Secured Loan For Mortgage

Description

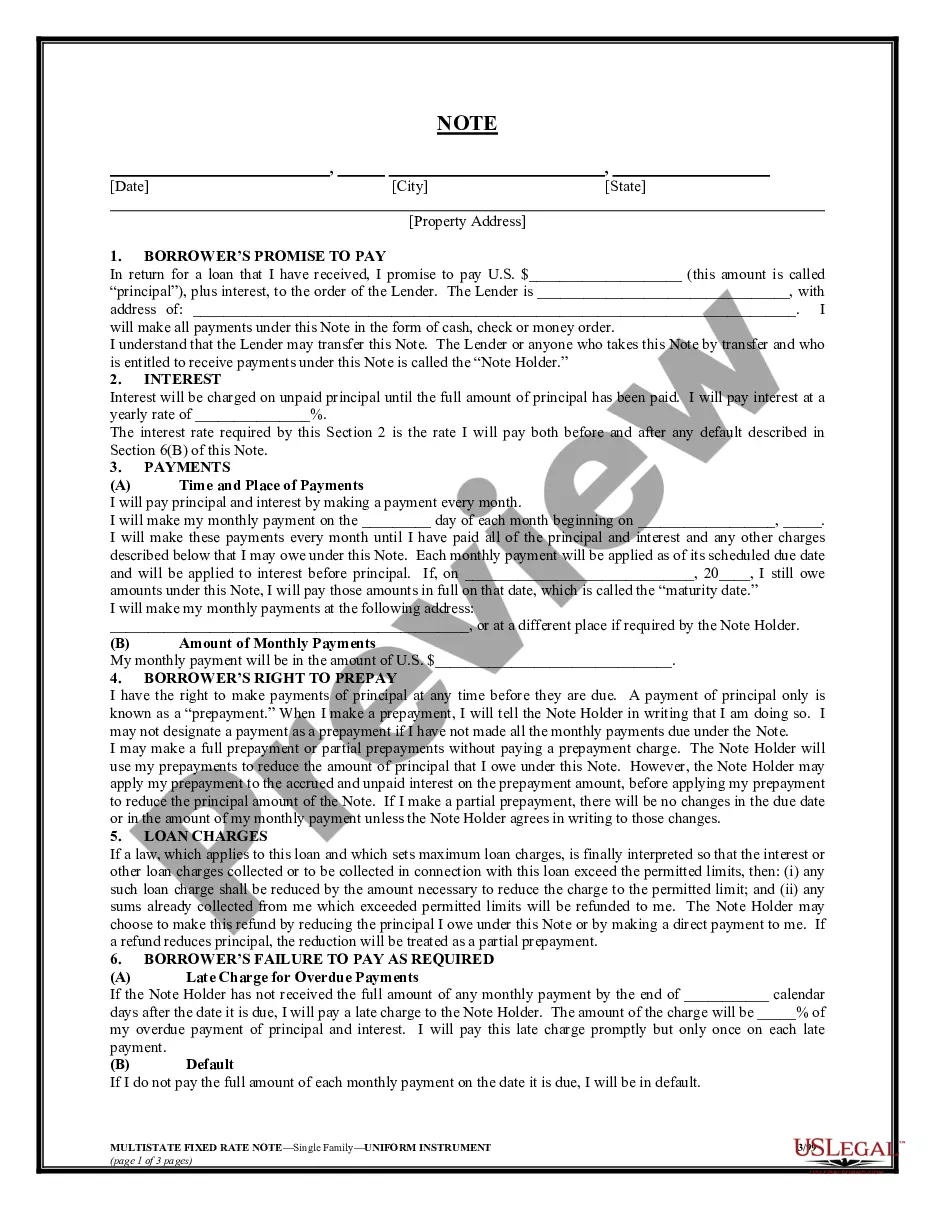

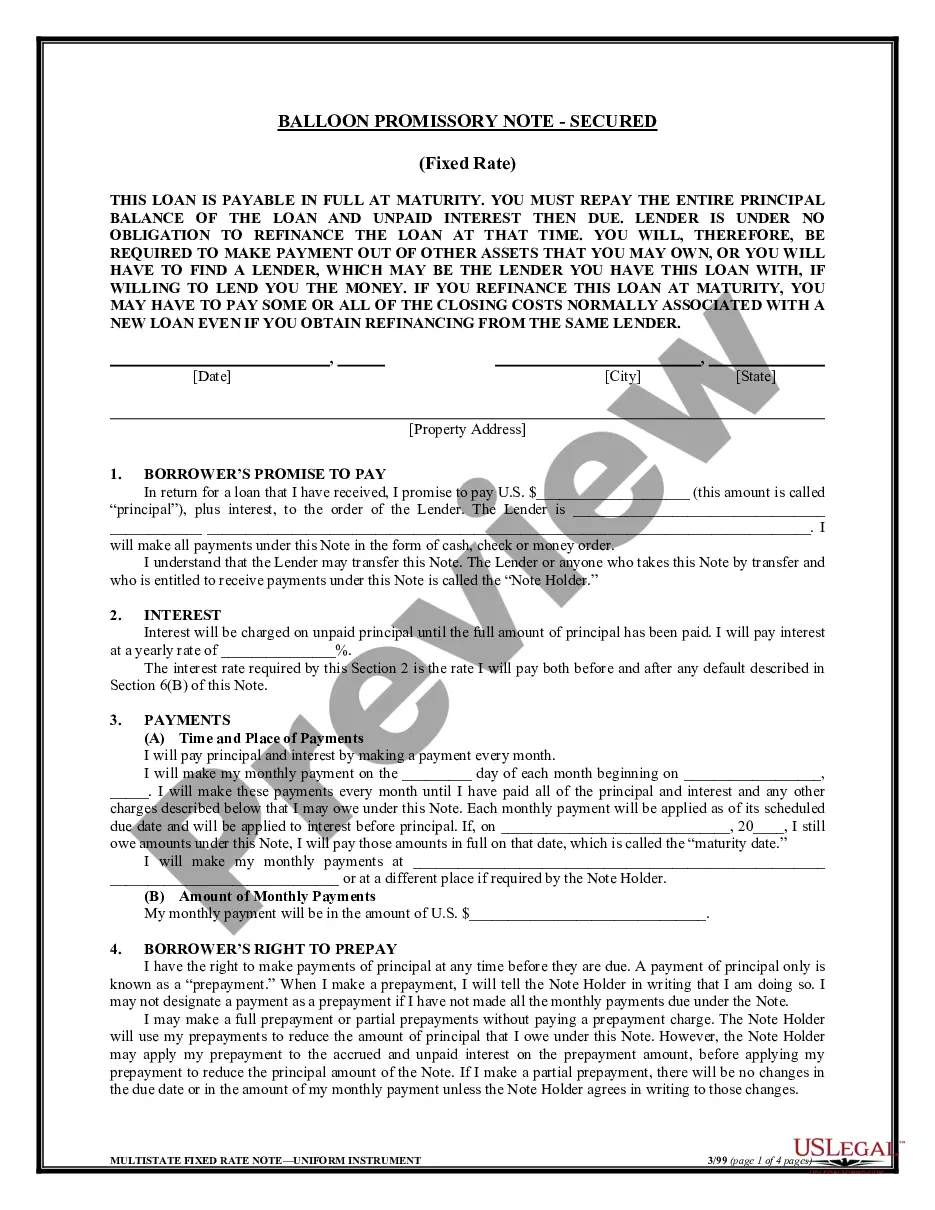

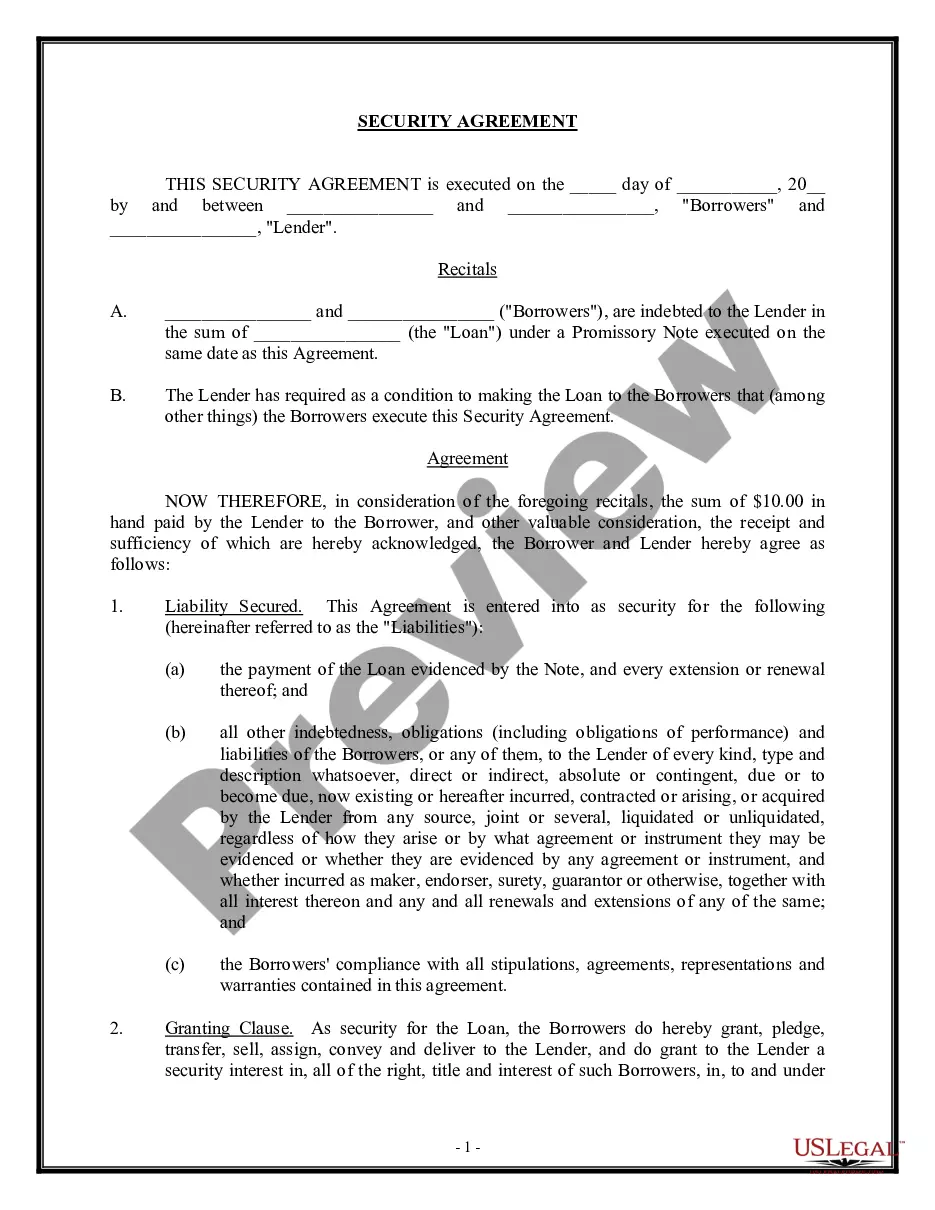

How to fill out Secured Promissory Note?

Dealing with legal paperwork and procedures can be a time-intensive addition to your daily routine.

Secured Loan For Mortgage and similar documents typically require you to look for them and comprehend how to fill them out efficiently.

Therefore, whether you are managing financial, legal, or personal issues, possessing a thorough and accessible online directory of forms when necessary will significantly help.

US Legal Forms is the leading online platform for legal templates, featuring over 85,000 state-specific documents and various tools to help you complete your paperwork swiftly.

Is this your first experience with US Legal Forms? Register and create your account in a matter of minutes, and you’ll gain access to the document directory and Secured Loan For Mortgage. Then, follow the steps outlined below to finalize your document: Ensure you have located the correct document using the Review feature and examining the document description. Select Buy Now when prepared, and choose the monthly subscription plan that suits your requirements. Click Download, then complete, sign, and print the document. US Legal Forms has 25 years of experience assisting users manage their legal documents. Find the document you need today and streamline any process without excessive effort.

- Explore the directory of relevant documents available to you with just one click.

- US Legal Forms provides state- and county-specific documents ready for download at any time.

- Protect your document management processes by using a high-quality service that allows you to create any document in minutes without additional or concealed charges.

