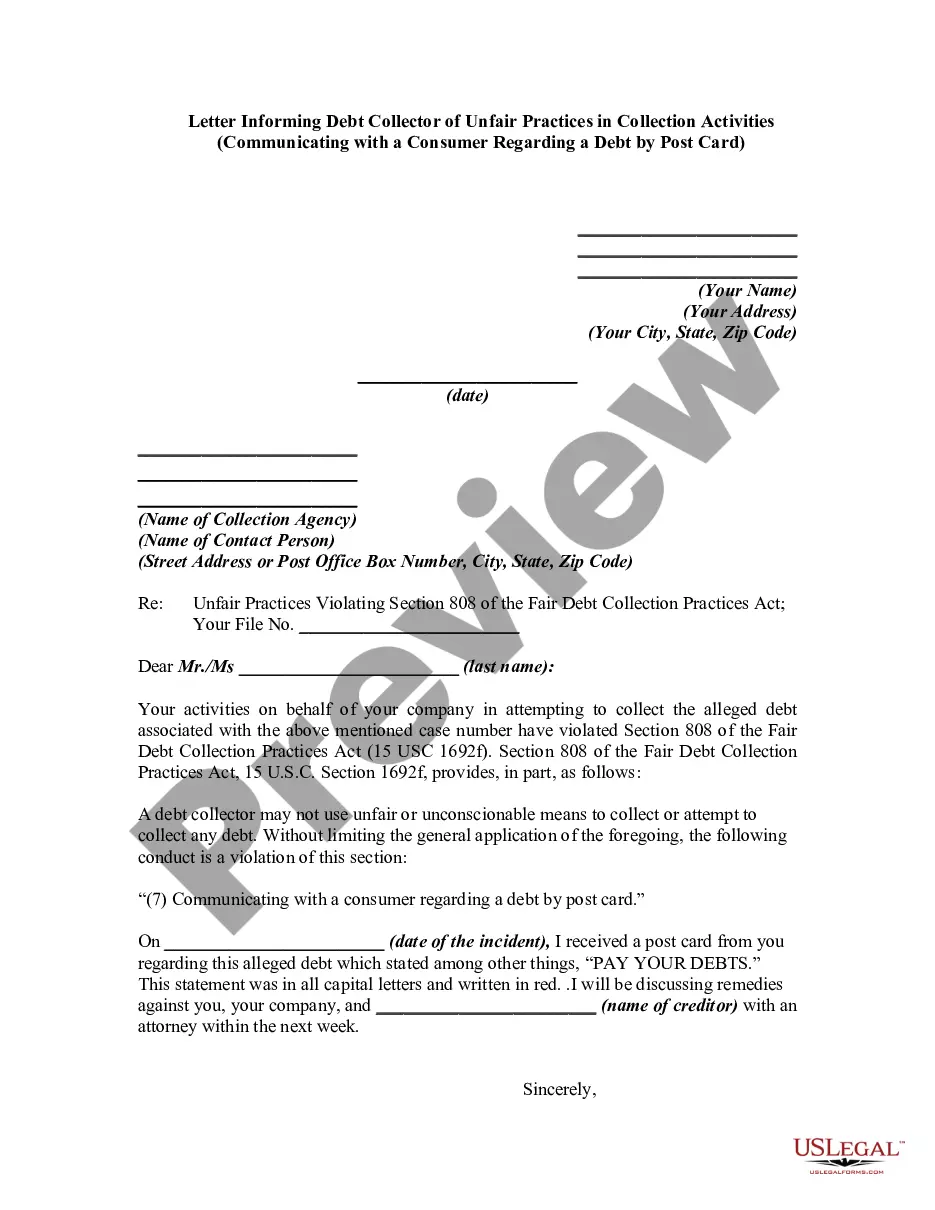

Notice of Violation of Fair Debt Act - Unlawful Contact by Postcard

Overview of this form

The Notice of Violation of Fair Debt Act - Unlawful Contact by Postcard is a legal document used by debtors to report violations of debt collection practices. Specifically, this form addresses unlawful communications made by debt collectors through postcards, which is prohibited under Section 808 of the Fair Debt Collection Practices Act (FDCPA). This form differs from other collection notices as it focuses solely on postcard communications and provides a structured way to document and report violations effectively.

