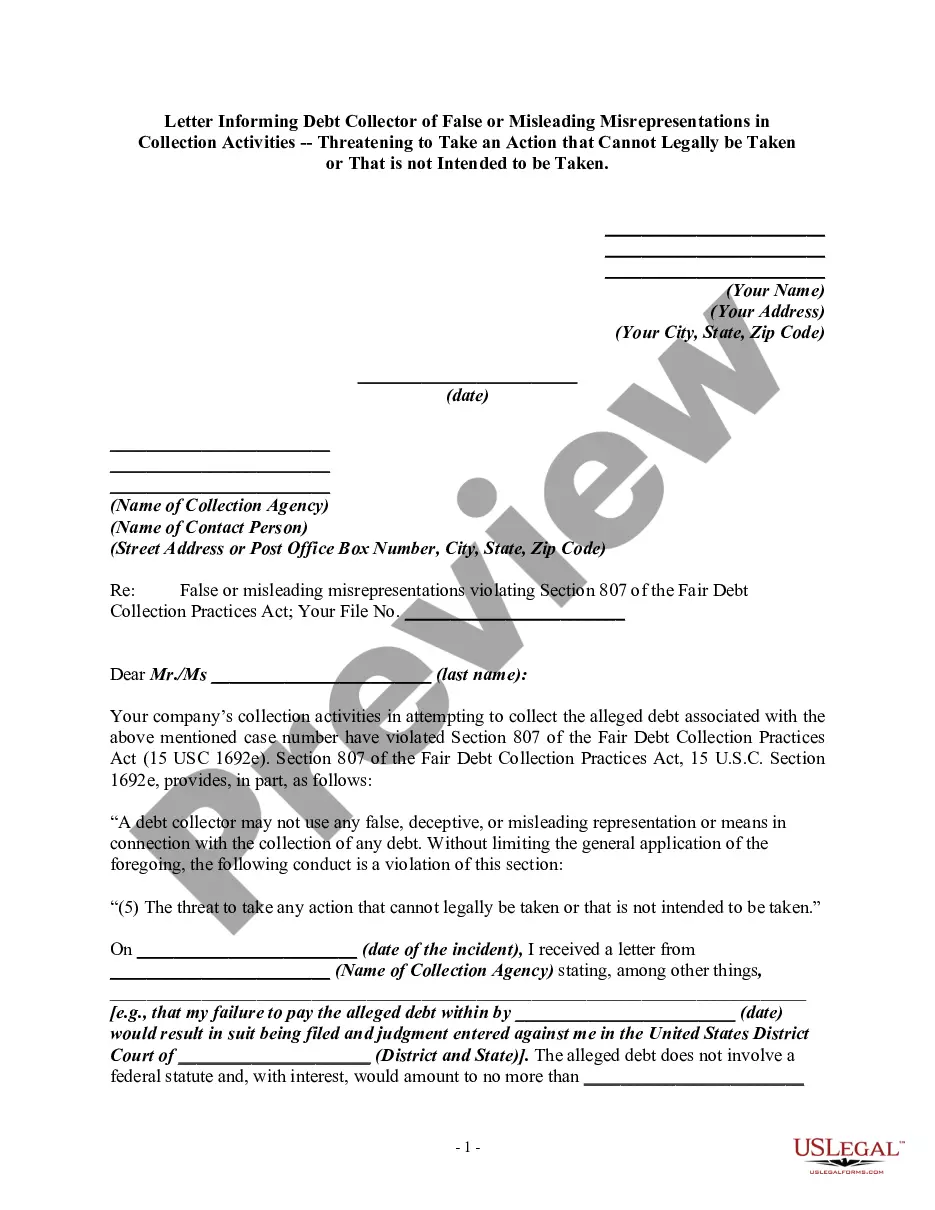

Letter Informing Debt Collector of False or Misleading Misrepresentations in Collection Activities - Threatening to Take an Action that Cannot Legally be Taken or That is not Intended to be Taken - Contacting the Consumer’s Employer

About this form

This form serves as a formal letter informing a debt collector of false or misleading representations during collection activities. Specifically, it addresses threats to take actions that cannot legally be taken, as stipulated by the Fair Debt Collection Practices Act. By using this letter, consumers can assert their rights and seek to halt improper collection practices that violate their legal protections.