- Simply Log In to your account, locate Secured Loan For Mortgage, and obtain it instantly within the My documents section.

- You can also retrieve previously downloaded documents.

Form popularity

FAQ

Eligibility for a secured loan usually extends to individuals who can provide adequate collateral and demonstrate the ability to repay the loan. This often includes homeowners and those with valuable assets. Lenders will assess your financial history and current situation before granting approval. If you have a steady income and a qualifying asset, you are likely eligible for a secured loan for mortgage.

Requirements for a secured loan typically include proof of income, a good credit score, and valuable collateral. Lenders will also need to assess the asset's worth to determine the loan amount. Additionally, you may be asked to provide personal identification and financial statements. By preparing these documents ahead of time, you can streamline the process of obtaining a secured loan for mortgage.

Approval for a secured loan is generally easier than for an unsecured loan, but it still requires careful consideration by the lender. Factors such as your credit score, income stability, and the value of the collateral play significant roles in the decision-making process. While it may not be difficult, ensuring you have all necessary documents ready can facilitate a smoother approval journey. Many users find success when applying for a secured loan for mortgage through platforms like US Legal Forms.

Qualification for a secured loan often depends on the value of the asset you are using as collateral. Lenders typically look for borrowers with a stable income and a good credit history. Additionally, you should be prepared to provide documentation regarding your financial situation and the asset you intend to secure. If you meet these criteria, you likely qualify for a secured loan for mortgage.

