Transfer Death Individual Within 2 Years Iht

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

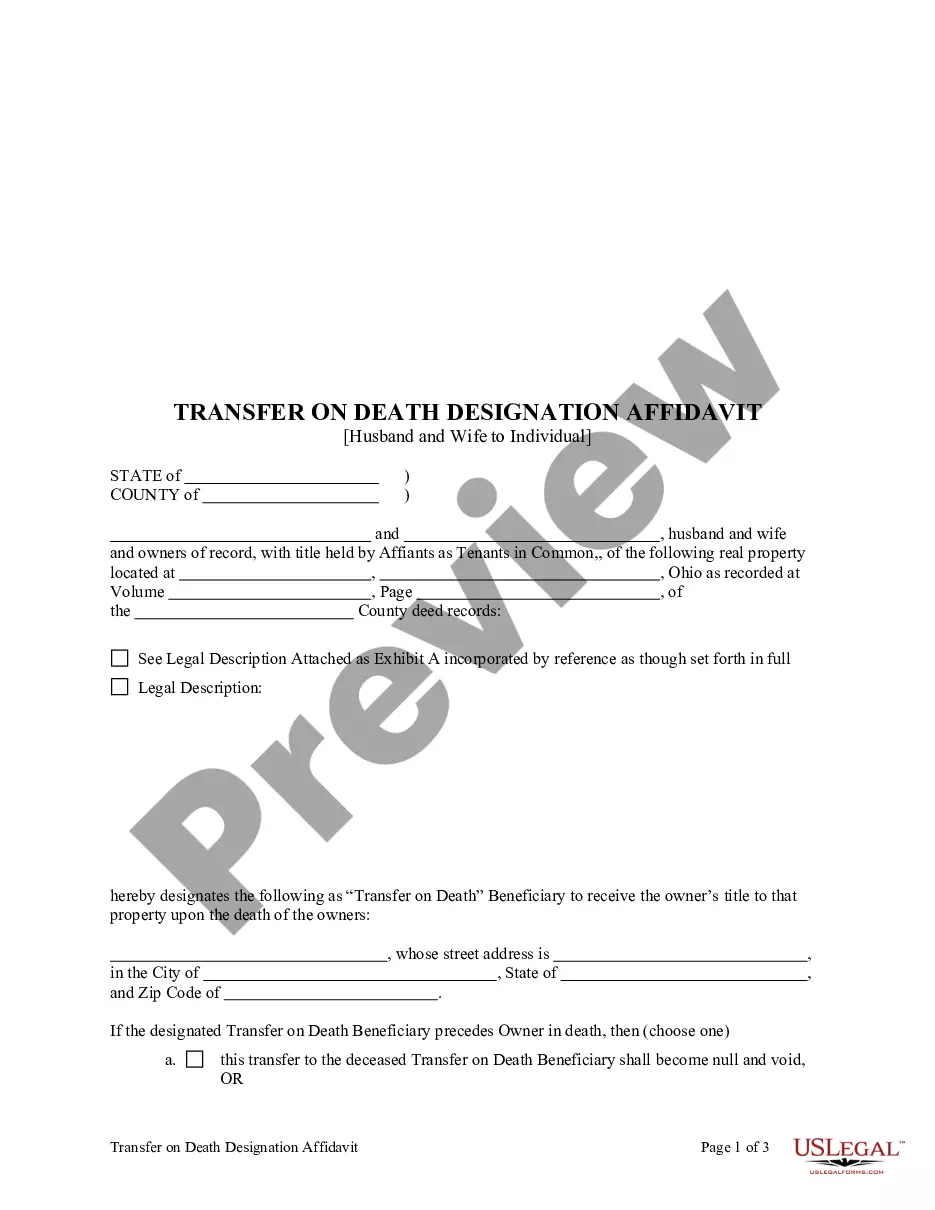

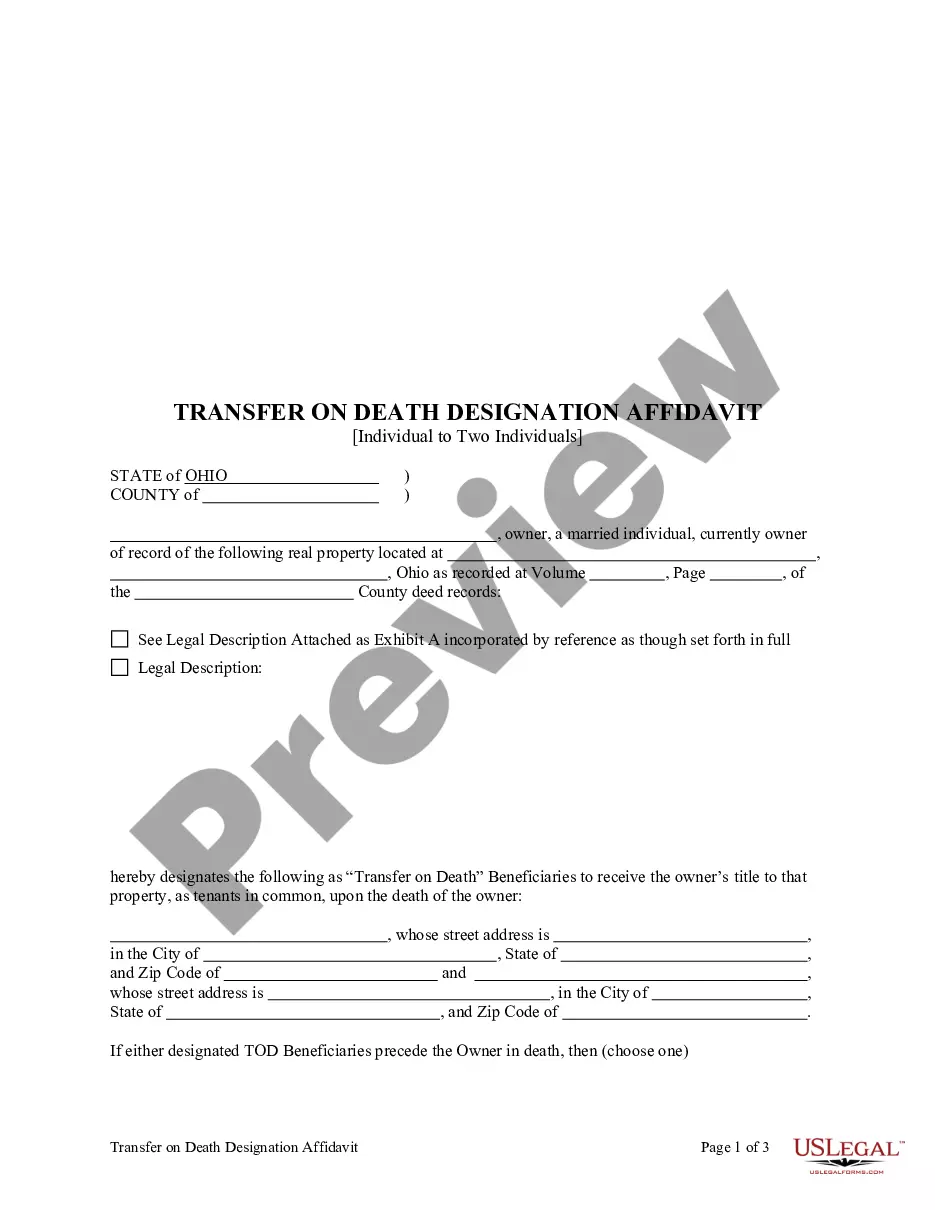

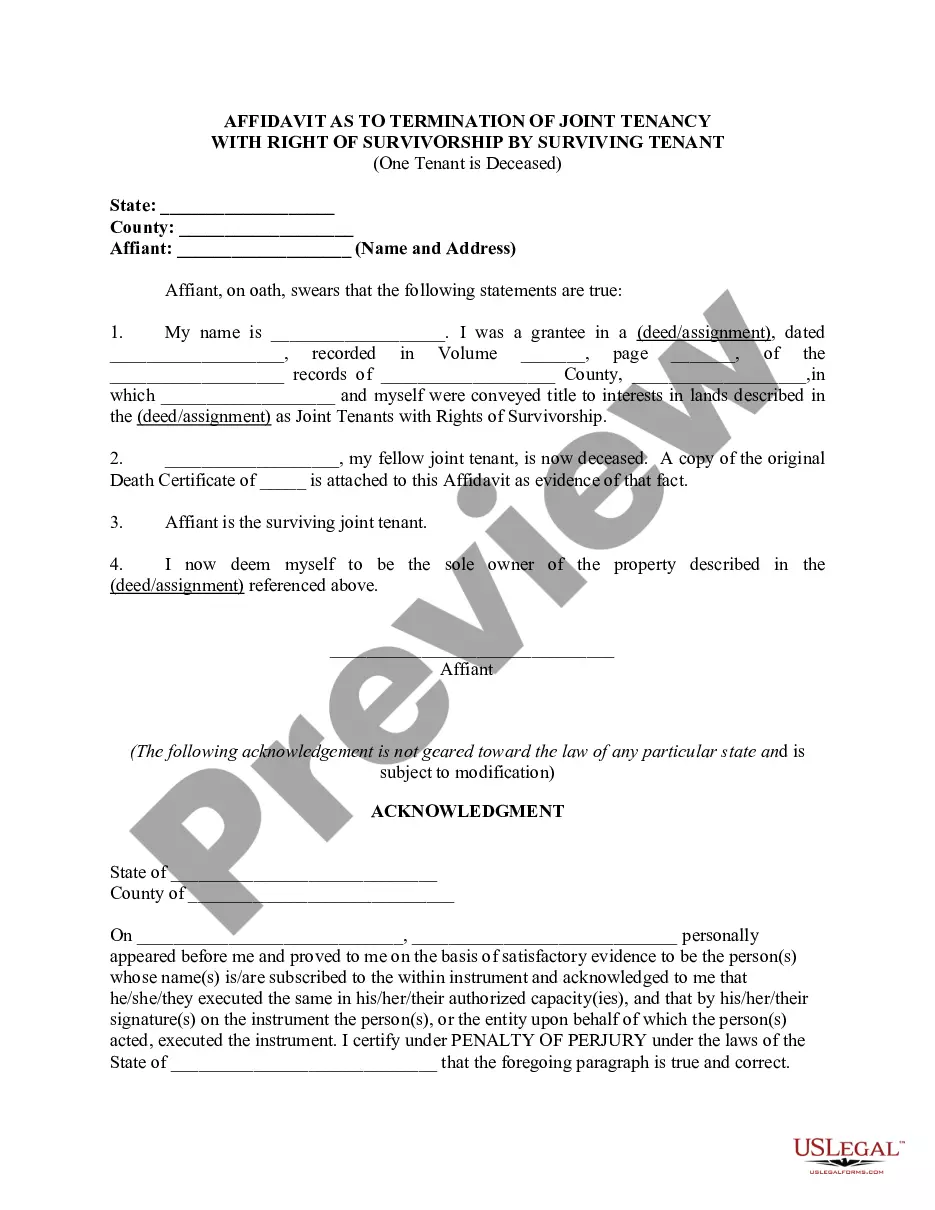

How to fill out Ohio Transfer On Death Designation Affidavit - TOD From Two Individuals To One Individual?

It’s widely acknowledged that one cannot become a legal authority instantly, nor can you swiftly learn to prepare Transfer Death Individual Within 2 Years Iht without a specialized background.

Compiling legal documents is a lengthy process necessitating particular education and expertise. So why not entrust the formulation of the Transfer Death Individual Within 2 Years Iht to the professionals.

With US Legal Forms, featuring one of the largest libraries of legal templates, you can obtain anything from judicial documents to templates for in-office correspondence. We recognize the importance of compliance with federal and state statutes and regulations. Therefore, all forms on our platform are specific to your location and current.

