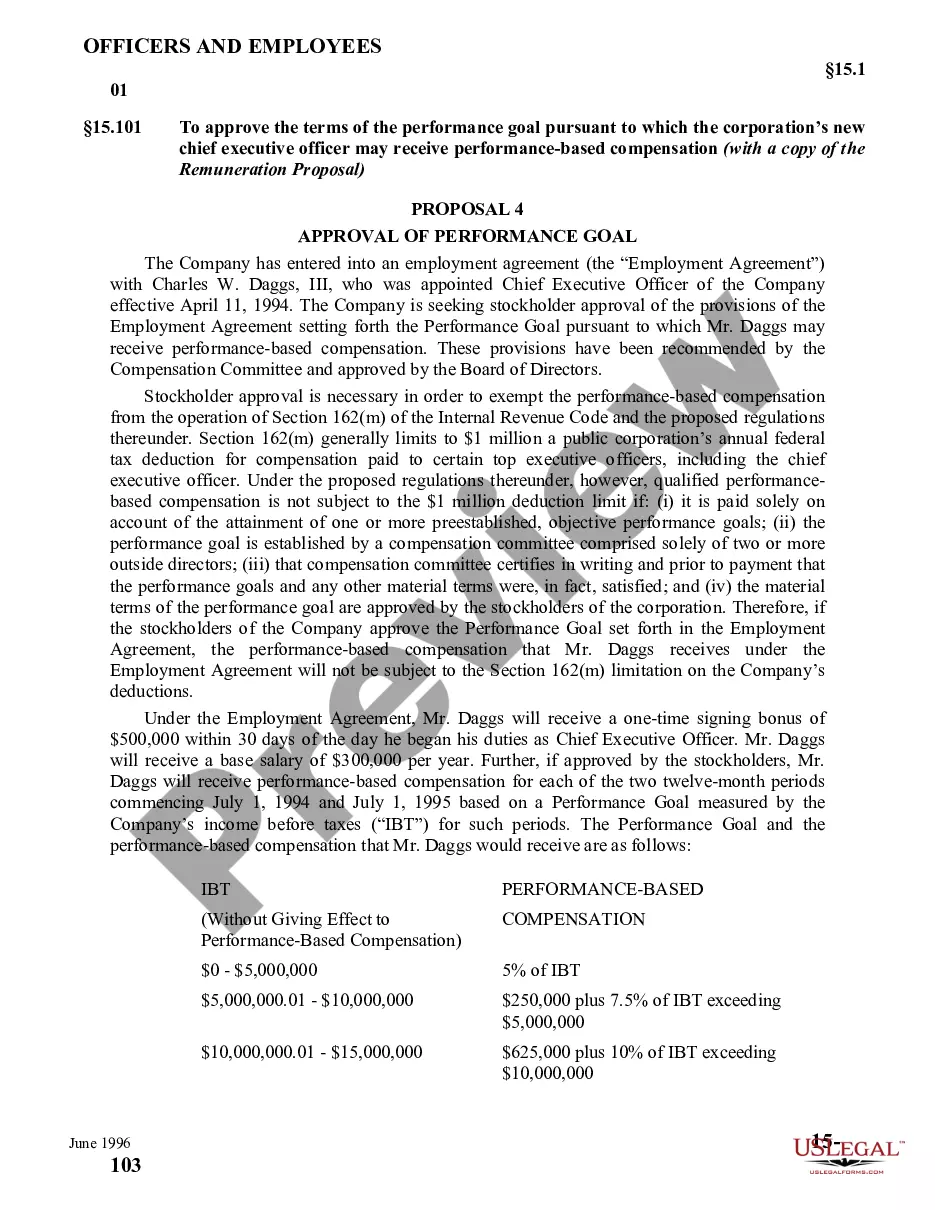

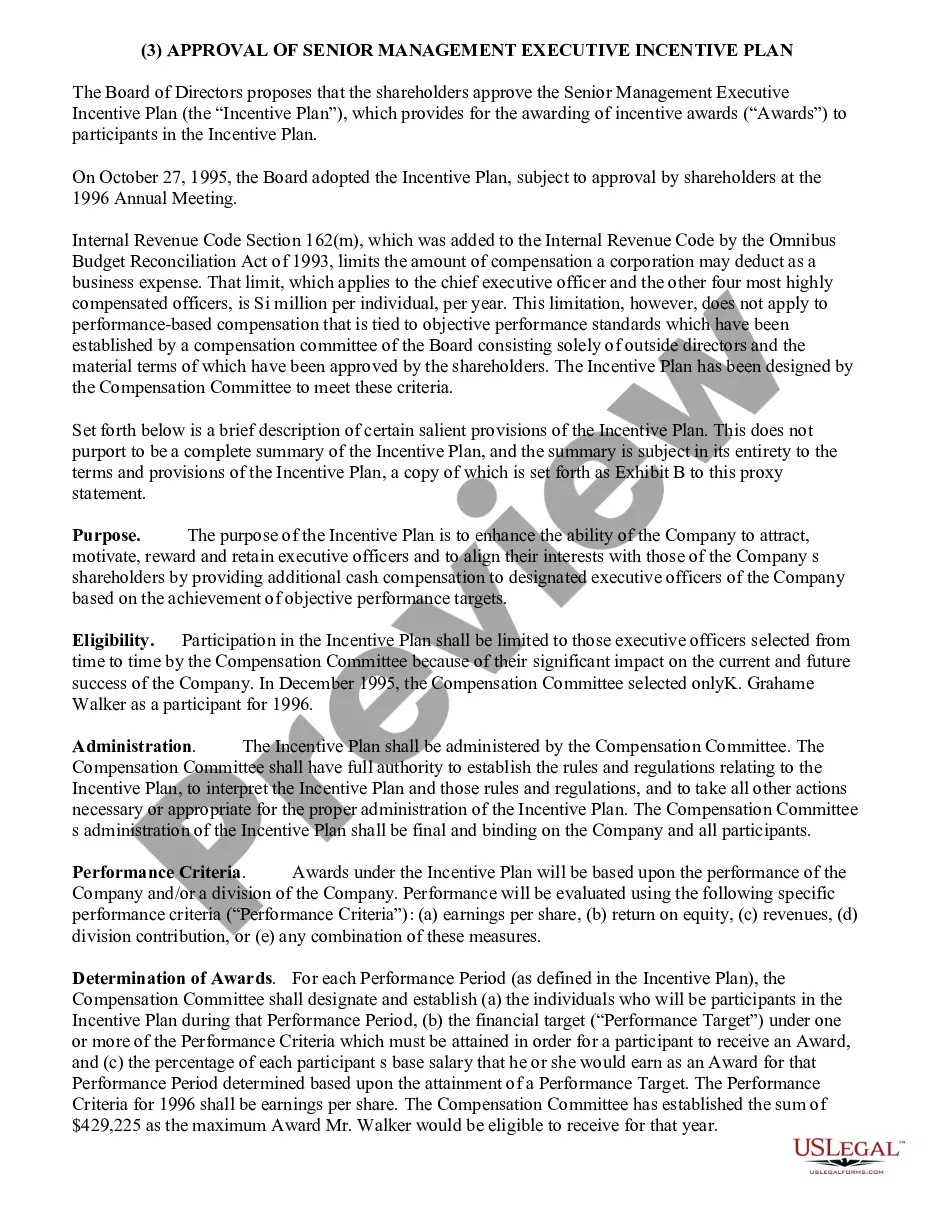

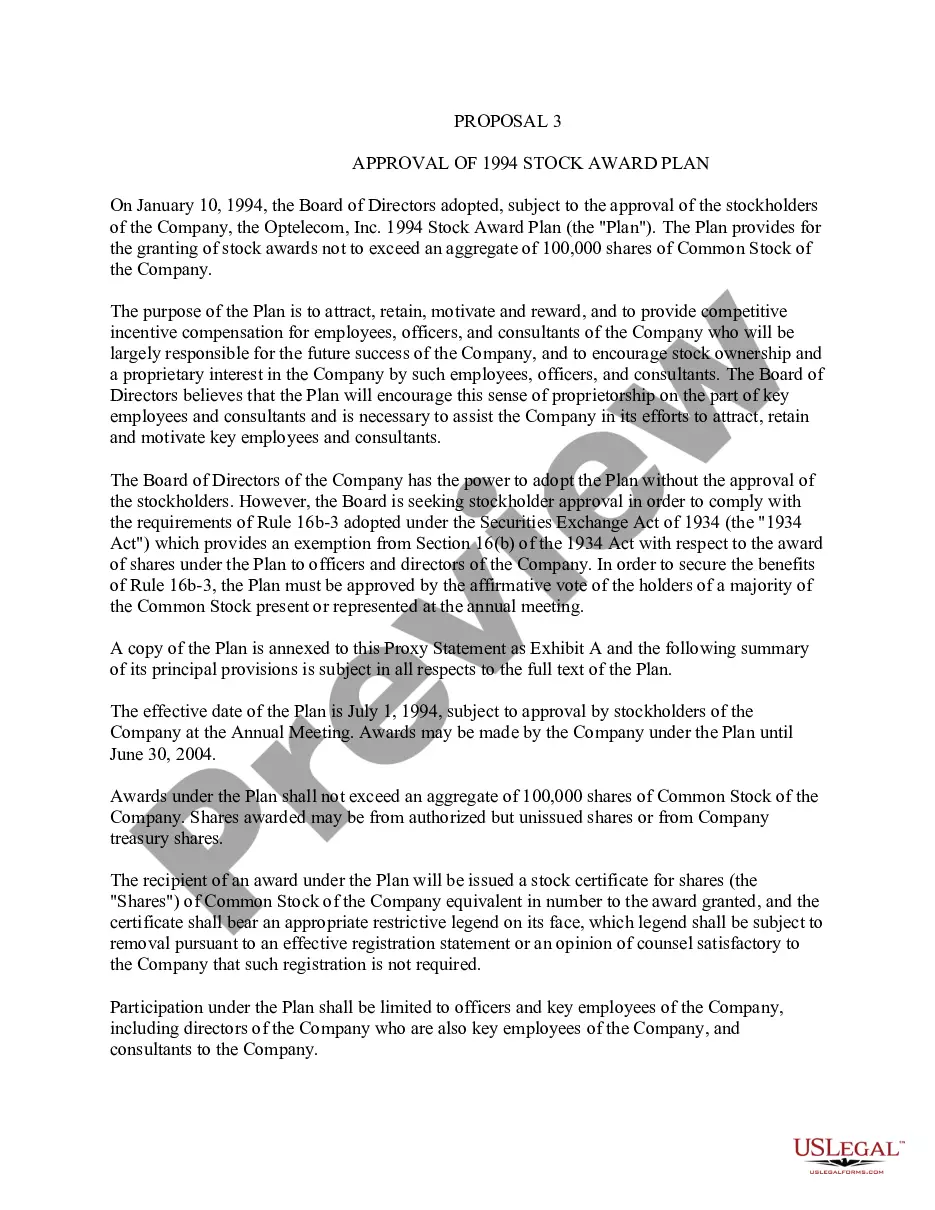

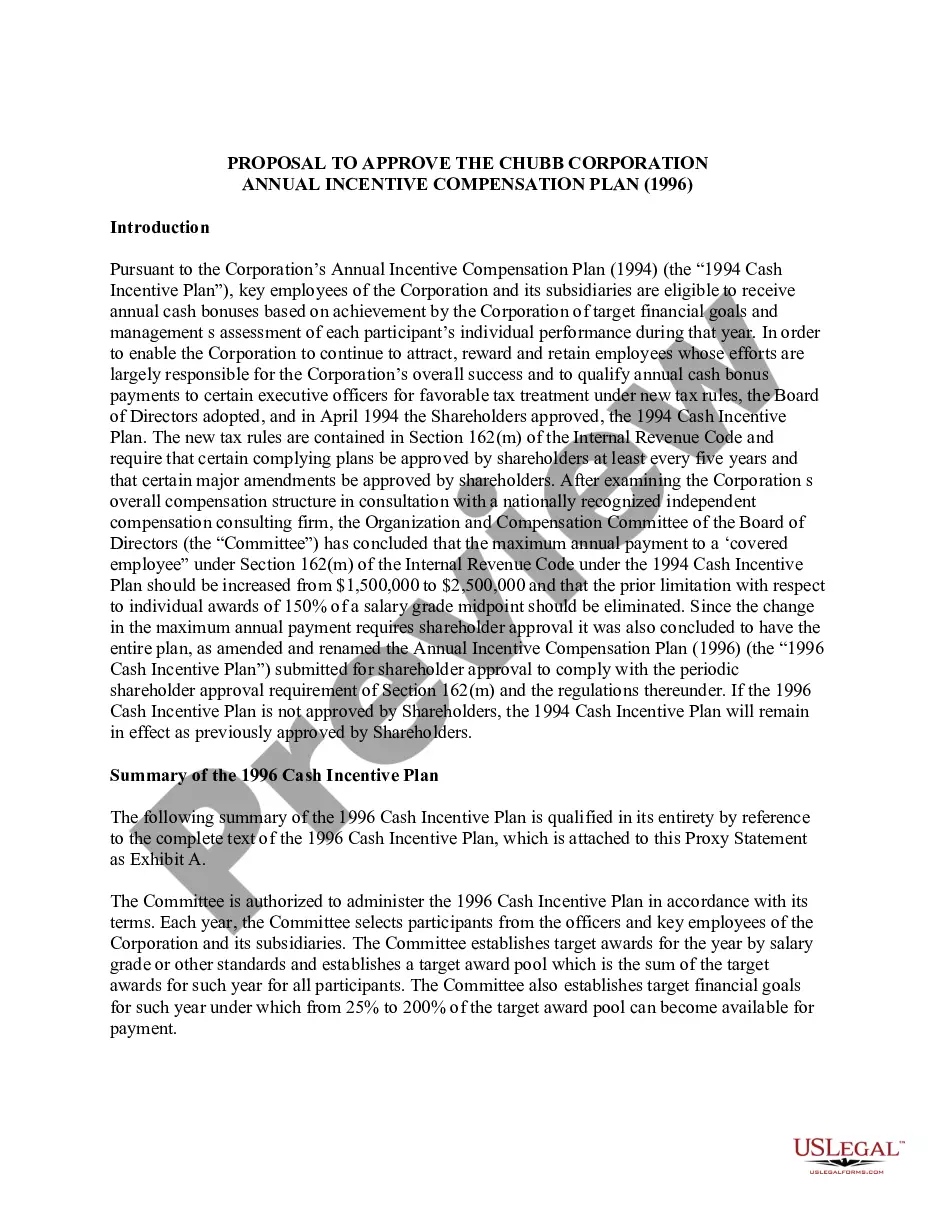

Approval of performance goals for bonus

Overview of this form

The Approval of Performance Goals for Bonus form is a legal document used by corporations to establish and gain shareholder approval for performance goals tied to executive bonuses. This form ensures that compensation based on these goals is fully deductible under federal tax laws. It navigates the nuances of corporate compensation, distinguishing itself from other financial forms by its specific focus on performance metrics and shareholder approval.

Key parts of this document

- Sections outlining the performance goals to be measured.

- Details about the compensation committee's authority and composition.

- Required disclosures to shareholders regarding material terms.

- Affirmative vote requirements for shareholder approval.

