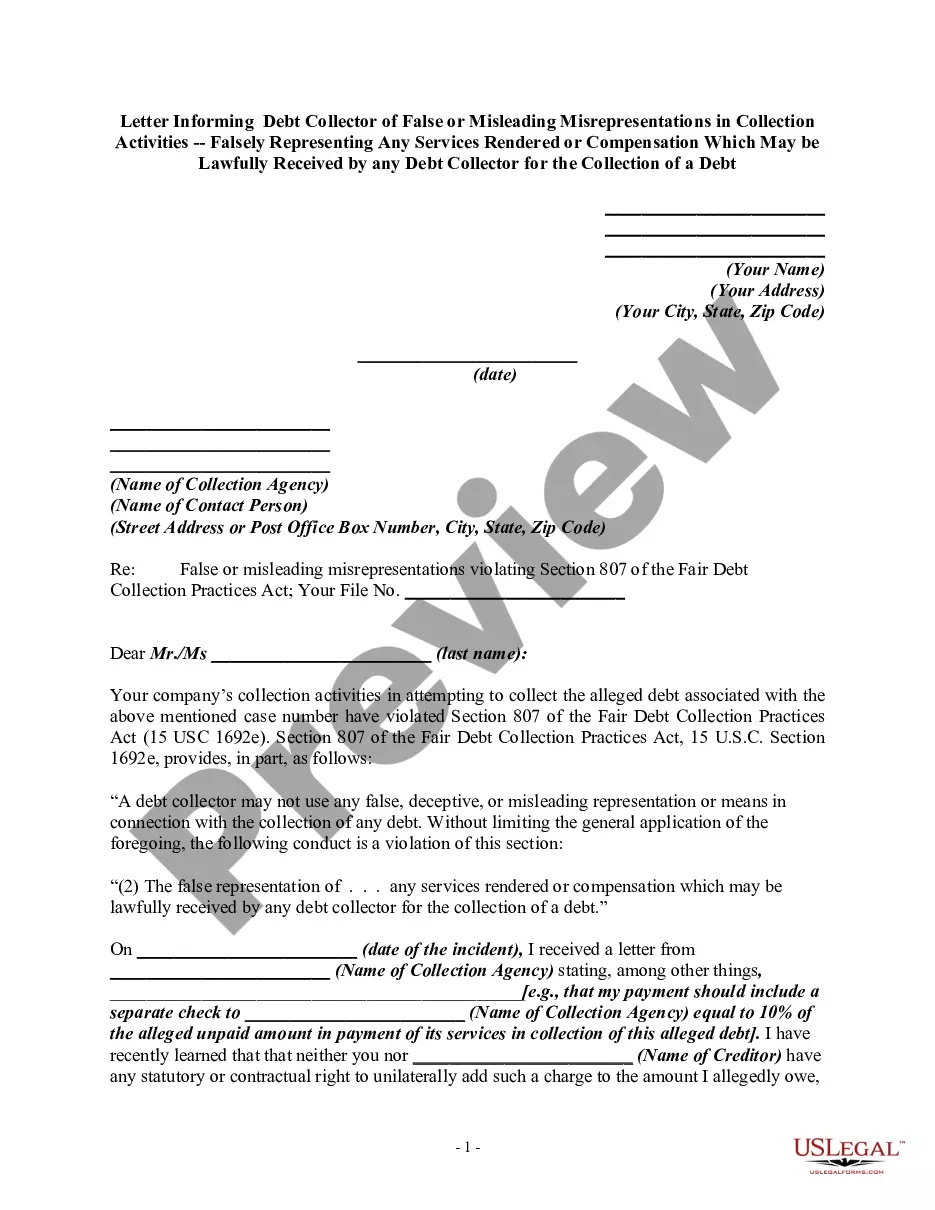

Letter Informing Debt Collector of False or Misleading Misrepresentations in Collection Activities - Falsely Representing or Implying that a Debt Collector Operates or is Employed by a Consumer Reporting Agency

What this document covers

This form is a Letter Informing Debt Collector of False or Misleading Misrepresentations in Collection Activities. It is used to notify a debt collector when they have falsely claimed to be affiliated with a consumer reporting agency. Under the Fair Debt Collection Practices Act, such misrepresentations are illegal and can be challenged using this form.

Main sections of this form

- Your personal information, including name and address.

- The date of the letter.

- The collection agencyâs name and contact person.

- Reference to the specific section of the Fair Debt Collection Practices Act.

- Description of the misleading communication received.

- Your signature and printed name.

Situations where this form applies

This form should be used when you believe that a debt collector has misrepresented their affiliation with a consumer reporting agency in their communications with you. It is particularly relevant if you have received a letter or call that suggests a false relationship with a credit bureau or implies threats to your credit score unjustly.

Intended users of this form

- Individuals who have been contacted by debt collectors.

- Consumers who believe they are victims of deceptive collection practices.

- Anyone who wants to formally document a misleading representation related to a debt.

Instructions for completing this form

- Fill in your personal details at the top of the letter.

- Insert the date you are sending the letter.

- Provide the name and address of the collection agency.

- Clearly state the section of the Fair Debt Collection Practices Act that has been violated.

- Describe the misleading communication you received.

- Sign and print your name at the bottom of the letter.

Does this form need to be notarized?

This form does not typically require notarization unless specified by local law. However, it is advisable to check state-specific requirements to ensure compliance.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Not including all relevant personal information.

- Failing to specify the date of the misleading communication.

- Ignoring to cite the correct section of the Fair Debt Collection Practices Act.

Benefits of completing this form online

- Convenient access to a professionally drafted template.

- Easy to customize and download according to your needs.

- Ensures compliance with legal requirements, reducing the chance of errors.

Looking for another form?

Form popularity

FAQ

Know Your Rights! RIGHT TO DISPUTE THE DEBT: Within 30 DAYS of receiving notice of the debt from the debt collector, you can send a letter to the debt collector disputing the debt and requesting the name and contact information of the original creditor.

Dispute the error with the credit bureau. Report the collections account and ask to have it removed from your credit report. 2feff Provide copies of any evidence you have proving the debt doesn't belong to you. Even if the debt belongs to you, that doesn't mean the collector is legally able to collect from you.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.

No. Debt collectors are prohibited from deceiving or misleading you while trying to collect a debt. Debt collectors are generally prohibited under federal law from using any false, deceptive, or misleading misrepresentation in collecting a debt.

In the letter, reference the date of the initial contact and the method, for example, "a phone call received from your agency on April 25, 2019." You also need to provide a statement that you're requesting validation of the debt. Do not admit to owing the debt or make any reference to payment.

The name 623 dispute method refers to section 623 of the Fair Credit Reporting Act (FCRA). The method allows you to dispute a debt directly with the creditor in question as long as you have already filed your complaint with the credit bureau and completed their process.

The debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request that the debt not be reported to credit reporting agencies until the matter is resolved or have it removed from the report, if it already has been

Your full name and address. The collections agency's name and address. A request for the amount of the debt claimed to be owed. A request for the name of the original creditor. A request for the judgment information (if applicable) A request for proof of the company's license.

If you believe any account information is incorrect, you should dispute the information to have it either removed or corrected. If, for example, you have a collection or multiple collections appearing on your credit reports and those debts do not belong to you, you can dispute them and have them removed.