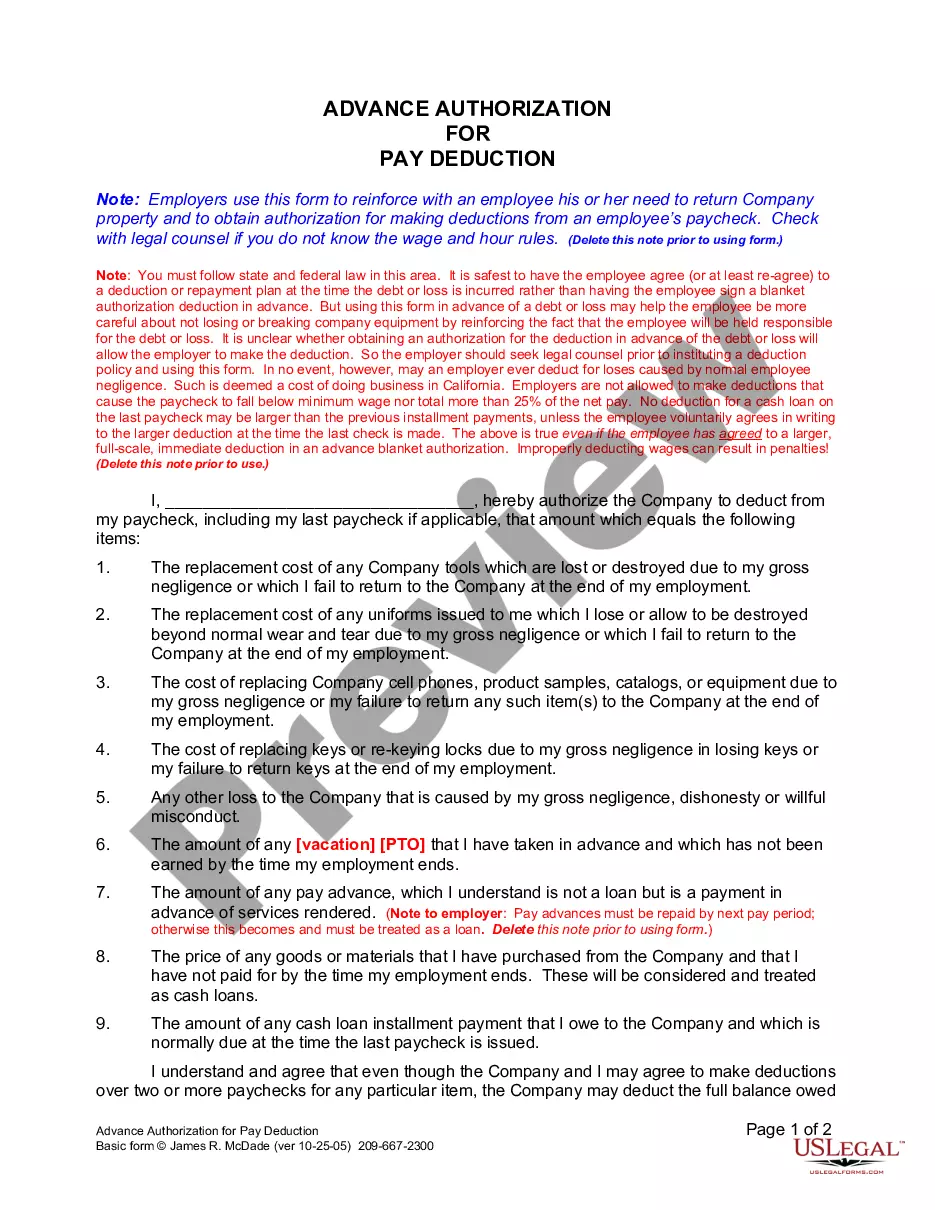

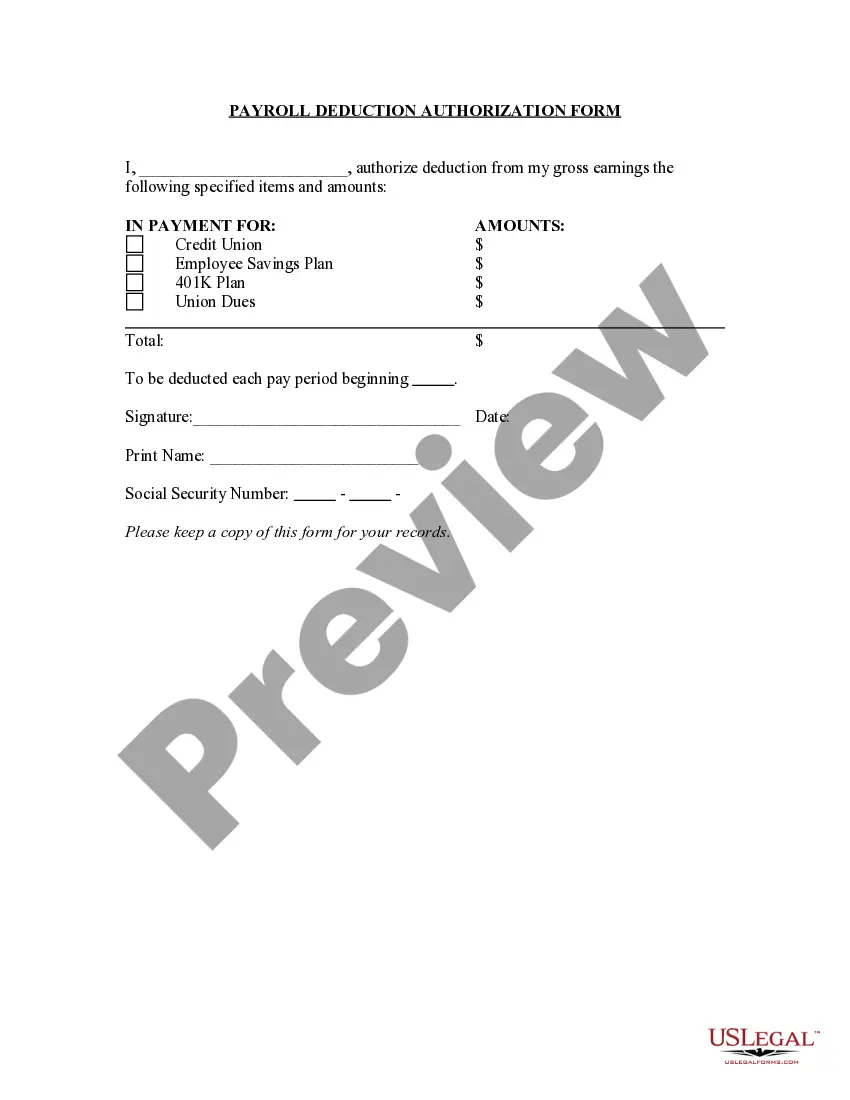

Deductible Pay For Insurance

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out California Authorization For Deduction From Pay For A Specific Debt?

Creating legal documents from the ground up can occasionally be overwhelming.

Certain situations may require extensive investigation and significant financial investment.

If you’re looking for a more straightforward and cost-effective method of drafting Deductible Pay For Insurance or any other documents without facing unnecessary challenges, US Legal Forms is readily available to you.

Our online library of over 85,000 current legal forms addresses nearly every aspect of your financial, legal, and personal matters. With a few clicks, you can swiftly obtain state- and county-compliant templates meticulously compiled by our legal experts.

Examine the document preview and descriptions to ensure you have identified the correct document. Confirm that the form you select satisfies the criteria of your state and county. Choose the most appropriate subscription plan to obtain the Deductible Pay For Insurance. Download the document, and then complete, sign, and print it out. US Legal Forms has an impeccable track record and over 25 years of expertise. Join us today and simplify the process of form execution!

- Utilize our service whenever you require dependable and trustworthy solutions that enable you to quickly find and download the Deductible Pay For Insurance.

- If you’re an existing user and have already registered with us, simply sign in to your account, choose the template, and download it right away or re-download it later in the My documents section.

- New to our site? No problem! It takes minimal time to create an account and explore the library.

- However, before diving directly into downloading the Deductible Pay For Insurance, keep these tips in mind.

Form popularity

FAQ

Choosing between a $500 or $1000 deductible depends on your financial situation and risk tolerance. A lower deductible means you will pay less out of pocket when making a claim, but it also leads to higher premium costs. Conversely, a higher deductible results in lower monthly payments, but you must be prepared to pay more upfront in the event of a claim. Consider your budget and how often you anticipate needing to file a claim when deciding on your deductible pay for insurance.

A deductible is the amount you need to pay out of pocket for your insurance before your coverage kicks in. For example, if you have a $1,000 deductible, you must pay that amount for services before your insurer starts to cover the costs. Understanding deductible pay for insurance is essential, as it directly impacts your overall expenses. At US Legal Forms, you can find resources that clarify how deductibles work and help you make informed choices about your insurance policy.

