in the income tax return. Taxpayers with capital gains income must select ITR-2 while filing an income tax return for AY2024-25.

Sell appreciated assets in a tax-exempt trust: You can minimize your taxable capital gains by moving appreciated assets into a tax-exempt trust – a Charitable Remainder Trust, for example – before you sell.

Instead, it taxes all capital gains as ordinary income, using the same rates and brackets as the regular state income tax: Utah is one of the states with a flat income tax rate, so no matter the amount of taxable ordinary income, the state tax rate will always be 4.65%.

Nine states have no state income tax on individual income at all. Eight of them – Alaska, Florida, Nevada, South Dakota, Tennessee, Texas, Washington and Wyoming – don't tax wages, salaries, dividends, interest or any sort of income.

A copy of the IRS letter of authorization, “Notice of Acceptance as an S Corporation,” must be at- tached to the S Corporation Franchise or Income Tax Return, TC-20S, when filing for the first time. and Tax Commission Master File Maintenance 210 N 1950 W Salt Lake City, UT 84134.

In Utah, groceries are not subject to state sales tax. This means that any food items purchased for home consumption, including meats, dairy products, fruits, vegetables, and canned goods, are exempt from sales tax.

For a Utah net loss carried forward to a taxable year beginning on or after January 1, 2023, the amount of Utah net loss that a taxpayer may carry forward to a taxable year may not exceed 80% of Utah taxable income calculated before deducting any Utah net loss from Utah taxable income.

Types of partnerships: Liability & tax considerations Utah does require a yearly partnership return from each partnership within the state.

At the federal level, businesses can carry forward their net operating losses indefinitely, but the deductions are limited to 80 percent of taxable income. Prior to the Tax Cuts and Jobs Act (TCJA) of 2017, businesses could carry losses forward for 20 years (without a deductibility limit).