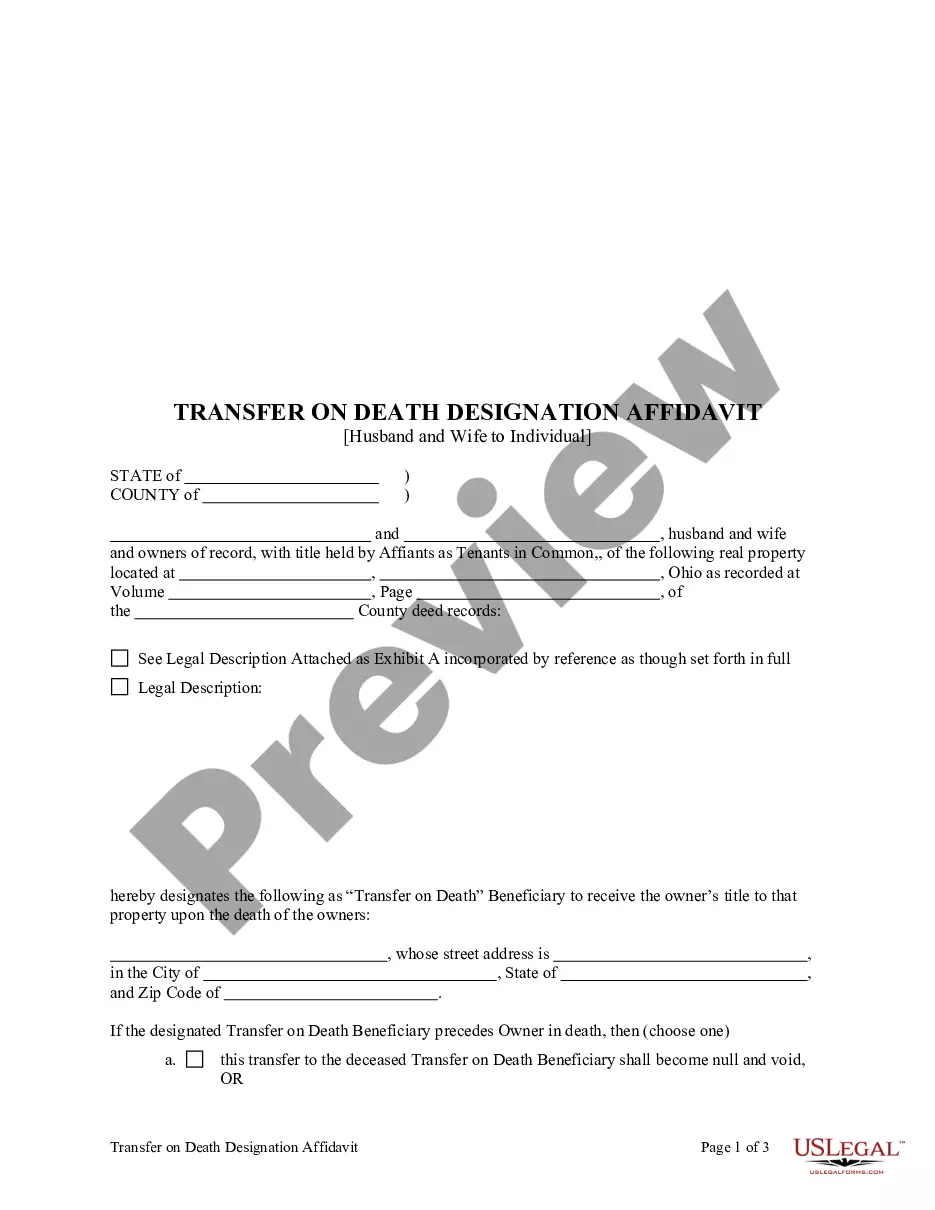

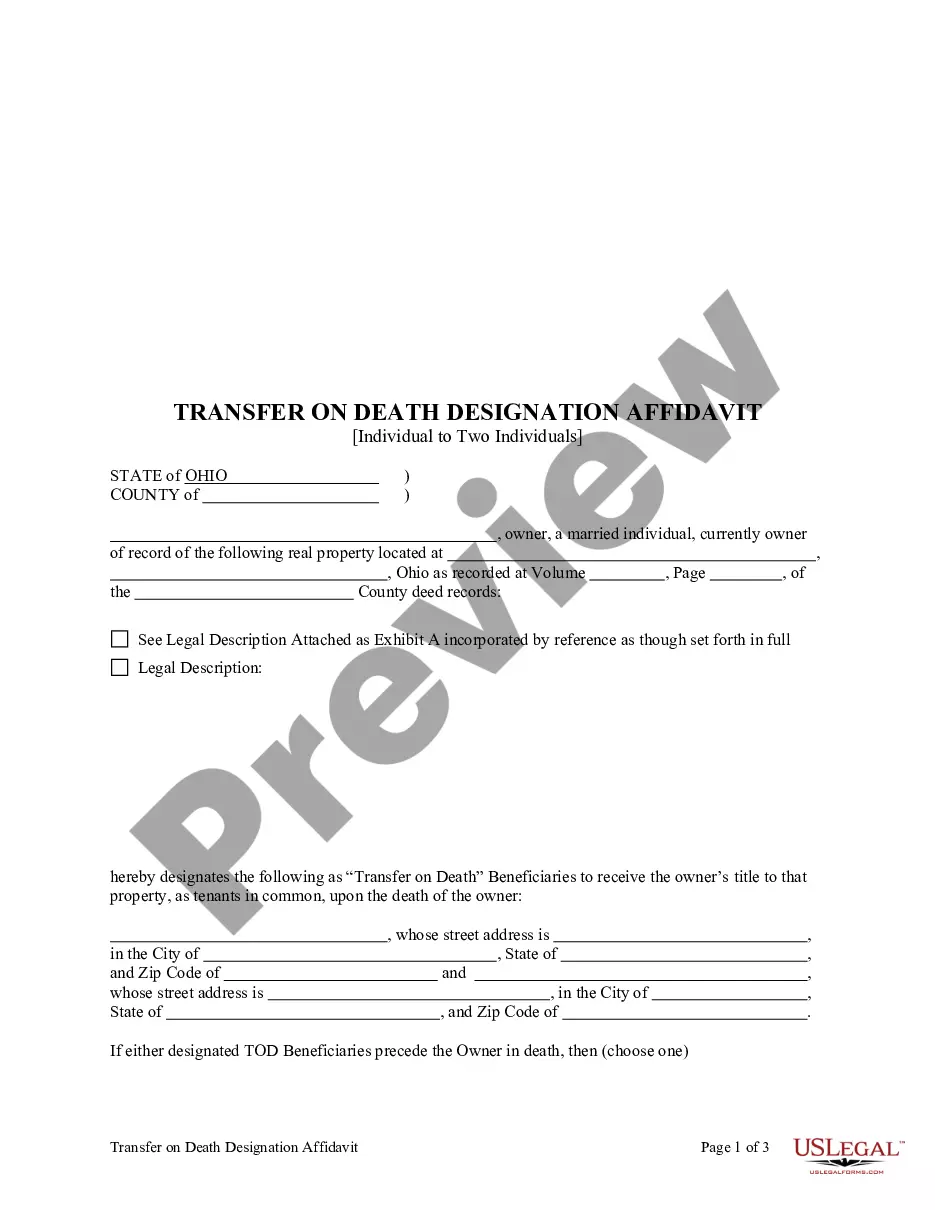

Transfer Death Individual For Each Other

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Ohio Transfer On Death Designation Affidavit - TOD From Two Individuals To One Individual?

- If you’re a returning user, log in to your account and select the desired form template for download by clicking the Download button. Ensure your subscription is active; if not, renew it according to your plan.

