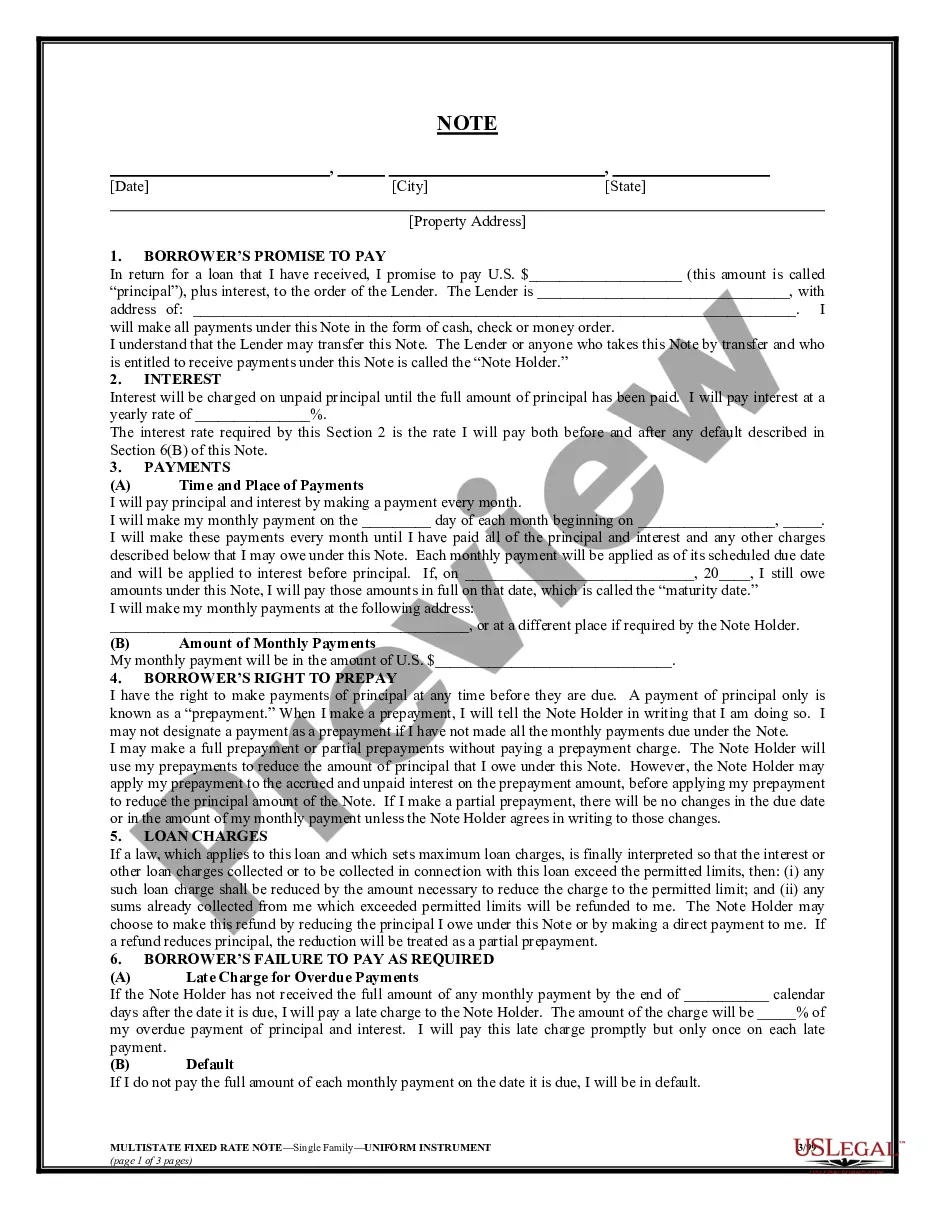

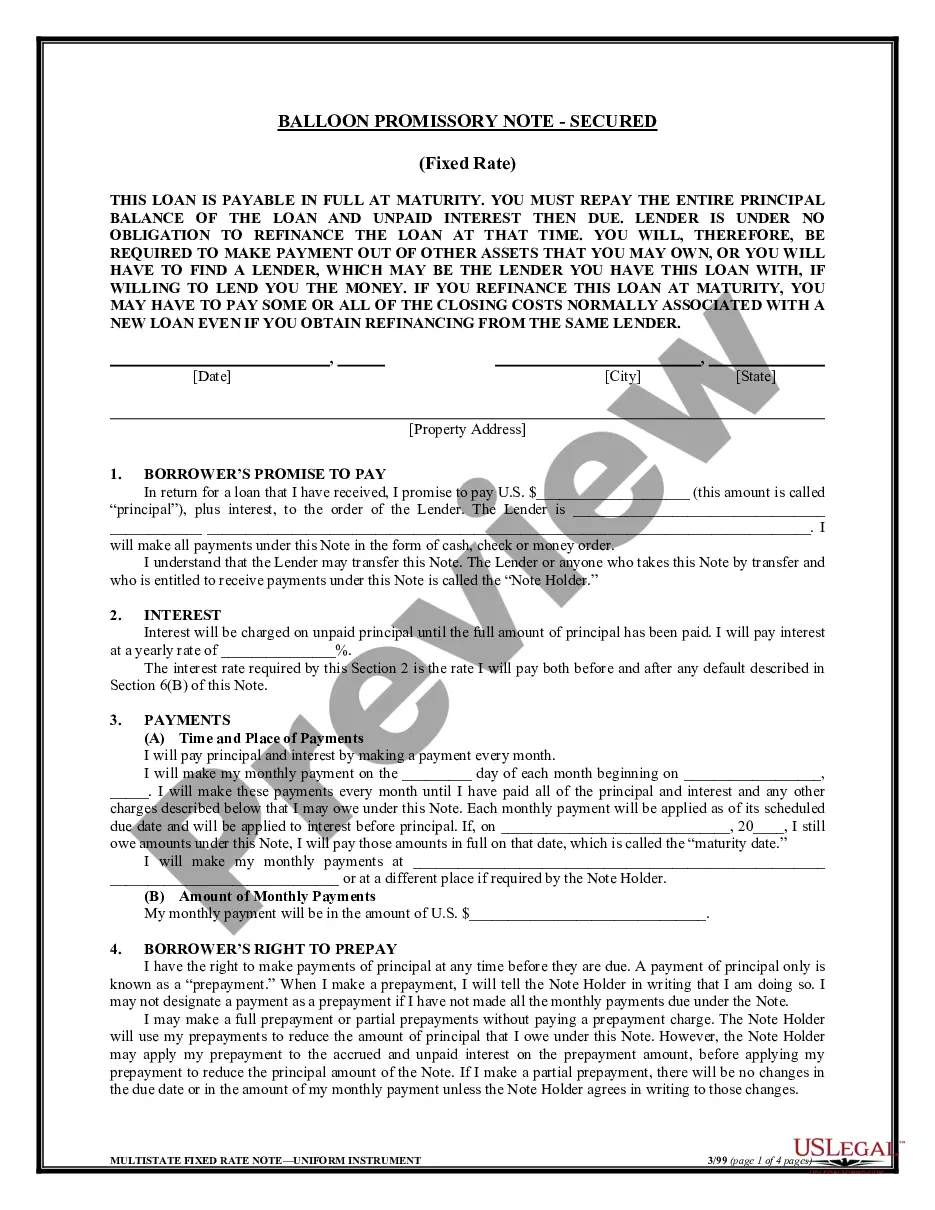

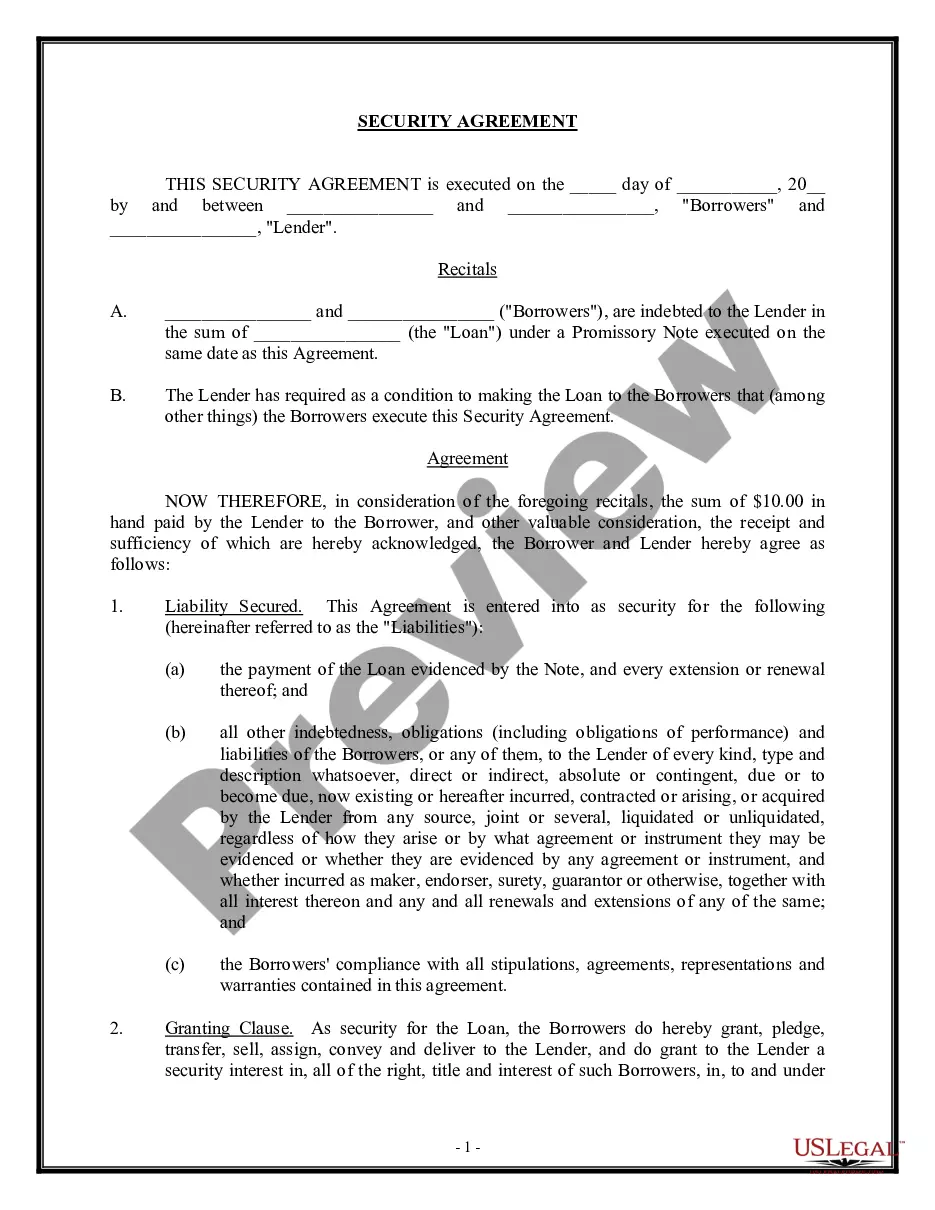

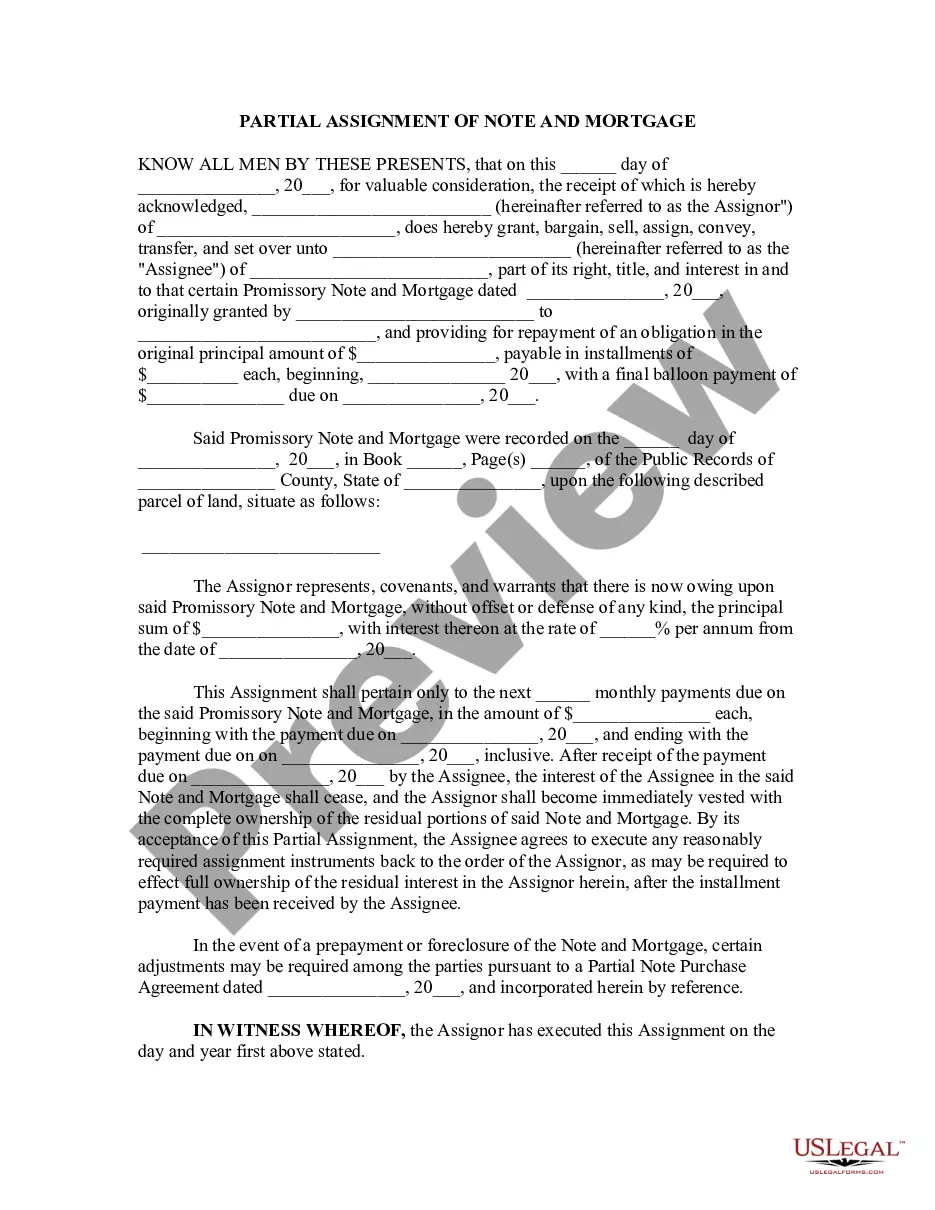

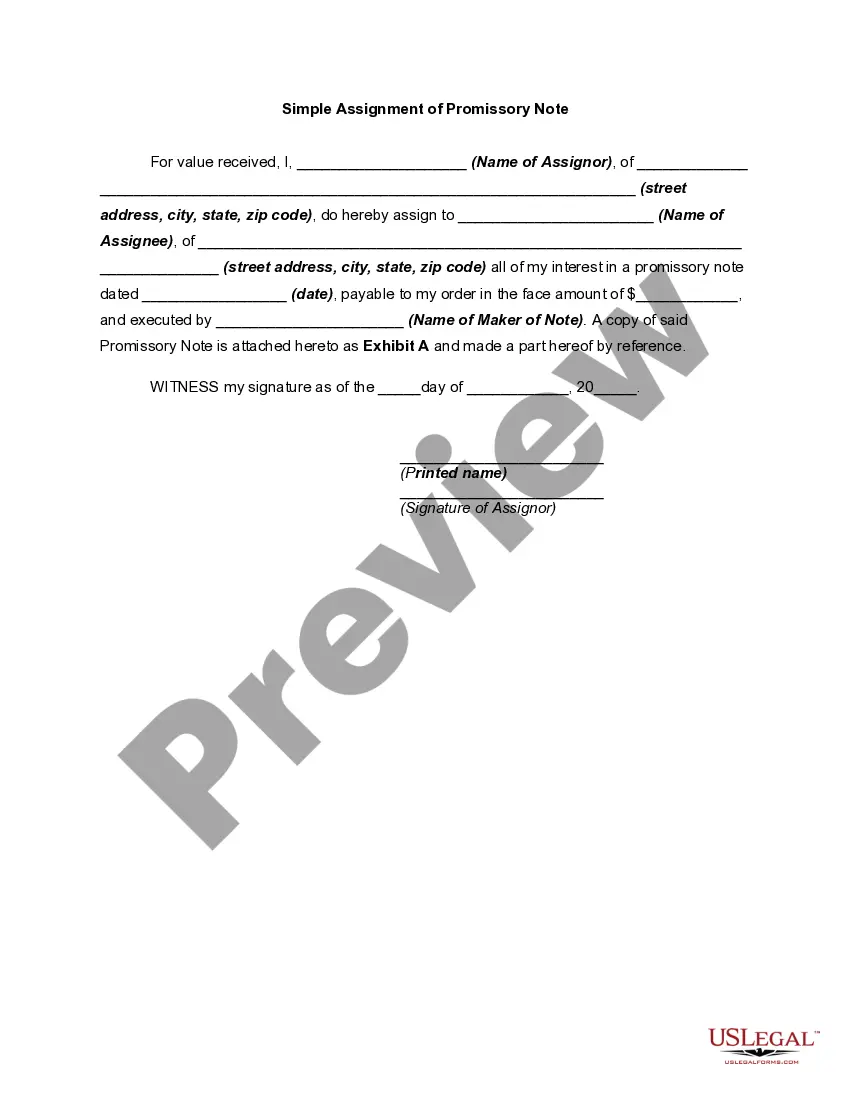

Secured Loan For Business

Description

How to fill out Secured Promissory Note?

Accessing legal document examples that adhere to federal and local regulations is crucial, and the internet provides numerous choices.

However, what’s the benefit of spending time searching for the appropriate Secured Loan For Business example online when the US Legal Forms digital library already has such templates gathered in one location.

US Legal Forms is the most extensive online legal repository with more than 85,000 editable templates created by attorneys for any business and personal situation.

