Letter Informing Debt Collector of Unfair Practices in Collection Activities - Communicating with a Consumer Regarding a Debt by Post Card

Understanding this form

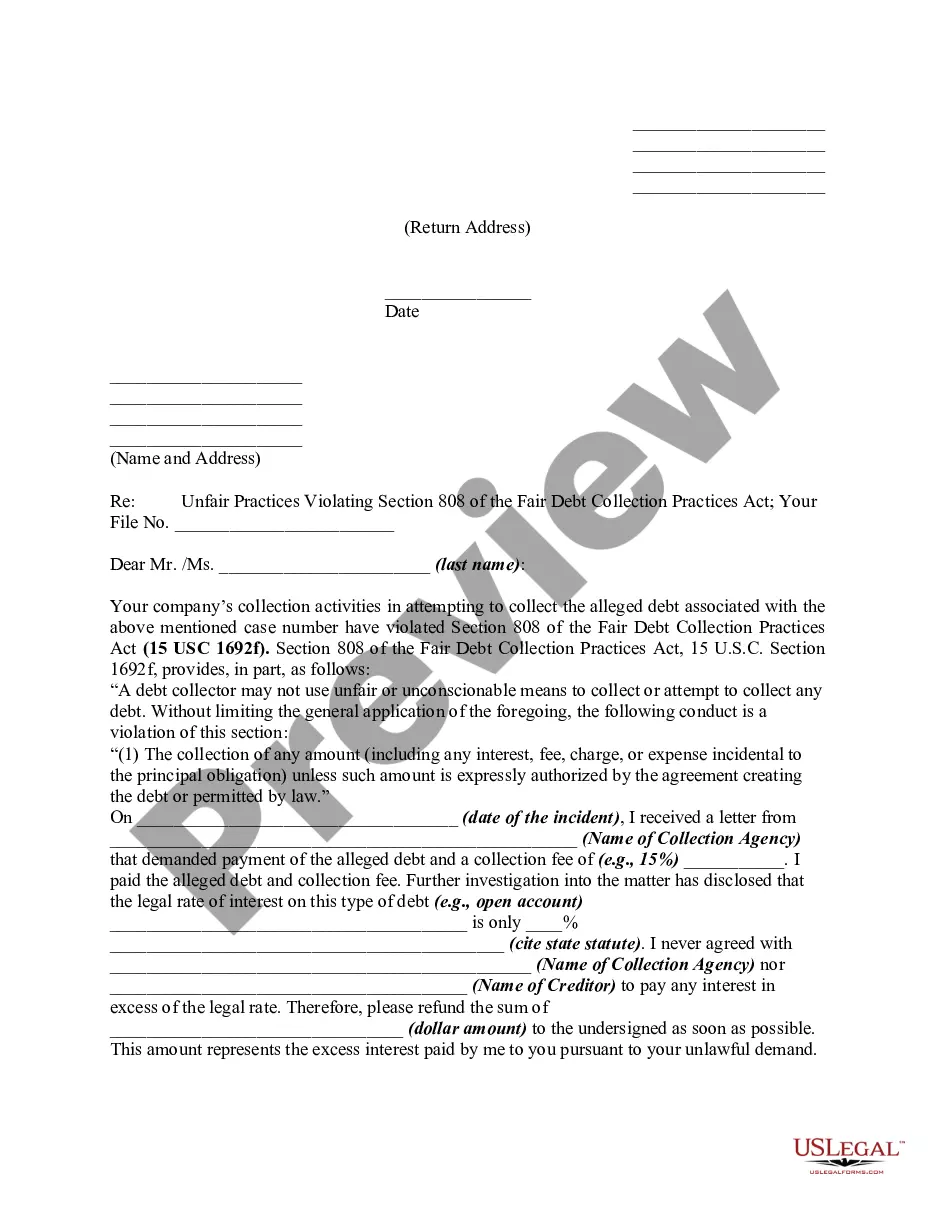

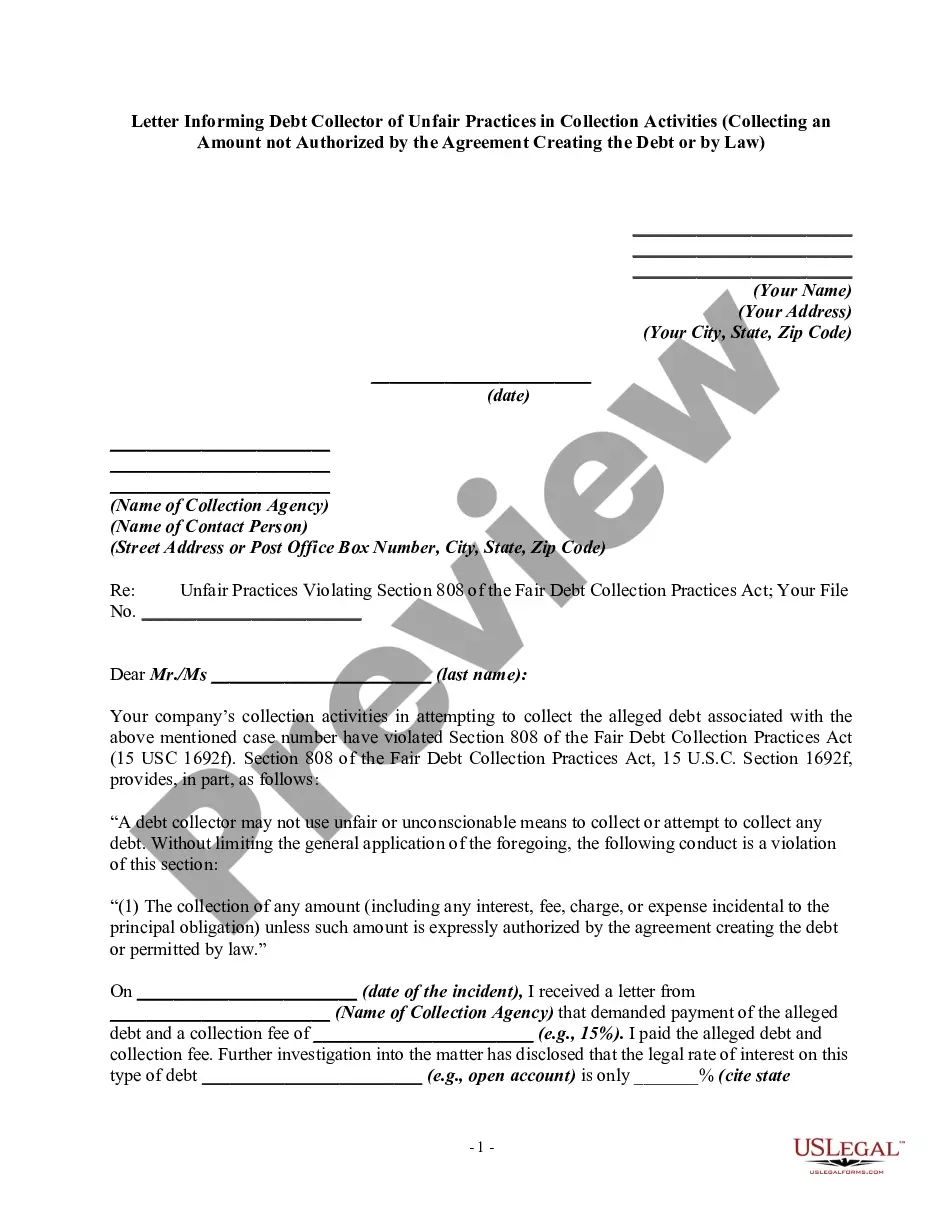

This form is a Letter Informing Debt Collector of Unfair Practices in Collection Activities, specifically addressing how a debt collector has communicated regarding a debt by post card. It is intended for consumers who want to formally notify a debt collector that their practices violate the Fair Debt Collection Practices Act (FDCPA). This letter serves as a warning to the collector and outlines the specific unfair practices that are prohibited under the law.

Key components of this form

- Your name and contact information

- Date of the letter

- Details of the collection agency and contact person

- Reference to the specific section of the FDCPA being violated

- A description of the incident involving the post card

- Your intentions to discuss remedies with an attorney

When to use this form

This form should be used when a consumer receives a post card from a debt collector that is deemed to violate the FDCPA. Use this letter if you believe the debt collector is using unfair communication methods that cause distress or violate your rights as a consumer. Sending this letter can help assert your legal rights and encourage the debt collector to cease such practices.

Intended users of this form

- Consumers who have received a post card from a debt collector.

- Individuals who believe debt collectors have violated their rights under the FDCPA.

- Anyone seeking to formally document their complaint against a debt collection agency.

Steps to complete this form

- Enter your name and contact information at the top of the letter.

- Fill in the date you are sending the letter.

- Provide the name and address of the collection agency and the contact person.

- Describe the unfair practices, referencing the specific violation of the FDCPA.

- State the date you received the post card and detail the contents that you find objectionable.

- Add your signature and printed name at the end of the letter, and include copies to the appropriate parties.

Notarization guidance

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include specific details about the incident.

- Not providing your contact information clearly.

- Using vague language instead of citing the specific violations.

Advantages of online completion

- Easy to download and customize according to your needs.

- Written by licensed attorneys to ensure legal accuracy and effectiveness.

