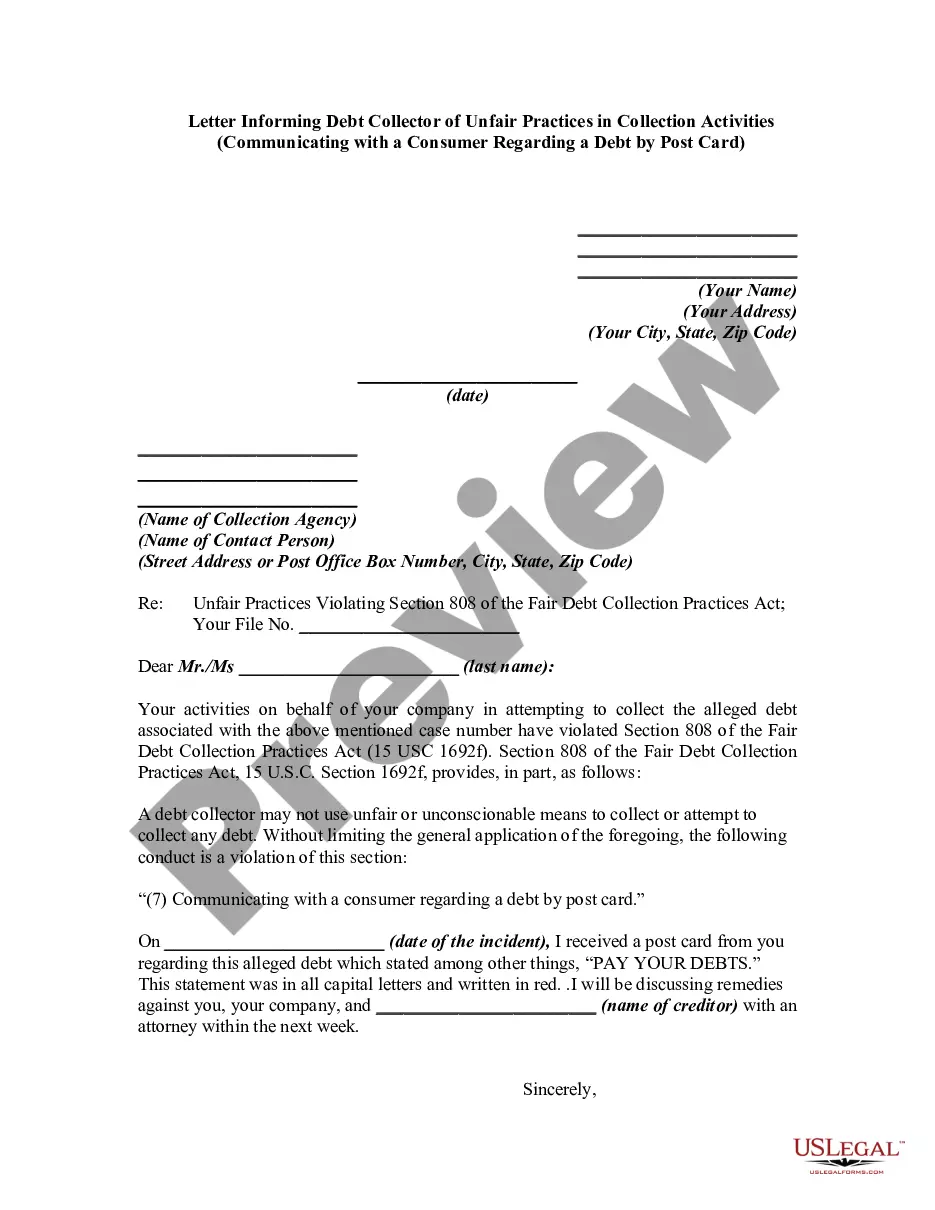

Letter Informing Debt Collector of Unfair Practices in Collection Activities - Soliciting a Postdated Check for the Purpose of Depositing or Threatening to Deposit the Check Prior to the Date on the Check

What this document covers

This form is a letter for informing a debt collector about their unfair practices in collecting a debt, specifically regarding the solicitation of postdated checks. It addresses violations under the Fair Debt Collection Practices Act, particularly the unlawful act of threatening to deposit a postdated check before its date. This letter serves as a formal notice to the collector, emphasizing your rights and the legal boundaries they must adhere to.

What’s included in this form

- Your contact information, including name and address

- Details about the collection agency and the individual collector

- A reference to the specific case number associated with the alleged debt

- A description of the unfair collection practices encountered

- A statement regarding potential legal actions being considered

When this form is needed

This form should be used when you have experienced unfair practices from a debt collector, particularly if they have solicited a postdated check or threatened to deposit a check before its designated date. If a debt collector pressures you for payment in ways that violate your rights, this letter is an essential step in asserting those rights and potentially halting illegal collection tactics.

Intended users of this form

- Individuals who believe they have been subjected to unfair debt collection practices

- Consumers facing allegations of unpaid debts from collection agencies

- Anyone who has been asked to provide a postdated check for a debt payment

- People seeking to document their communications with debt collectors

How to complete this form

- Enter your name and address at the top of the letter.

- Fill in the date when you are writing the letter.

- Provide the name and address of the collection agency and the contact person.

- State the details of the unfair practices you experienced, referencing the violation.

- Indicate your intention to seek legal counsel regarding the situation.

Notarization requirements for this form

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to include the collection agency's correct name and address.

- Not referencing the specific violation under the Fair Debt Collection Practices Act.

- Leaving out your case number, which may confuse the collector.

- Not keeping a copy of the letter for your records.

Advantages of online completion

- Convenience of having a legally-sound template ready for immediate use.

- Editability allows you to tailor the letter to your specific situation effectively.

- Reliable guidance in ensuring compliance with legal standards.

Legal use & context

- This letter serves as official documentation of your concerns and can be used if you pursue legal action.

- It helps establish a record of the debt collector's violations, which can support your case.

- Consulting with an attorney after sending this letter may provide further legal options.

Looking for another form?

Form popularity

FAQ

The FDCPA gives you a set period of time to dispute debts with collection agencies, but you can still request a debt validation after 30 days.

Under the Fair Debt collection Practices Act (FDCPA), I have the right to request validation of the debt you say I owe you. I am requesting proof that I am indeed the party you are asking to pay this debt, and there is some contractual obligation that is binding on me to pay this debt.

Debt collectors are legally required to send you a debt validation letter, which outlines what the debt is, how much you owe and other information. If you're still uncertain about the debt you're being asked to pay, you can send the debt collector a debt verification letter requesting more information.

You're protected from harassing or abusive practices The Fair Debt Collection Practices Act prohibits debt collectors from using any harassing or abusive practices in an attempt to collect the debt.Along with other restrictions, debt collectors cannot: Use profane language. Threaten or use violence.

Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

A debt validation letter can be an effective tool for dealing with debt collectors.

Once a debt collector receives written notice from a consumer that he or she refuses to pay the debt or wants the collector to stop further collection efforts, the debt collector must cease any further communication with the consumer except "(1) to advise the consumer that the debt collector's further efforts are being

The Fair Debt Collection Practices Act (FDCPA) is the main federal law that governs debt collection practices. The FDCPA prohibits debt collection companies from using abusive, unfair or deceptive practices to collect debts from you.

Collection agencies can and do refuse payments. There's no law saying they have to accept a check or money order. Some people might tell you that as long as you send something in every month, creditors can't take collection action against you.