Review the template using the Preview feature or through the text description to ensure it fulfills your needs.

- They are easy to search through with all documents categorized by state and intended use.

- Our experts stay updated with legislative changes, so you can always be assured your form is current and compliant when securing a Secured Loan For Business from our site.

- Acquiring a Secured Loan For Business is quick and straightforward for both existing and new users.

- If you already possess an account with an active subscription, Log In and save the document example you require in your preferred format.

- If you are new to our site, follow the steps below.

Form popularity

FAQ

To secure a loan for a business, start by assessing your financial needs and gathering necessary documentation, such as your business plan and financial statements. Next, research different lenders and their requirements for secured loans. Platforms like US Legal Forms can provide valuable resources and templates to streamline your application process and help you understand the terms involved in securing a loan.

The monthly payment on a $50,000 business loan depends on the interest rate and the loan term. For example, with an interest rate of 6% over five years, your monthly payment would be approximately $966. Calculating your potential payments can help you budget effectively when considering a secured loan for business.

Secured business loans work by requiring the borrower to pledge an asset as collateral. This means that if you fail to repay the loan, the lender can take the asset to recover their losses. This arrangement often leads to lower interest rates and higher loan amounts compared to unsecured loans, making a secured loan for business a smart option for many entrepreneurs.

To secure a business loan, you typically need to provide collateral, which can include assets like real estate, equipment, or inventory. Lenders also require a solid business plan, proof of revenue, and a good credit score. By presenting these documents, you demonstrate your ability to repay the secured loan for business, which can enhance your chances of approval.

Secured loans, also called collateralized loans, can be ideal for businesses who: Need low-cost capital. Need a larger or longer-term funding option.

As it's very unlikely that a lender would write off a secured loan, the only way to get rid of one is to pay it off. There are three main ways to do this: continue making your regular payments as normal. negotiate with the lender and agree a different payment plan.

A secured business loan requires a specific piece of collateral, such as a business vehicle or commercial property, which the lender can claim if you fail to repay your loan.

Most people have a loan secured by property, such as a mortgage or a car loan. These debts, called "secured debts," can be tricky in Chapter 7 bankruptcy. Although you can wipe out or "discharge" a secured loan in Chapter 7 bankruptcy, you'll lose the property you purchased if you don't pay for it after bankruptcy.

How to apply for a business loan in 7 steps Prepare documentation. ... Review your credit score. ... Gather financial documents. ... Create a business plan. ... Consider your collateral. ... Consider which loan to apply for. ... Assemble and submit your application.