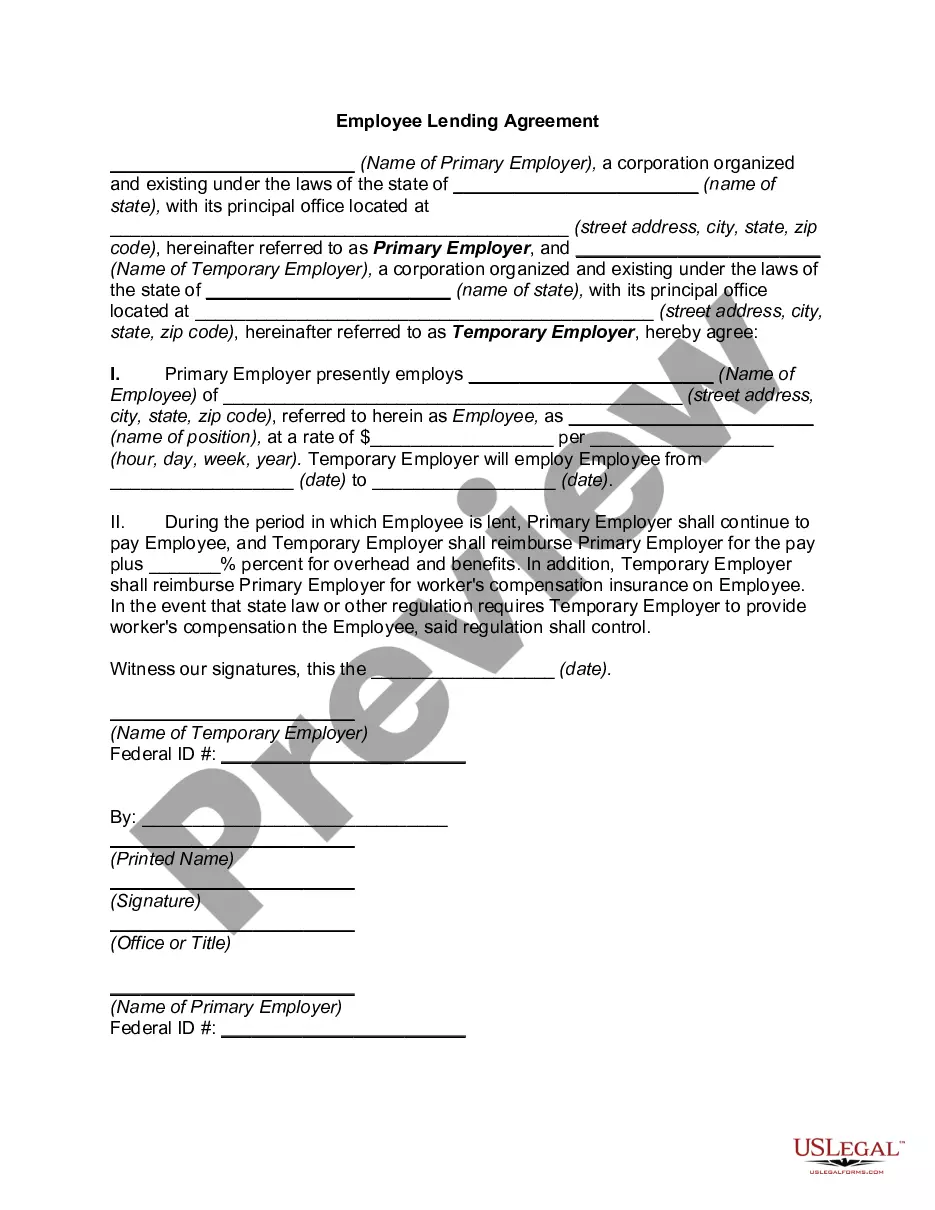

Loan Agreement for Employees

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Loan Agreement For Employees?

Use US Legal Forms to get a printable Loan Agreement for Employees. Our court-admissible forms are drafted and regularly updated by skilled lawyers. Our’s is the most extensive Forms library online and provides cost-effective and accurate templates for consumers and attorneys, and SMBs. The documents are grouped into state-based categories and a number of them might be previewed before being downloaded.

To download samples, users must have a subscription and to log in to their account. Press Download next to any template you want and find it in My Forms.

For people who do not have a subscription, follow the tips below to quickly find and download Loan Agreement for Employees:

- Check out to ensure that you get the proper form with regards to the state it is needed in.

- Review the document by reading the description and using the Preview feature.

- Press Buy Now if it’s the document you need.

- Generate your account and pay via PayPal or by card|credit card.

- Download the template to your device and feel free to reuse it multiple times.

- Make use of the Search engine if you want to get another document template.

US Legal Forms provides thousands of legal and tax samples and packages for business and personal needs, including Loan Agreement for Employees. Above three million users have used our service successfully. Choose your subscription plan and have high-quality documents in just a few clicks.

Form popularity

FAQ

Identity of the Parties. The names of the lender and borrower need to be stated. Date of the Agreement. Interest Rate. Repayment Terms. Default provisions. Signatures. Choice of Law. Severability.

The most basic loan agreement is commonly called an "IOU." These are typically used between friends or relatives for small amounts of money, and simply state the dollar amount that is owed. They do not usually say when payment is due, nor include any interest provisions.

A loan to an employee is money advanced by the company to assist the employee. If the employee is expected to repay the loan within one year of the balance sheet date, the loan balance is a current asset of the company. Any amount not expected to be collected within one year is a noncurrent or long term asset.

State laws for employee loansEmployers in the U.S. can provide loans to their employees, but may have to comply with different laws depending on your state. Some states allow employees to repay loans through payroll deductions, but only if it doesn't reduce their wages below the $7.25-per-hour federal minimum wage.

State the purpose for the loan. #Set forth the amount and terms of the loan. Your agreement should clearly state the amount of money you're lending your friend, the interest rate, and the total amount your friend will pay you back.

A 'perquisite' is a benefit offered by the employer to an employee based on his job designation. Such a benefit is considered under the head 'Salary' for tax purposes. Similarly, an interest-free or concessional loan provided by an employer is taxable as a 'perquisite' for an employee.

A loan agreement is the document in which a lender usually a bank or other financial institution sets out the terms and conditions under which it is prepared to make a loan available to a borrower.

Starting the Document. Write the date at the top of the page. Write the Terms of the Loan. State the purpose of the personal payment agreement and the terms for returning the money. Date the Document. Statement of Agreement. Sign the Document. Record the Document.

A salary, or wage, advance is a type of short-term loan from an employer to an employee. No taxes should come out of the actual advance, but you must withhold taxes from the repayment.This way, the employees' wages will be taxed as normal.