- Maximum bonus limits for executive officers except Group Executives.

When this form is needed

This form is needed when a corporation seeks to align executive compensation with company performance by establishing specific objectives. It should be used prior to a shareholder meeting where bonuses based on these goals will be discussed. Corporations must have this documentation ready to ensure compliance with tax regulations and to facilitate transparency with shareholders concerning executive compensation.

Who needs this form

This form is primarily for:

- Corporate boards of directors.

- Compensation committees within publicly held corporations.

- Shareholders involved in voting on executive compensation plans.

Instructions for completing this form

- Identify the performance goals that will be the basis for executive bonuses.

- Detail the composition and authority of the compensation committee.

- Clearly disclose the material terms and conditions to be approved by shareholders.

- Set limits on the maximum bonus allowable for each executive officer.

- Prepare for a shareholder vote on the proposed performance goals and conditions.

Does this form need to be notarized?

In most cases, this form does not require notarization. However, some jurisdictions or signing circumstances might. US Legal Forms offers online notarization powered by Notarize, accessible 24/7 for a quick, remote process.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to adequately define performance goals leading to ambiguity.

- Not fully disclosing material terms, risking shareholder disapproval.

- Neglecting to ensure a majority vote is secured before payout decisions.

- Overlooking the required composition of the compensation committee.

Why complete this form online

- Convenient access to templates that are easy to modify to fit specific needs.

- Quickly downloadable and printable for immediate use.

- Ensures compliance with federal regulations while accommodating corporate governance structures.

Legal use & context

- This form is legally binding once duly completed and approved by shareholders.

- It supports the corporation's compliance with federal income tax laws related to executive compensation.

- Failure to follow the proper procedures highlighted in this form can result in tax penalties for excessive compensation payments.

Quick recap

- The Approval of Performance Goals for Bonus form is essential for determining executive compensation strategy.

- Shareholder approval is crucial for ensuring tax deductibility of bonuses based on performance metrics.

- Clear, measurable performance goals increase transparency in executive compensation.

Looking for another form?

Form popularity

FAQ

How to Calculate a Bonus. To calulate a bonus based on your employee's salary, just multiply the employee's salary by your bonus percentage. For example, a monthly salary of $3,000 with a 10% bonus would be $300.

Calculation for Bonus PayableCalculation of bonus will be as follows: If Salary is equal to or less than Rs. 7000/- then the bonus is calculated on the actual amount by using the formula: Bonus = Salary x 8.33/100.

A company sets aside a predetermined amount; a typical bonus percentage would be 2.5 and 7.5 percent of payroll but sometimes as high as 15 percent, as a bonus on top of base salary.It will also make you look good to your manager if you show an interest in the company's performance.

In accordance with the terms of the Principal Act, every employee who draws a salary of INR 10,000 or below per month and who has worked for not less than 30 days in an accounting year, is eligible for bonus (calculated as per the methodology provided under the Principal Act) with the floor of 8.33% of the salary

THE PAYMENT OF BONUS ACT, 1965 The minimum bonus of 8.33% is payable by every industry and establishment under section 10 of the Act. The maximum bonus including productivity linked bonus that can be paid in any accounting year shall not exceed 20% of the salary/wage of an employee under the section 31 A of the Act. 1.

Know how much money you have available for the bonus plan. Base the plan on quantifiable, measurable results. Consider setting tiered goals so that employees can reach different bonus levels by achieving more difficult goals. Put your bonus plan in writing.

Eligibility for bonus. Every employee shall be entitled to be paid by his employer in an accounting year, bonus, in accordance with the provisions of this Act, provided he has worked in the establishment for not less than thirty working days in that year.

The Payment of Bonus Act, 1965 provides for a minimum bonus of 8.33 percent of wages. The salary limited fixed for eligibility purposes is Rs. 3,500 per month and the payment is subject to the stipulation that the bonus payable to employees drawing wages or salary not exceeded to Rs.