Purchase of common stock for treasury of company

Understanding this form

The Purchase of Common Stock for Treasury of Company form is a legal document that enables a corporation to buy back its own shares of common stock from the open market. This form helps companies manage their stock option plans and employee compensation agreements while avoiding dilution of existing shareholders' interests. Unlike other share purchase agreements, this form specifically addresses the acquisition of stock for treasury purposes, which can be critical for maintaining financial balance within a company.

What’s included in this form

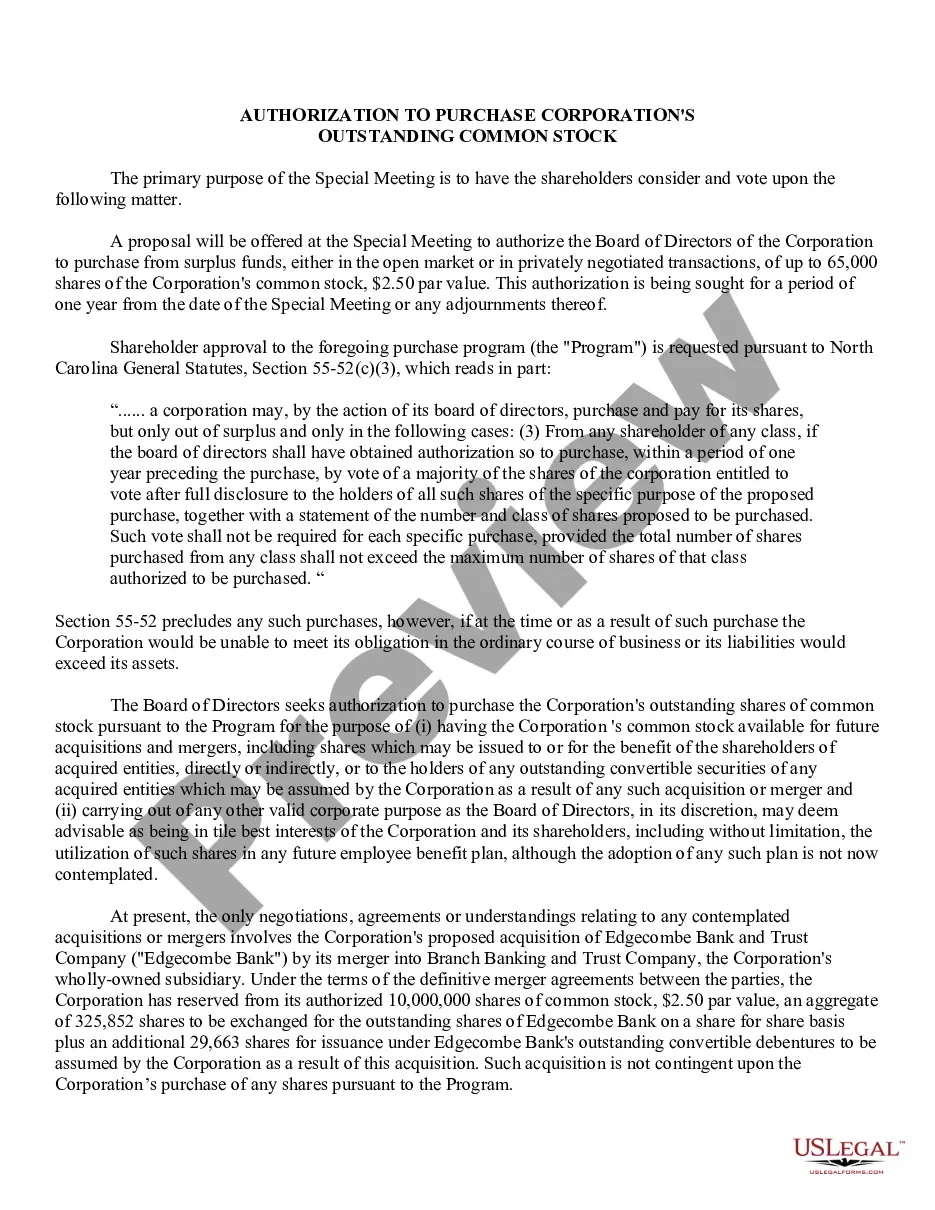

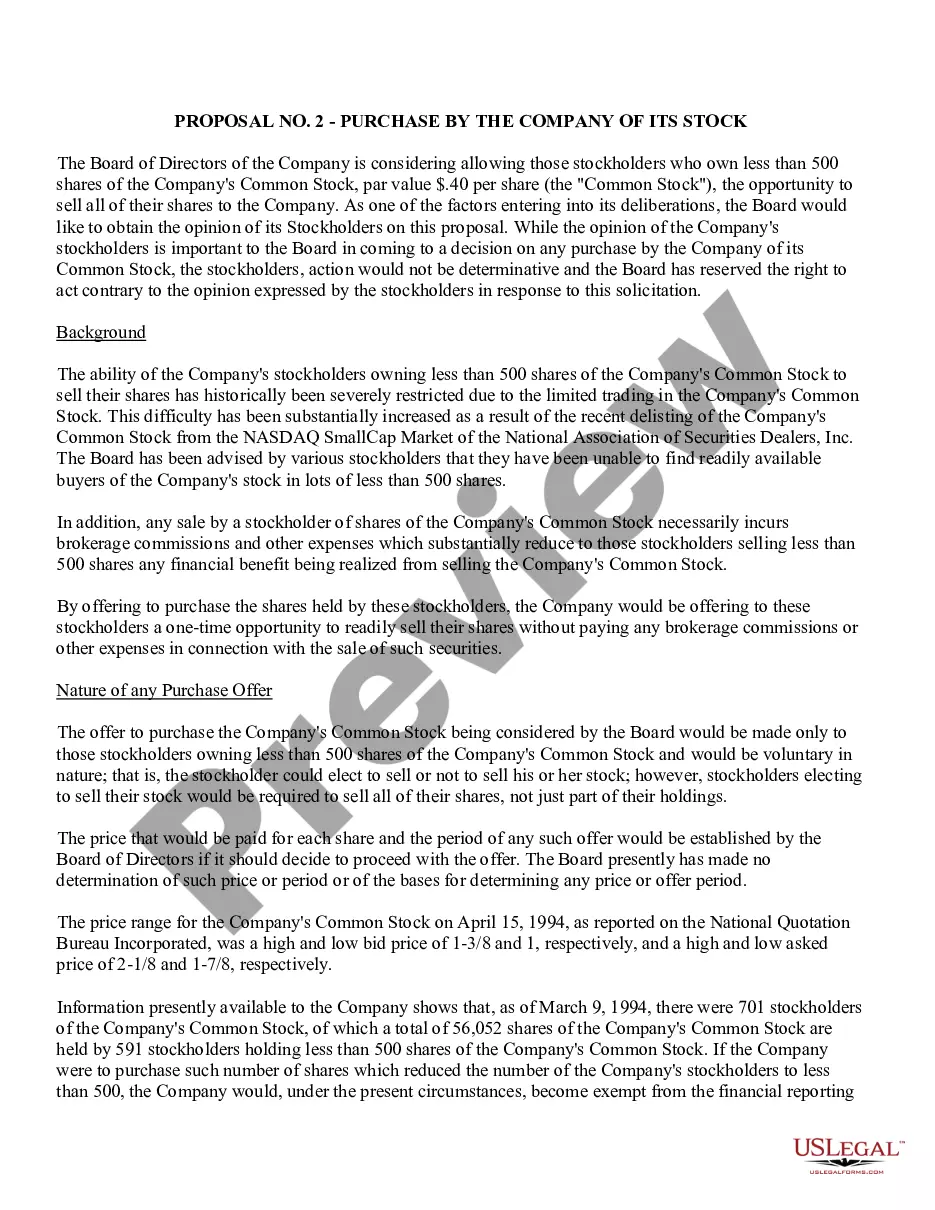

- Resolution presentation for shareholder approval

- Specifications regarding the number of shares to be purchased

- Terms and conditions of the stock purchase

- Regulatory compliance with federal and state laws

- Clarification on the purpose of treasury shares

- Voting requirements for shareholder approval

When this form is needed

This form should be used when a company seeks to repurchase its own common stock. It's specifically useful during annual meetings when companies need to secure shareholder approval for such actions. Typical scenarios include funding employee stock option plans, meeting deferred compensation obligations, or ensuring that existing shareholders' equity remains intact by preventing dilution from new stock issues.

Who this form is for

- Corporate directors and officers who represent the company

- Shareholders who need to understand the resolution being presented for approval

- Legal teams advising on corporate governance and compliance issues

- Financial officers responsible for managing stock options and treasury shares

How to complete this form

- Draft the resolution for the shareholder meeting outlining the purchase details.

- Specify the maximum number of shares to be purchased and applicable terms.

- Ensure compliance with federal securities laws and relevant state regulations.

- Present the proposal to shareholders and conduct a vote.

- Document the results of the vote and act accordingly if the proposal is approved.

Does this document require notarization?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to specify the total number of shares intended for purchase.

- Not adhering to state-specific voting requirements for shareholder approvals.

- Omitting necessary compliance checks with federal securities laws.

- Neglecting to include terms or conditions affecting the stock purchase.

Benefits of completing this form online

- Convenience of immediate access to the legal form you need.