- For first-time users, start by previewing the form description carefully. Confirm that you’ve selected the right document suitable for your needs and compliant with local jurisdiction requirements.

- If you need a different template, utilize the Search feature to find the correct one. Once identified, proceed to the next step.

- Complete your purchase by clicking on the Buy Now button and selecting a suitable subscription plan. An account registration is required to gain access to the resource library.

- Finalize your purchase by entering your credit card information or using PayPal for payment.

- Download the form and save it on your device. You can access it anytime through the My Forms section in your profile.

By utilizing US Legal Forms, you can effortlessly manage the transfer of death individual for each other, ensuring accurate and legally valid documents.

Don’t hesitate—start your journey with US Legal Forms today to streamline your legal documentation process.

Form popularity

FAQ

The choice between a transfer on death (TOD) and naming a beneficiary depends on your specific situation. A TOD may be more efficient for certain assets, providing a straightforward transfer process. However, naming a beneficiary may be preferable for financial accounts, as it can help avoid the probate process altogether. To determine which is better for you and learn how to transfer death individual for each other effectively, consider consulting platforms like US Legal Forms for tailored guidance.

The key difference lies in how the asset is handled after death. A transfer on death (TOD) facilitates the automatic transfer of specific assets to designated individuals upon your passing. In contrast, a beneficiary is a person or entity named to receive benefits from certain contracts or policies, like life insurance. By understanding how to transfer death individual for each other, you can identify the best options for your estate strategy.

While a transfer on death (TOD) can designate a beneficiary, it is not the same in all respects. A TOD allows for direct transfer of assets without going through probate, while a beneficiary designation typically refers to financial accounts or insurance policies. Understanding how to transfer death individual for each other can help you make informed decisions regarding your estate. Thus, clarity on these terms is critical for effective estate planning.

One downside of a transfer on death (TOD) is that it may not avoid probate in certain situations, especially if the asset ownership is unclear. Additionally, if you transfer death individual for each other without clear communication, it can create confusion among family members. Furthermore, this option does not provide any tax benefits that might accompany other estate planning strategies. It's essential to consider all your options before deciding.

While TOD accounts offer numerous benefits, they also have some disadvantages. One key issue is that they may not effectively address complex estate situations. Additionally, a TOD account does not provide protection against creditors, which means assets could still be claimed by creditors after death. It's essential to weigh these disadvantages and consider consulting with a professional for tailored advice.

You do not necessarily need a lawyer to create a transfer on death account. Many financial institutions allow you to establish a TOD designation on your own. However, consulting a lawyer can provide valuable insights into your specific situation and ensure that your documentation is correctly completed. Ultimately, considering legal guidance can help avoid any potential issues down the line.

An individual transfer on death means that a specific person, usually a beneficiary, automatically receives your assets when you pass away. This transfer occurs outside the probate process, simplifying the transition of assets. In essence, it streamlines the process of transferring ownership, ensuring that your wishes are honored efficiently. This can be particularly beneficial if you desire to transfer death individual for each other without complications.

Transfer on death accounts can be a smart financial choice. They allow you to pass assets directly to your beneficiaries upon your death, bypassing probate. This means your loved ones receive their inheritance faster and with less hassle. However, it's essential to consider your individual circumstances and goals before deciding if a TOD account is right for you.

Deciding between a TOD account and a beneficiary designation depends on your personal circumstances. A TOD account provides a straightforward transfer, avoiding probate, while a beneficiary designation offers more comprehensive estate planning options. Evaluating your goals and potential family dynamics is crucial, and using uslegalforms can help navigate these choices effectively.

Generally, a transfer on death account is not taxable as income for the account holder. However, any earnings generated within the account may be subject to income tax until distribution. Beneficiaries typically do not face immediate tax obligations upon receiving the transfer. To understand the specific implications in your situation, consider reviewing resources available on uslegalforms.