Promissory Note Secured Format India

Description

How to fill out Multistate Promissory Note - Secured?

Finding a go-to place to take the most recent and relevant legal samples is half the struggle of dealing with bureaucracy. Discovering the right legal papers calls for precision and attention to detail, which is the reason it is crucial to take samples of Promissory Note Secured Format India only from reputable sources, like US Legal Forms. A wrong template will waste your time and delay the situation you are in. With US Legal Forms, you have very little to be concerned about. You can access and check all the information concerning the document’s use and relevance for the circumstances and in your state or county.

Consider the listed steps to finish your Promissory Note Secured Format India:

- Utilize the library navigation or search field to find your sample.

- View the form’s description to see if it suits the requirements of your state and area.

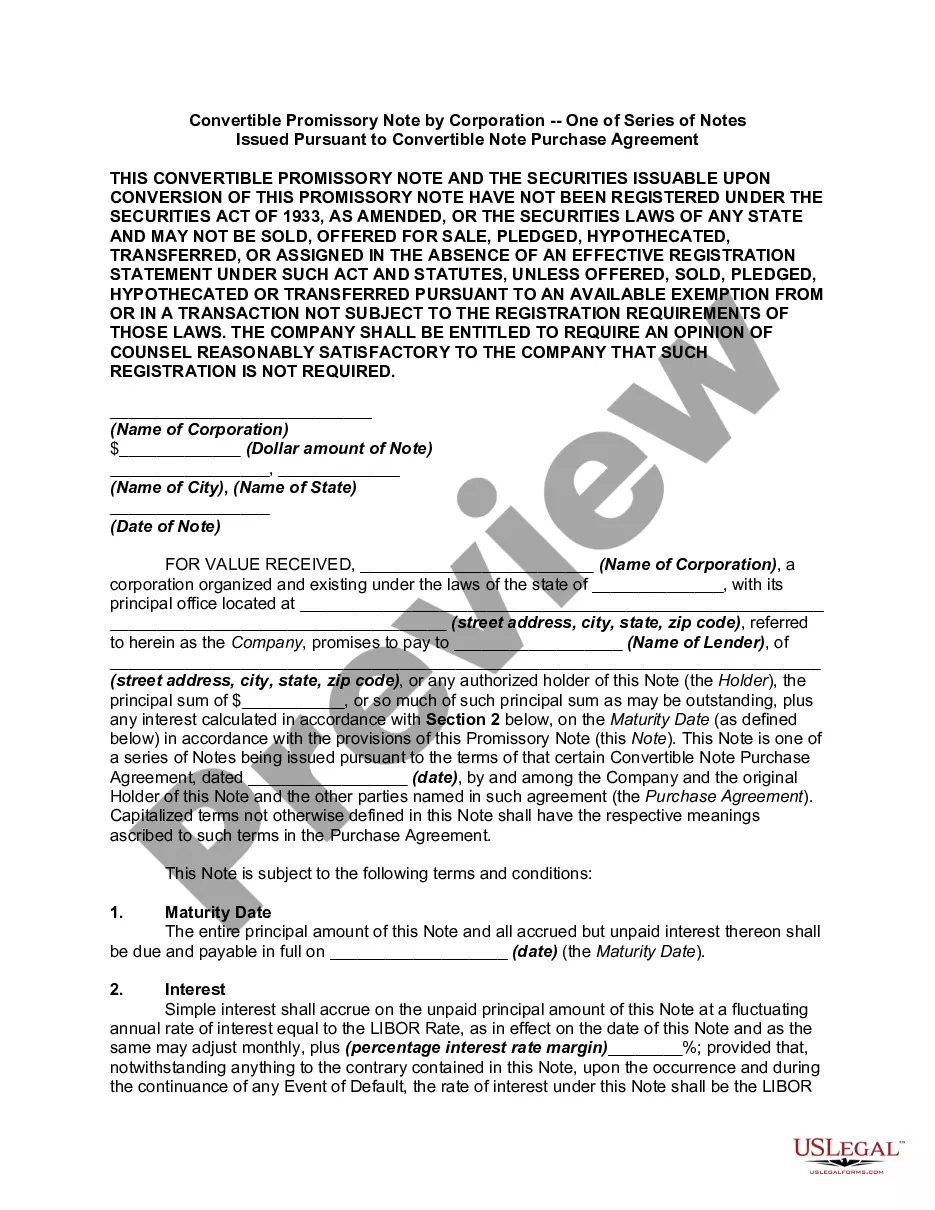

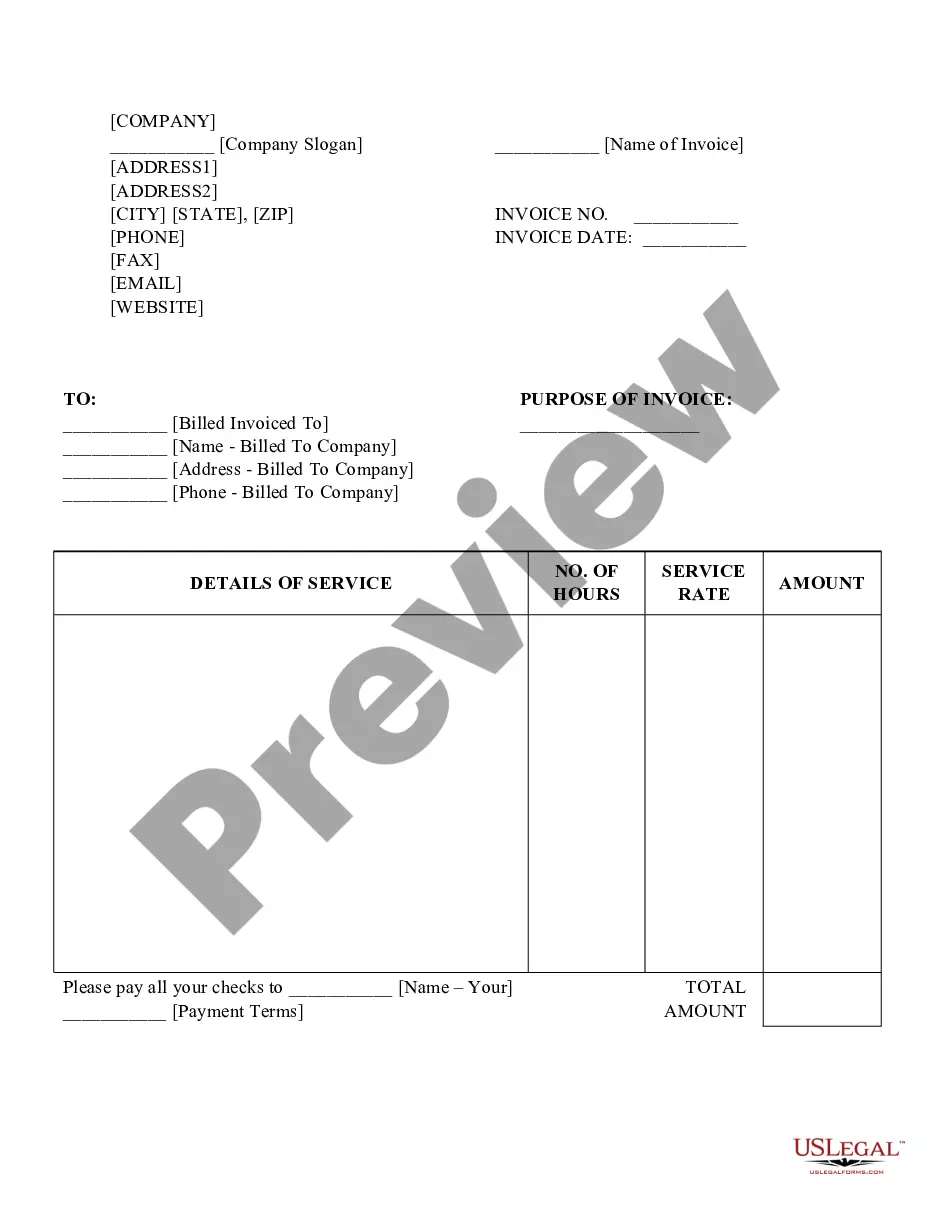

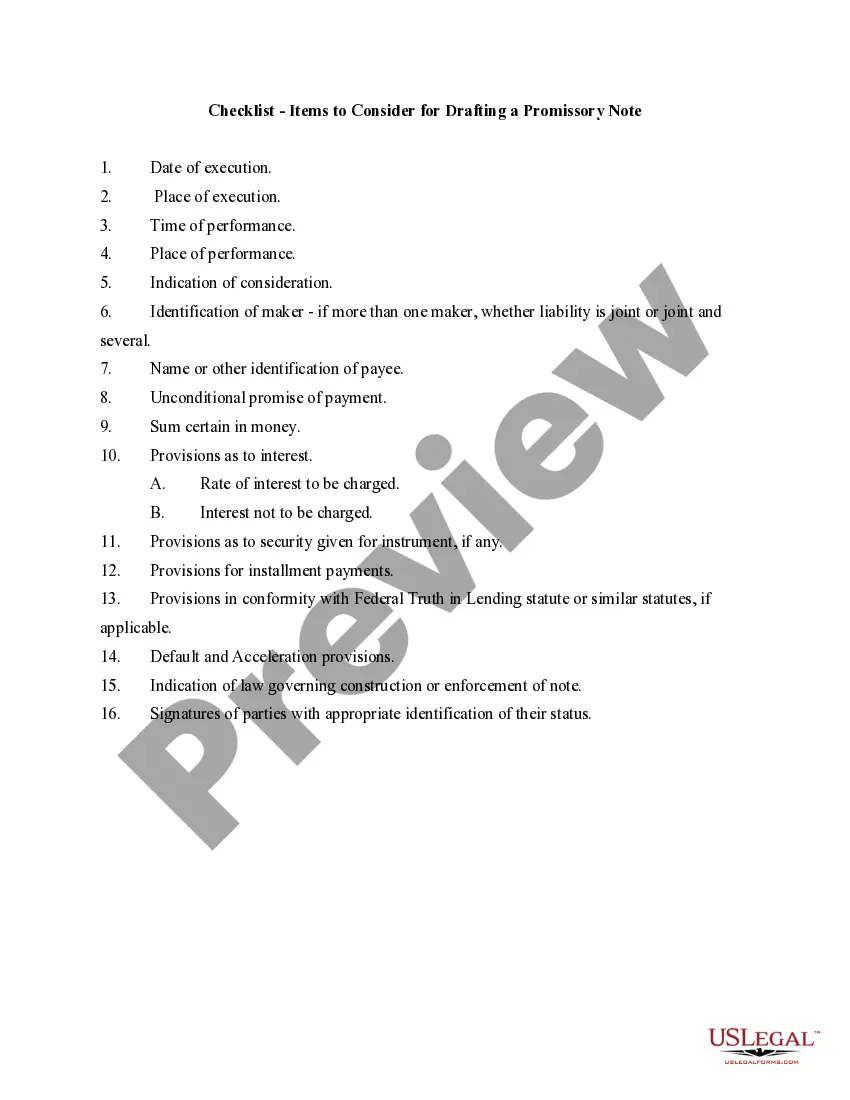

- View the form preview, if there is one, to make sure the form is definitely the one you are searching for.

- Go back to the search and look for the appropriate document if the Promissory Note Secured Format India does not suit your needs.

- If you are positive regarding the form’s relevance, download it.

- If you are a registered customer, click Log in to authenticate and access your selected forms in My Forms.

- If you do not have a profile yet, click Buy now to get the template.

- Choose the pricing plan that fits your needs.

- Proceed to the registration to finalize your purchase.

- Complete your purchase by picking a transaction method (bank card or PayPal).

- Choose the file format for downloading Promissory Note Secured Format India.