One of the most overlooked tax breaks is the deduction for medical expenses that exceed 7.5% of your adjusted gross income. Many people miss this benefit because they do not keep track of their medical costs throughout the year. Understanding how deductible pay for insurance can qualify for this deduction may help you claim more savings on your taxes. It's beneficial to explore every available deduction, as these can significantly impact your overall financial health.

Deciding between a $500 deductible and a $1,000 deductible for insurance depends on your financial situation and risk tolerance. A lower deductible means you will pay less out-of-pocket when filing a claim, which may provide peace of mind. However, lower deductibles often come with higher premiums, impacting your monthly budget. Assessing your deductible pay for insurance can help you balance between manageable premiums and potential out-of-pocket expenses.

Choosing between a $500 deductible and a $1,000 deductible depends on your financial situation and risk tolerance. A $500 deductible means you'll pay less out-of-pocket during a claim, but your premiums may be higher. On the other hand, a $1,000 deductible often leads to lower premiums, which could mean less overall deductible pay for insurance long term. Weighing these factors will help you make an informed choice.

An insurance deductible can be illustrated through a car insurance policy with a $1,000 deductible. If you have an accident and the repair costs are $4,000, you would pay the first $1,000, and your insurance would cover the remaining $3,000. Knowing how these deductibles work helps you navigate your deductible pay for insurance effectively.

An example of a deductible amount might be $750 for a homeowner’s insurance policy. In this scenario, you must pay the first $750 of any covered repairs or damages before your insurance starts paying. Understanding various deductible amounts helps you better manage your deductible pay for insurance and provides you with options based on your financial comfort level.

The most common deductible varies based on the type of insurance, but many health insurance plans use features like a $500 to $1,500 deductible. This means policyholders often choose a deductible within this range. Selecting the right deductible can significantly impact your deductible pay for insurance, so it's essential to consider your financial situation and healthcare needs carefully.

A deductible for insurance refers to the amount you pay out-of-pocket before your coverage kicks in. For instance, if you have a health plan with a $1,000 deductible, you will need to pay the first $1,000 of your medical expenses. Once you've met this amount, your insurance will begin to cover the costs, lessening your deductible pay for insurance. Understanding this concept is crucial for effective financial planning.