Form components explained

- Your personal information, including your name and address.

- Date of the letter.

- Details about the collection agency and a contact person.

- Reference to the specific violations of the Fair Debt Collection Practices Act.

- A description of the misleading communication received from the collector.

- Your request to cease unlawful collection practices.

When to use this document

This form should be used when you receive communication from a debt collector that includes threats of actions not legally permitted, such as contacting your employer for purposes outside of obtaining location information. It is particularly useful when a collector attempts to pressure you by misrepresenting the legal consequences of not paying a debt.

Intended users of this form

- Consumers who have received misleading communications from debt collectors.

- Individuals feeling threatened by debt collection tactics that violate their rights.

- Anyone wishing to formally respond to collection activities that are potentially unlawful.

How to complete this form

- Enter your personal information at the top of the letter.

- Fill in the date of writing the letter.

- Provide the name and contact details of the collection agency.

- Clearly outline the misleading statements made by the debt collector.

- Request cessation of improper collection practices in your closing statement.

- Sign the letter with your printed name and signature.

Is notarization required?

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include all required personal information.

- Not specifying the date of the misleading communication.

- Using vague language that does not clearly state the violation.

- Neglecting to keep a copy of the letter for your records.

Benefits of using this form online

- Conveniently create and download your letter without needing legal assistance.

- Editable templates allow you to customize the content to fit your specific situation.

- Access to professionally drafted forms ensures compliance with legal standards.

Legal use & context

- This form is legally valid under the Fair Debt Collection Practices Act.

- Using this letter can help document communication with debt collectors.

- It serves as an essential step in resolving disputes about unlawful collection tactics.

Looking for another form?

Form popularity

FAQ

You have the right to sue the collection agency if they act improperly for one year from the improper action. You can sue for lost wages and other expenses incurred, including legal and court costs. Also, the judge is allowed to award you up to $1,000 in punitive damages.

Debt validation is your federal right granted under the Fair Debt Collection Practices Act (FDCPA). To request debt validation, you must send a written request to the debt collector within 30 days of being contacted by the collection agency.

The debt dispute letter should include your personal identifying information; verification of the amount of debt owed; the name of the creditor for the debt; and a request that the debt not be reported to credit reporting agencies until the matter is resolved or have it removed from the report, if it already has been

No. Debt collectors are prohibited from deceiving or misleading you while trying to collect a debt. Debt collectors are generally prohibited under federal law from using any false, deceptive, or misleading misrepresentation in collecting a debt.

If you pay the collection agency directly, the debt is removed from your credit report in six years from the date of payment. If you don't pay, it purges six years from the last activity date, but you may be at risk for wage garnishment.

Within 30 days of receiving the written notice of debt, send a written dispute to the debt collection agency. You can use this sample dispute letter (PDF) as a model. Once you dispute the debt, the debt collector must stop all debt collection activities until it sends you verification of the debt.

The name 623 dispute method refers to section 623 of the Fair Credit Reporting Act (FCRA). The method allows you to dispute a debt directly with the creditor in question as long as you have already filed your complaint with the credit bureau and completed their process.

Step 1: Keep detailed records of what the debt collector is doing. Step 2: Take action write to the debt collector, complain to an External Dispute Resolution scheme (Ombudsman Service) or VCAT. Step 3: Complain to a Regulator.

Debt collectors cannot harass or abuse you. They cannot swear, threaten to illegally harm you or your property, threaten you with illegal actions, or falsely threaten you with actions they do not intend to take. They also cannot make repeated calls over a short period to annoy or harass you.