- Once you have the form on your device, you can modify it with the editor or print it and finish it manually.

Get rid of the hassle that accompanies your legal documentation. Check out the comprehensive US Legal Forms catalog to find legal samples, examine their relevance to your circumstances, and download them immediately.

Form popularity

FAQ

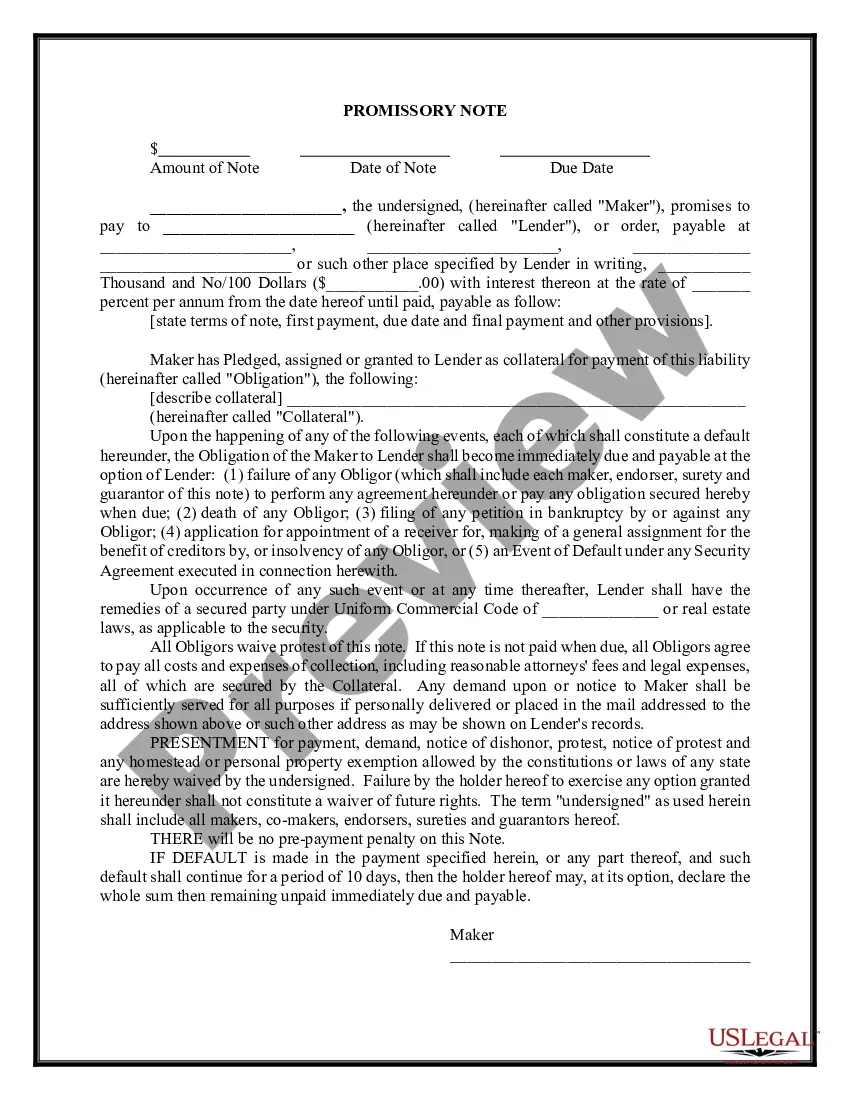

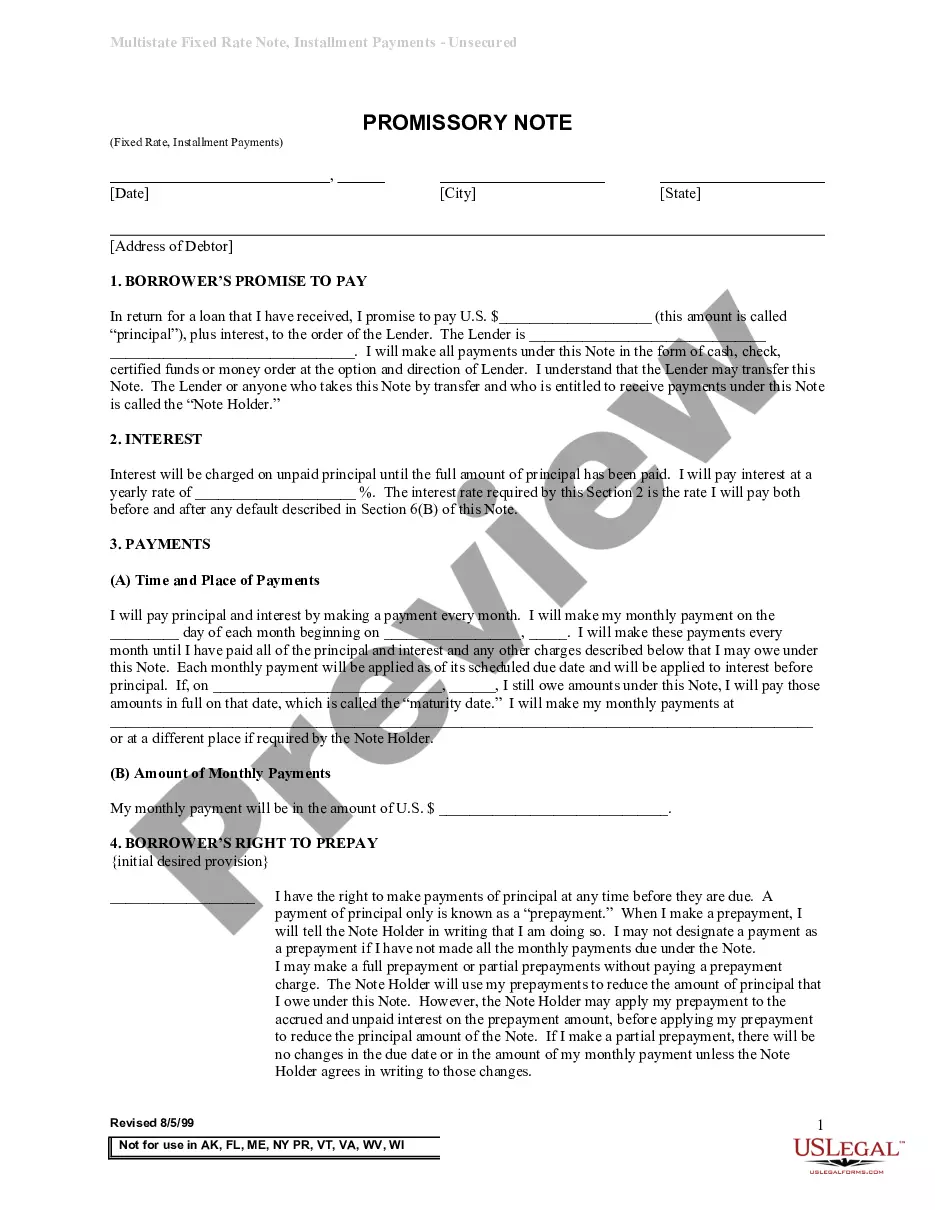

How to Write a Promissory Note Date. Name of the lender and borrower. Loan amount. Whether the loan is secured or unsecured. If it's secured with collateral: What is the collateral? ... Payment amount and frequency. Payment due date. Whether the loan has a cosigner, and if so, who.