You can retrieve your forms from the My documents section at any moment. If you’re a returning client, you can simply Log In and locate and download the template from the same section.

Regardless of the reason for your documentation—be it financial and legal, or personal—our platform can assist you. Experience US Legal Forms today!

- Locate the form you require by utilizing the search bar located at the top of the page.

- Preview it (if this feature is available) and review the accompanying description to ascertain whether Transfer Death Individual Within 2 Years Iht is what you are seeking.

- Restart your search if you need a different form.

- Create a free account and select a subscription plan to acquire the form.

- Select Buy now. Once your payment is processed, you can obtain the Transfer Death Individual Within 2 Years Iht, fill it out, print it, and send or mail it to the appropriate individuals or organizations.

Form popularity

FAQ

The executor or administrator of the estate will usually claim to transfer unused nil rate band and they usually have 2 years to make that claim. If they do not make a claim then if you're liable for any tax due to the person's death you can make a claim.

When you have got a good idea about the assets that make up the estate, and their values, add up the figures. If the gross value of all the assets is less than £100,000, continue to fill in form IHT207. do not fill in form IHT207 - you will need to fill in form IHT400.

HMRC should not be contacted on first death to agree the transferable NRB. When the claim is made after second death, the appropriate form is provided by HMRC IHT402. The time limit for claiming is generally 24 months from the end of the month in which the surviving spouse died.

Broadly, a gift from one individual to another is a PET. An everyday example is where a parent makes a cash gift to an adult child. The person making the gift is the 'donor' or 'transferor' and the recipient is the 'donee' or 'transferee'.

You must complete the form IHT400, as part of the probate or confirmation process if there's Inheritance Tax to pay, or the deceased's estate does not qualify as an 'excepted estate'.