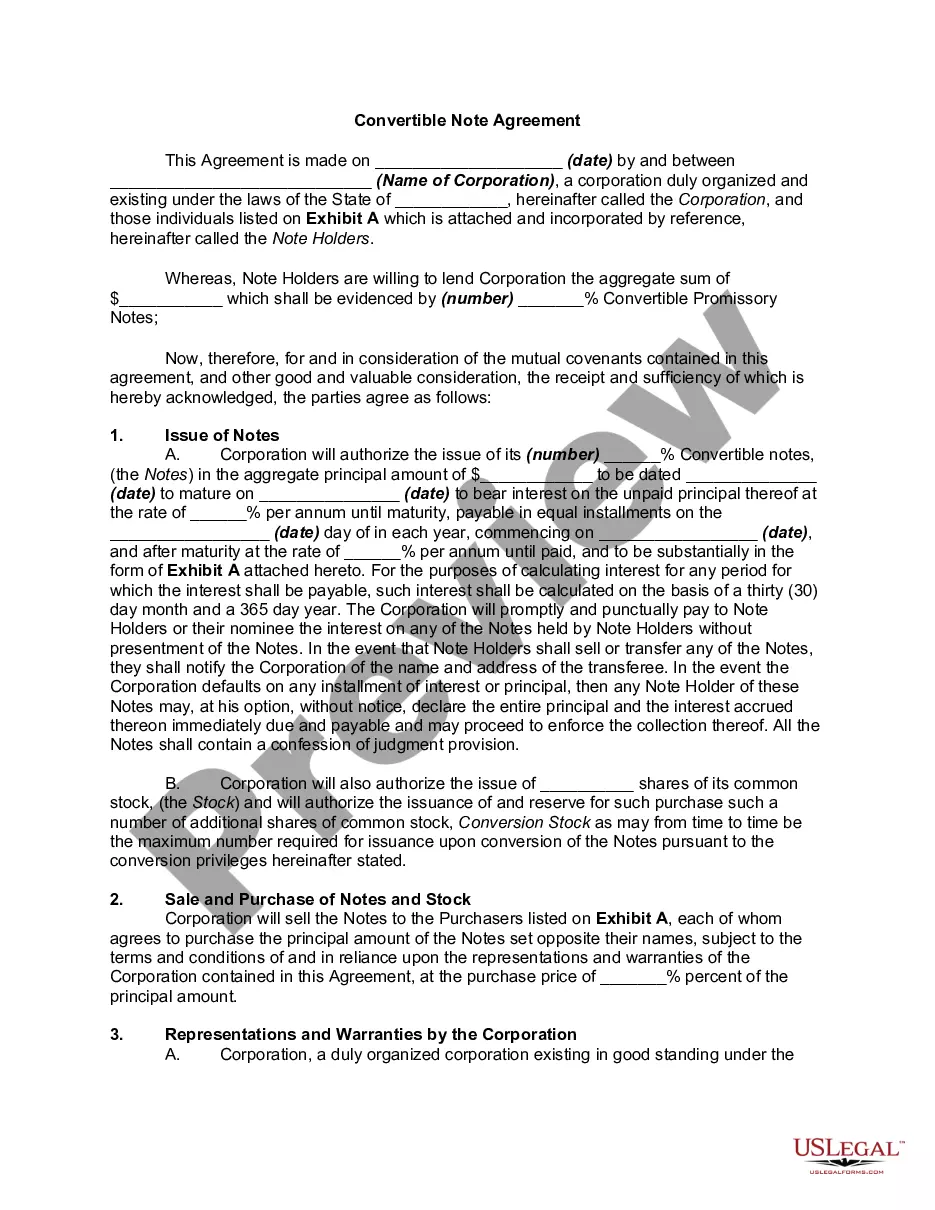

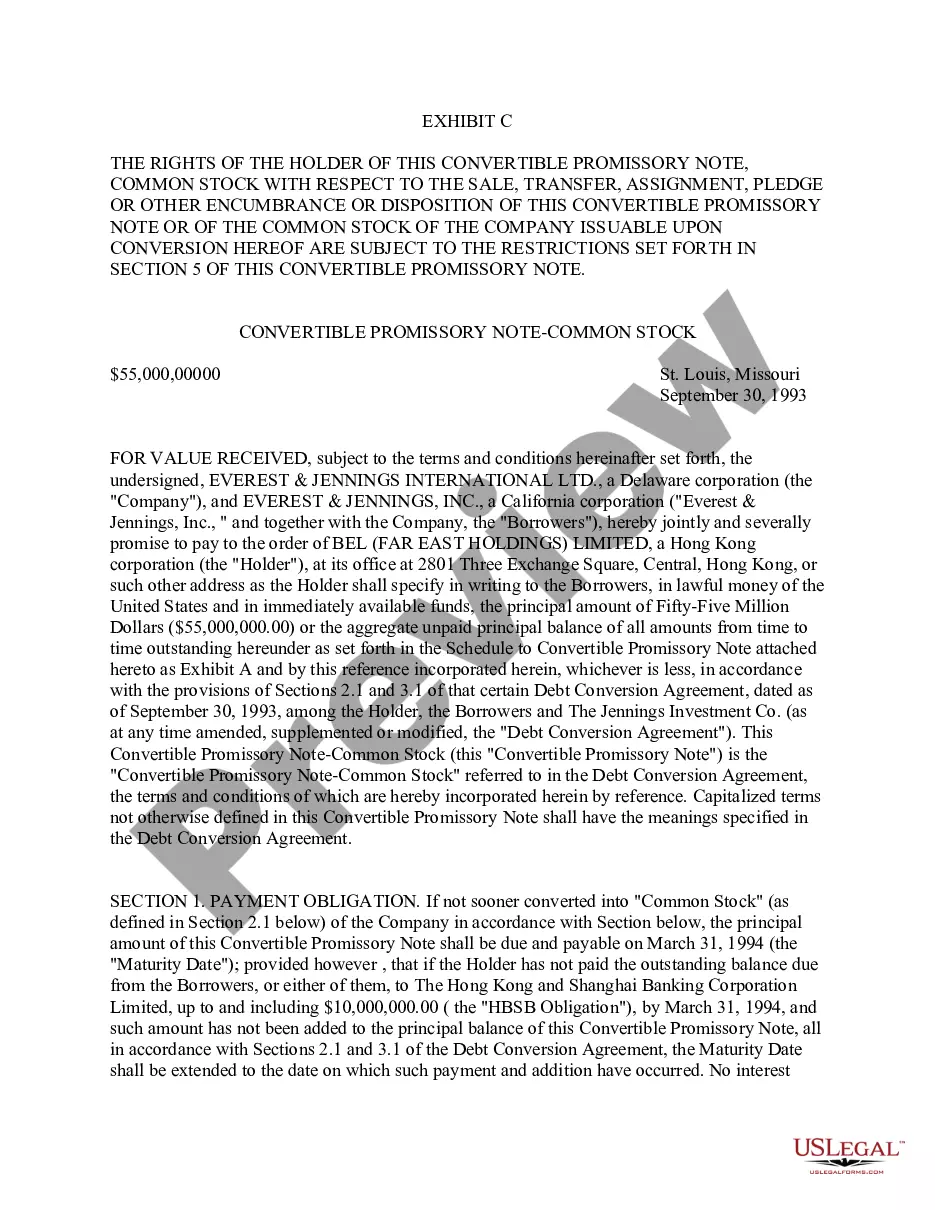

Promissory Note And Notes

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Convertible Promissory Note By Corporation - One Of Series Of Notes Issued Pursuant To Convertible Note Purchase Agreement?

Legal paperwork oversight can be daunting, even for seasoned experts.

If you're looking for a Promissory Note And Notes and lack the time to search for the correct and current version, the procedures can be stressful.

US Legal Forms caters to all your requirements, from personal to business documents, all in one location.

Employ cutting-edge tools to complete and manage your Promissory Note And Notes.

Here are the steps to follow after downloading the form you need: Verify this is the correct form by previewing it and reviewing its details. Ensure the template is valid in your state or county. Click Buy Now when you're ready. Choose a subscription plan. Select the desired format, and Download, fill out, sign, print, and send your document. Take advantage of the US Legal Forms online catalog, backed by 25 years of experience and reliability. Transform your routine document management into a straightforward and user-friendly process today.

- Access a valuable resource library of articles, guides, and manuals relating to your situation and requirements.

- Conserve time and effort by finding the documents you need, and utilize US Legal Forms’ sophisticated search and Review tool to locate and obtain Promissory Note And Notes.

- If you have a subscription, Log In to your US Legal Forms account, search for the form, and acquire it.

- Check the My documents tab to see the documents you have previously saved and to organize your folders as needed.

- If this is your first encounter with US Legal Forms, create an account and gain unlimited access to all the advantages of the library.

- An extensive online form directory could revolutionize the way anyone addresses these matters.

- US Legal Forms stands as a frontrunner in online legal documents, offering more than 85,000 state-specific legal forms available at your convenience.

- With US Legal Forms, you can access state- or county-specific legal and business forms.

Form popularity

FAQ

Promissory notes are legally binding whether the note is secured by collateral or based only on the promise of repayment. If you lend money to someone who defaults on a promissory note and does not repay, you can legally possess any property that individual promised as collateral.

The concise sample promissory note covers: proper identification of the parties. basic repayment terms ? interest, payment dates, place of payment, etc. optional default and confession of judgment provisions. repayment ledger.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

A promissory note must include the date of the loan, the loan amount, the names of both the lender and borrower, the interest rate on the loan, and the timeline for repayment. Once the document is signed by both parties, it becomes a legally binding contract.

At its most basic, a promissory note should include the following things: Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.