What’s included in this form

- Debtor's information: Name and address of the debtor initiating the notice.

- Debt collector's information: Name and address of the company collecting the debt.

- Violation details: A section for describing the specific actions taken by the debt collector that constitute a violation.

- Case number: Reference to the associated debt or case for clarity.

- Notification letters: Instructions for sending copies of prior complaints to the FTC and state attorney general.

When this form is needed

This form should be used when a debtor has received communications from a debt collector via postcard, which violates the FDCPA. It is appropriate to file this notice after the first violation is identified, as well as in cases of subsequent violations. By using this form, the debtor can formally notify the debt collector of their unlawful actions and seek to stop these practices.

Who should use this form

- Debtors who have been contacted by debt collectors via postcard.

- Individuals seeking to report unfair debt collection practices.

- Consumers wishing to protect their rights under the Fair Debt Collection Practices Act.

How to prepare this document

- Identify your name and address at the top of the form.

- Fill in the name and address of the debt collector and any relevant case number.

- Describe the violation in your own words, providing factual details.

- Include the dates of the first notice and any subsequent violations.

- Send the completed letter via certified or registered mail with return receipt requested.

Notarization requirements for this form

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to provide accurate details about the debt collector and the violation.

- Not sending the letter through certified mail to maintain proof of communication.

- Neglecting to keep copies of the notice and any related complaint letters.

Advantages of online completion

- Convenience of immediate access and downloading options in Word or Rich Text format.

- Editability to customize the letter for specific situations.

- Reliable format ensuring compliance with legal standards.

Legal use & context

- This form serves to assert your rights as a consumer under federal law.

- Documenting unfair practices can strengthen your case if further legal action is needed.

- Sending this notice by certified mail provides proof of communication.

- Persistent violations may lead to civil claims for damages as allowed by the FDCPA.

Looking for another form?

Form popularity

FAQ

Harassment of the debtor by the creditor More than 40 percent of all reported FDCPA violations involved incessant phone calls in an attempt to harass the debtor.

If a debt collector violates the FDCPA, you may sue that collector in state or federal court. You can even sue in small claims court. You must do this within one year from the date on which the violation occurred.The court might also order the debt collector to stop engaging in certain collection activities.

Protects against harassment, including excessive phone calls, abusive language and threats of violence, harm or arrest. Allows consumers to seek proof that they owe the money the debt collector wants.

Debt collectors must be truthful The Fair Debt Collection Practices Act states that debt collectors cannot use any false, deceptive or misleading representation to collect the debt. Along with other restrictions, debt collectors cannot misrepresent: The amount of the debt. Whether it's past the statute of limitations.

When a debt collector calls, it's important to know your rights and what you need to do. The FTC enforces the Fair Debt Collection Practices Act (FDCPA), which makes it illegal for debt collectors to use abusive, unfair, or deceptive practices when they collect debts.

Under the Fair Debt collection Practices Act (FDCPA), I have the right to request validation of the debt you say I owe you. I am requesting proof that I am indeed the party you are asking to pay this debt, and there is some contractual obligation that is binding on me to pay this debt.

Never Give Them Your Personal Information. A call from a debt collection agency will include a series of questions. Never Admit That The Debt Is Yours. Even if the debt is yours, don't admit that to the debt collector. Never Provide Bank Account Information.

In the letter, reference the date of the initial contact and the method, for example, "a phone call received from your agency on April 25, 2019." You also need to provide a statement that you're requesting validation of the debt. Do not admit to owing the debt or make any reference to payment.