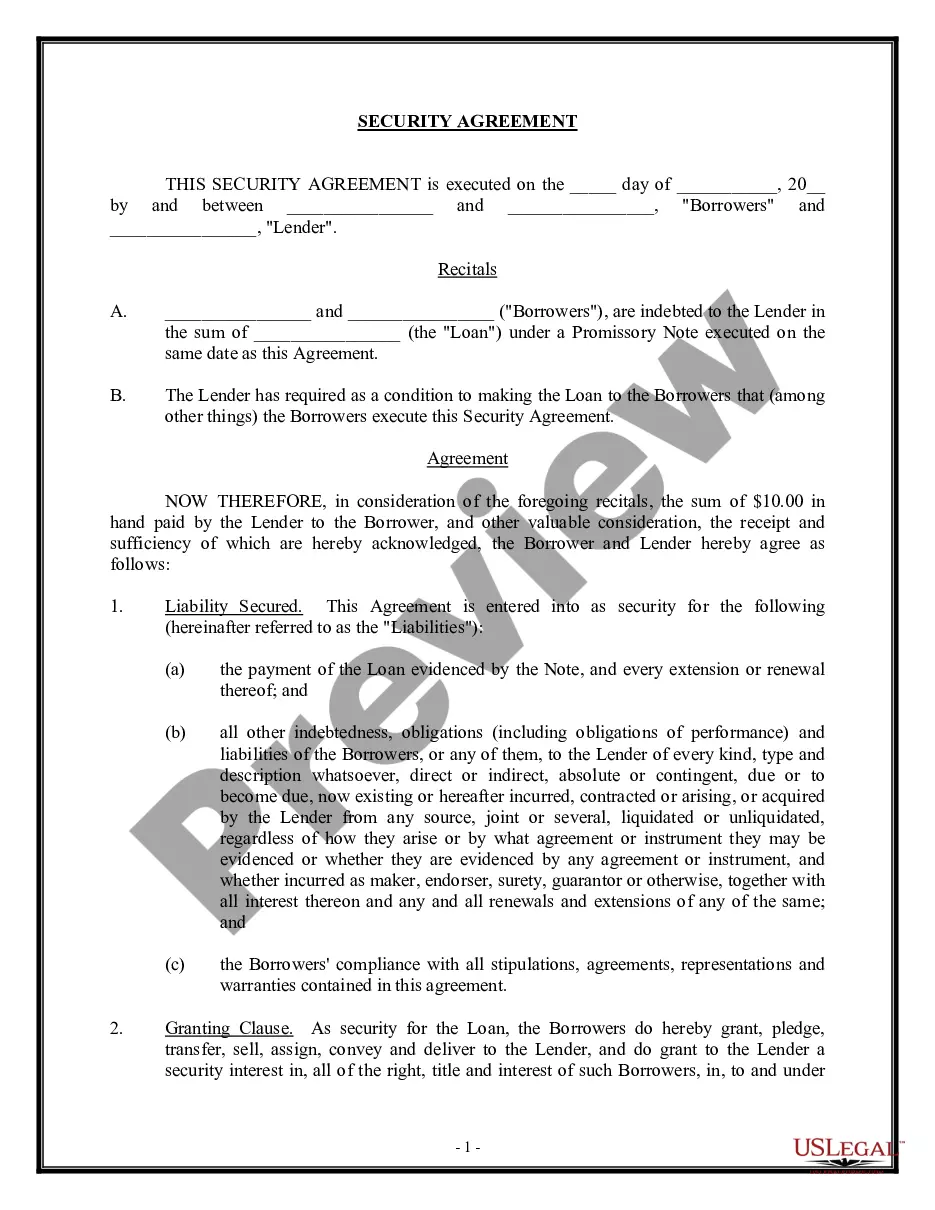

What should be included in a Secured Promissory Note? The amount of the loan and how that money may be transferred. All parties involved and their contact information. ... Repayment schedule. ... Any interest on the loan. ... The details of the collateral.

An unsecured promissory note does not require the borrower to provide any collateral in order to receive the loan. However, an unsecured promissory note is still a contract, and as such the lender has legal options to collect any overdue payments.

An unsecured promissory note is an obligation for payment without any property securing the payment. If the payor fails to pay, the payee must file a lawsuit and hope that the payor has sufficient assets that can be seized to satisfy the loan.

A contract for a collateral loan should clearly state what asset(s) are being used to secure the loan and include a clause on what could happen to the asset if the borrower defaults. It should also clearly outline the circumstances under which the collateral could be forfeited to the lender.