- Available for immediate use, saving time compared to traditional legal consultations.

Legal use & context

- This letter serves as a formal notice regarding unfair debt collection practices.

- It can help document your complaints, which may be useful if pursuing further legal action.

- Sending this letter may compel the debt collector to amend their practices.

What to keep in mind

- The letter serves to notify debt collectors of violations of your rights under the FDCPA.

- It is essential to provide detailed information about the unfair practices encountered.

- Consulting with an attorney after sending this letter can help you explore further legal options.

Looking for another form?

Form popularity

FAQ

Step 1: Keep detailed records of what the debt collector is doing. Step 2: Take action write to the debt collector, complain to an External Dispute Resolution scheme (Ombudsman Service) or VCAT. Step 3: Complain to a Regulator.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

You have the right to tell a debt collector to stop communicating with you. To stop communication, send a letter to the debt collector and keep a copy of the letter. If you don't want a debt collector to contact you again, write a letter to the debt collector saying so.

Within 30 days of receiving the written notice of debt, send a written dispute to the debt collection agency. You can use this sample dispute letter (PDF) as a model. Once you dispute the debt, the debt collector must stop all debt collection activities until it sends you verification of the debt.

Your creditor also has to report your complaint to the Financial Conduct Authority (FCA), even if they respond within 3 business days. If you need help with this, you can phone our debt helpline on 0300 330 1313. We can usually help between 9am and 8pm, Monday to Friday.

The debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request that the debt not be reported to credit reporting agencies until the matter is resolved or have it removed from the report, if it already has been

Reach out to the company the collector says is the original creditor. They might help you figure out if the debt is legitimate and if this collector has the right to collect the debt. Also, get your free, annual credit report online or at 877-322-8228 and see if the debt shows up there. Dispute the debt in writing.

The name 623 dispute method refers to section 623 of the Fair Credit Reporting Act (FCRA). The method allows you to dispute a debt directly with the creditor in question as long as you have already filed your complaint with the credit bureau and completed their process.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.