- Editability to customize the form for specific business needs.

- Reliability with forms drafted by licensed attorneys to ensure legal integrity.

- Quick download and easy storage for future reference.

Legal use & context

- This form is essential for corporations looking to repurchase shares while adhering to legal standards.

- It provides a structured method for complying with employee compensation commitments without increasing stock supply.

- Maintains shareholder confidence by preventing dilution through careful stock management.

Key takeaways

- The Purchase of Common Stock for Treasury form is crucial for companies managing employee stock options.

- Proper approval and adherence to legal standards are necessary to avoid common pitfalls.

- Using this form online streamlines the process, ensuring that corporate actions are both effective and compliant.

Looking for another form?

Form popularity

FAQ

The entry to record the issuance of common stock at a price above par includes a debit to Cash. Cash is increased (debit) by the issue price. The journal entry would also include a credit to both Common Stock (increased) and Paid-In Capital in Excess of Par--Common Stock (increased).

If the corporation sells any of its treasury stock for less than its cost, the cash received is debited to Cash, the cost of the shares sold is credited to Treasury Stock, and the difference ("loss") is debited to Paid-in Capital from Treasury Stock (so long as the balance in that account will not become a debit

Common stock is reported in the stockholder's equity section of a company's balance sheet.

To record the stock purchase, the accountant debits Investment In Company and credits Cash. At the end of each period, the accountant evaluates the value of the investment. If the value declined, the accountant records an entry debiting Impairment of Investment in Company and credits Investment in Company.

Common stock. The sale of the stock is recorded by increasing (debiting) cash and increasing (crediting) common stock by $5,000.

To record a repurchase, simply record the entire amount of the purchase in the treasury stock account. Resale. If the treasury stock is resold at a later date, offset the sale price against the treasury stock account, and credit any sales exceeding the repurchase cost to the additional paid-in capital account.

Purchase: The journal entry is to debit treasury stock and credit cash for the purchase price. For example, if a company buys back 10,000 shares at $5 per share, the amount debited and credited is $50,000 (10,000 x $5).

There are mainly two methods of accounting for treasury stock: the cost method and the par value method.