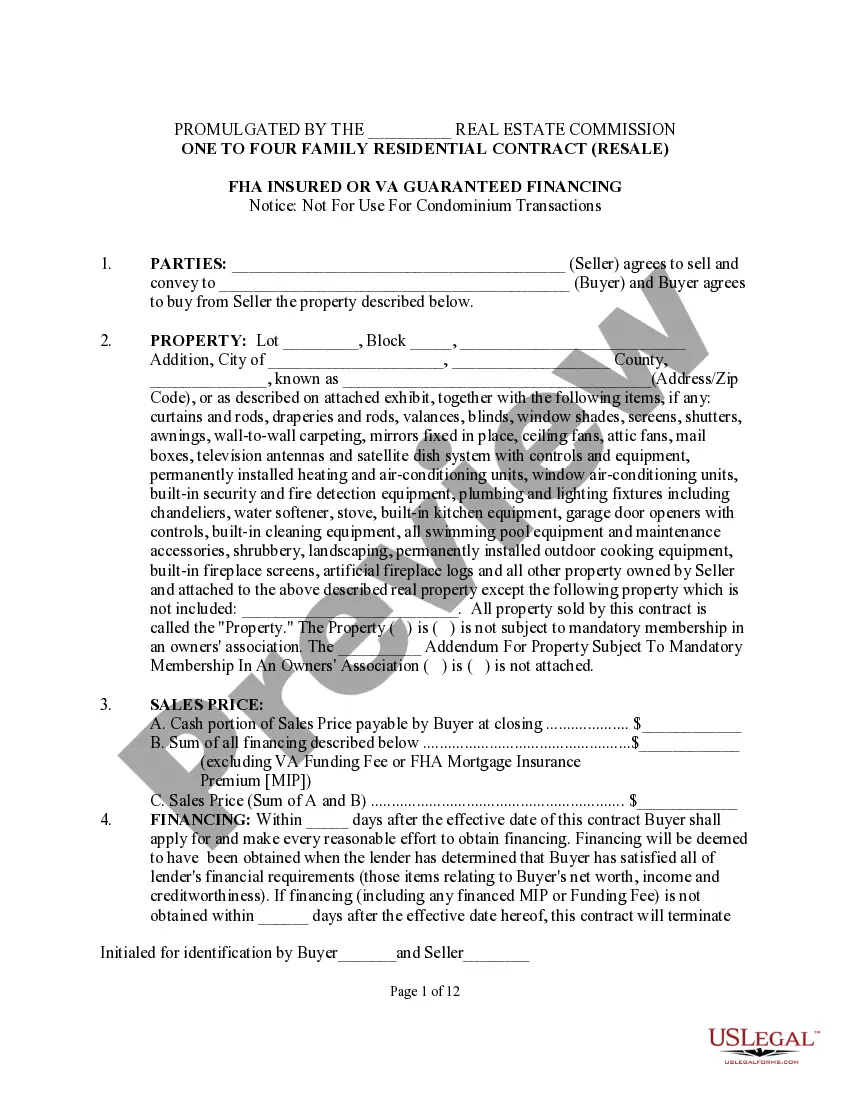

Residential Seller Financing Foreclosure

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Texas One To Four Family Residential Contract - Resale - All Cash, Assumption, Third Party Conventional Or Seller Financing?

The Residential Seller Financing Foreclosure displayed on this page is a versatile legal template created by expert attorneys in accordance with federal and local regulations.

For over 25 years, US Legal Forms has offered individuals, businesses, and legal professionals more than 85,000 validated, state-specific documents for any business and personal situation. It’s the fastest, easiest, and most reliable method to acquire the paperwork you require, as the service ensures the utmost level of data protection and anti-malware safeguards.

Sign up for US Legal Forms to have authenticated legal templates for all of life’s situations at your service.

- Search for the document you require and examine it.

- Scan through the file you sought and preview it or review the form details to confirm it meets your requirements. If it doesn’t, utilize the search feature to locate the suitable one. Click Buy Now once you have identified the template you need.

- Register and Log In.

- Select the payment plan that suits you and set up an account. Use PayPal or a credit card for a swift transaction. If you already possess an account, Log In and verify your subscription to proceed.

- Obtain the editable template.

- Choose the format you desire for your Residential Seller Financing Foreclosure (PDF, Word, RTF) and download the sample to your device.

- Complete and sign the documents.

- Print the template to fill it out manually. Alternatively, use an online multifunctional PDF editor to swiftly and accurately complete and sign your form with an eSignature.

- Download your documents once more.

- Reutilize the same document whenever necessary. Access the My documents tab in your profile to redownload any previously acquired forms.

Form popularity

FAQ

Limited Recourse ? If the Borrower fails to pay, the Seller must foreclose. In many States including California, Seller Financers are barred from suing the Borrower if they are not paid back in full.

Examples of seller financing are all-inclusive mortgages, rent-to-own agreements, second mortgages or junior mortgages, wrap-around agreements, and land contracts.

How Do You Structure a Seller Financing Deal? Don't use current market interest rates to create the interest rate for your seller financing loan. ... The higher the price?the longer the loan term. ... Bring as little cash to the deal as possible. ... Defer payments if possible. ... Exchange down payment for needed repairs.

Disadvantages Of Seller Financing Buyers still vulnerable to foreclosure if seller doesn't make mortgage payments to senior financing. No home inspection/PMI may result in buyer paying too much for the property. Higher interest rates and bigger down payment required.

Here's a quick look at some of the most common types of seller financing. All-inclusive mortgage. In an all-inclusive mortgage or all-inclusive trust deed (AITD), the seller carries the promissory note and mortgage for the entire balance of the home price, less any down payment. Junior mortgage.