Financed House Lend Formation In Suffolk

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

Form popularity

FAQ

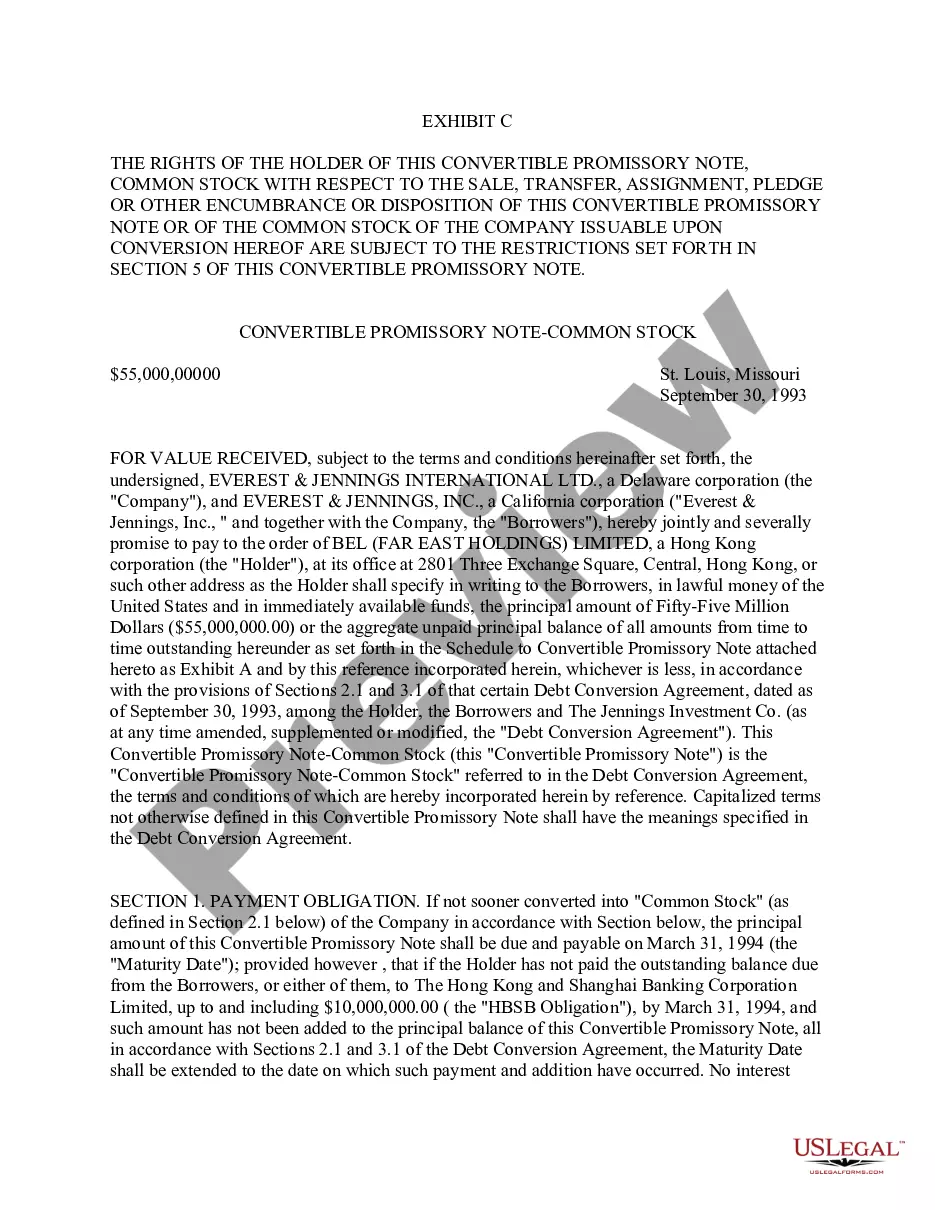

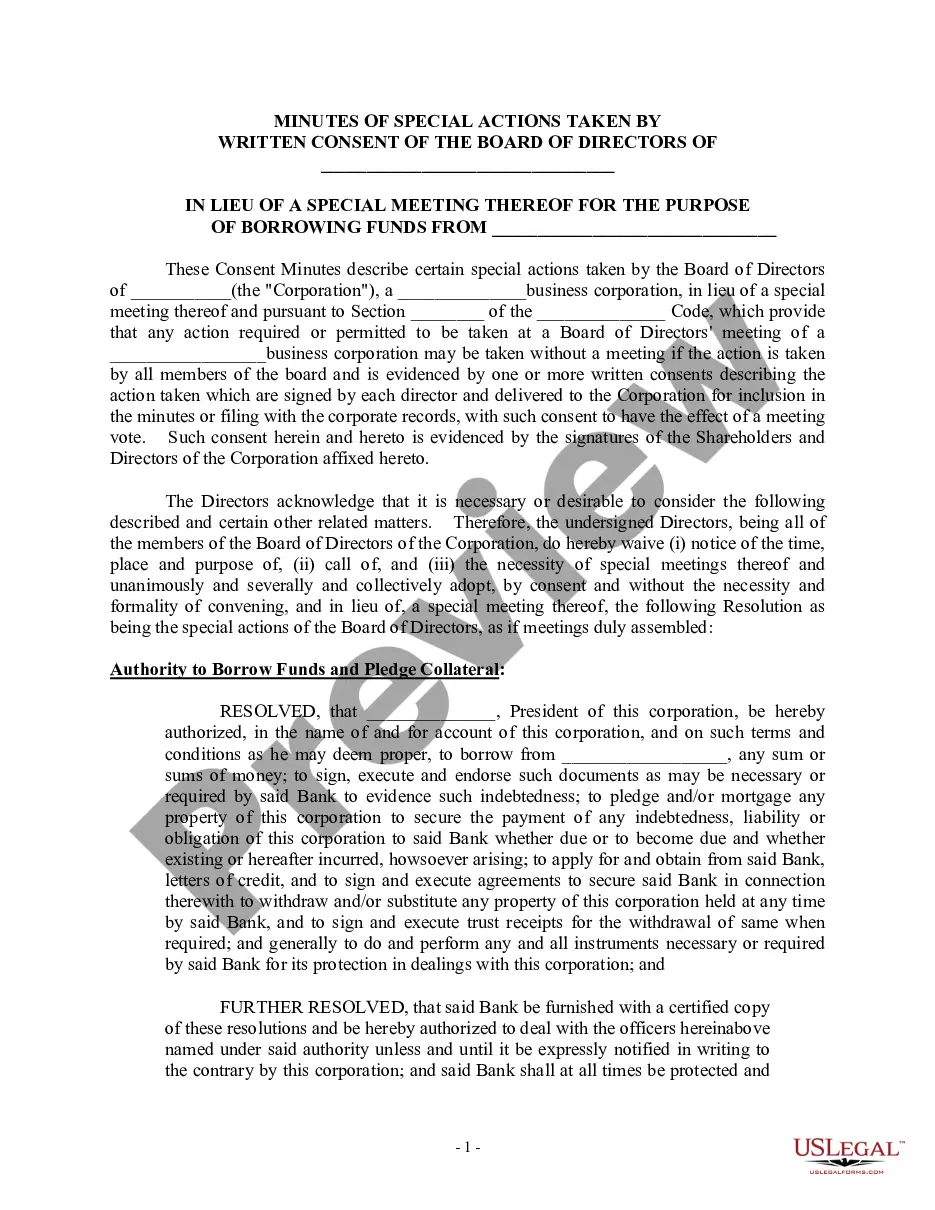

The grantor must sign the deed form and that signature must be properly acknowledged by a notary public. All signatures must be original; we cannot accept photocopies. A complete description of the property including the village, town, county and state where the property is located must also be included on the form.

Transfer Tax is due on all conveyances with consideration greater than $500.00. The amount of tax is computed at $2.00 per $500.00, or any fraction thereof. (Example: $750.00; Consideration = $4.00 tax.) Mansion Tax is due on all residential conveyances where the consideration is $1,000,000.00 or greater.

Whatever the reason, you will need to retain an attorney, experienced in real estate, to draft a new deed conveying (i.e., transferring) your home to yourself and the person you wish to add to your title. In addition to the deed, your attorney will also need to prepare transfer tax returns.

Deeds should be recorded in the Office of the County Clerk of the county in which the real property being transferred is located. When recording a deed, it is your responsibility to take the proper steps to ensure that the document meets the legal requirements for recording.

Recording Fees Document TypeFee Declaration of Trust $255 Deed, Unit Deed, or Easement $155 Mortgage $205 Mortgage Foreclosure Deed & Affidavit $1559 more rows

FHLB Welcome Home Program Mortgage Eligibility & Qualification Requirements. To qualify for the grant: Your total household income must be at or below 80% of the Mortgage Revenue Bond (MRB) limit for the county and state where the property is located.

Getting approved for a mortgage can be tough — lenders review every aspect of your finances, including your income, credit history and outstanding debts. CNBC Select compared more than a dozen mortgage companies and compiled a list of the easiest mortgages to qualify for.

Interest Rates: In-house financing may have higher interest rates compared to traditional loans. This is because the seller or dealership is taking on more risk by providing financing directly to the buyer. Traditional loans are typically offered at lower interest rates, as they are backed by financial institutions.

Compared to traditional car loans, in-house loans are much easier to qualify for. The dealership sets its own eligibility requirements instead of following those of a bank or finance company. An in-house financing dealership might not run your credit at all.