Getting a secured loan can be a beneficial choice if you need funds for a mortgage. This type of loan typically offers lower interest rates compared to unsecured options because it is backed by collateral. However, it is crucial to assess your financial situation and ensure you can meet the repayment terms. With the right planning, a secured loan for mortgage can enhance your financial flexibility.

Is a mortgage secured or unsecured debt? Mortgages are "secured loans" because the house is used as collateral, meaning if you're unable to repay the loan, the home may go into foreclosure by the lender. In contrast, an unsecured loan isn't protected by collateral and is therefore higher risk to the lender.

Examples of what can be used as collateral for a personal loan include the following: Your Vehicle. Your Home. Your Savings. Your Investment Accounts. Your Future Paychecks. Art. Jewelry.

Keep the loan Be aware, some lenders may be less willing to remortgage your property if you have a loan attached to it. So make sure you find out where the lender stands on this matter - before you apply. This will prevent you from applying for a mortgage that is unsuitable.

As it's very unlikely that a lender would write off a secured loan, the only way to get rid of one is to pay it off. There are three main ways to do this: continue making your regular payments as normal. negotiate with the lender and agree a different payment plan.

Keep the loan Be aware, some lenders may be less willing to remortgage your property if you have a loan attached to it. So make sure you find out where the lender stands on this matter - before you apply. This will prevent you from applying for a mortgage that is unsuitable.