Revocable Trust Agreement with Husband and Wife as Trustors and Income to

What is this form?

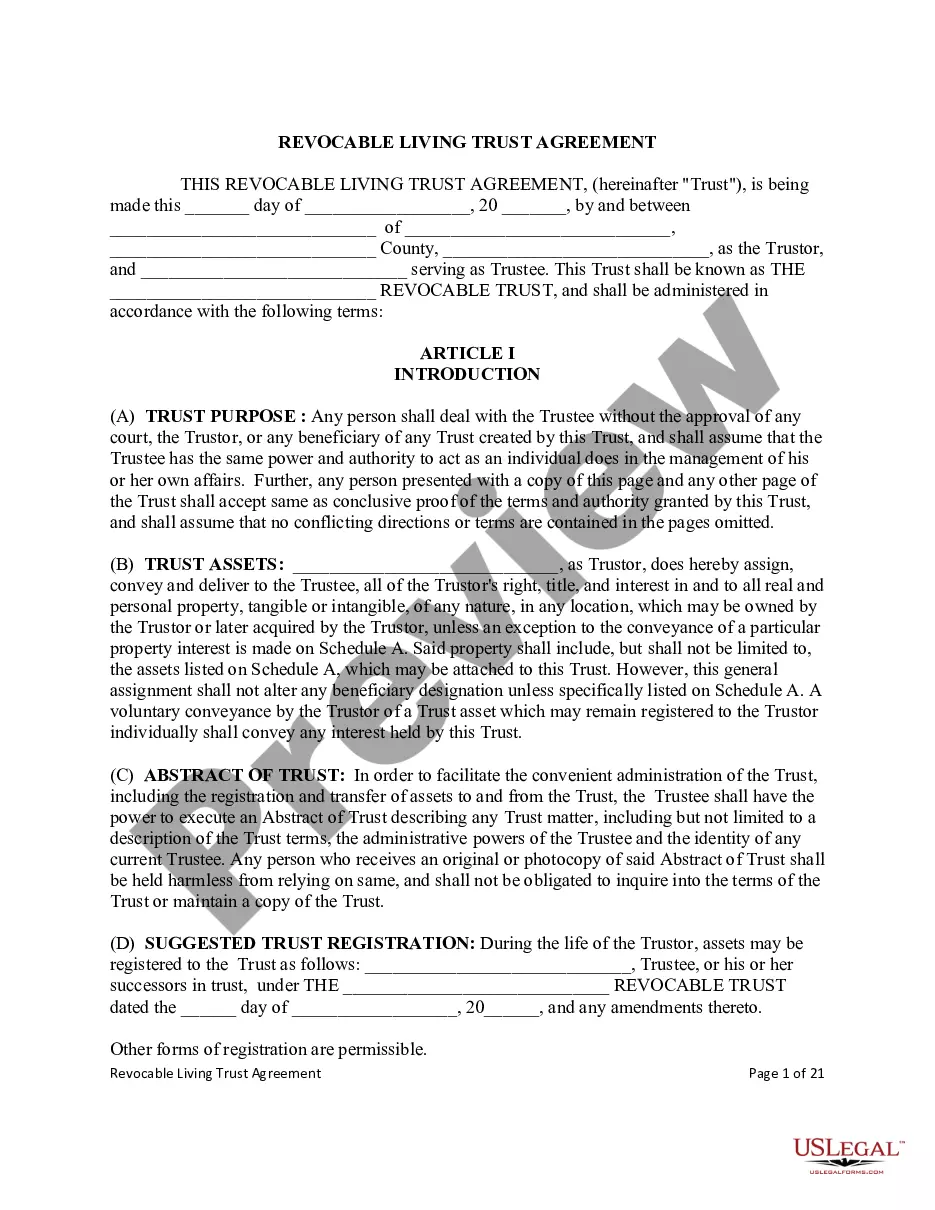

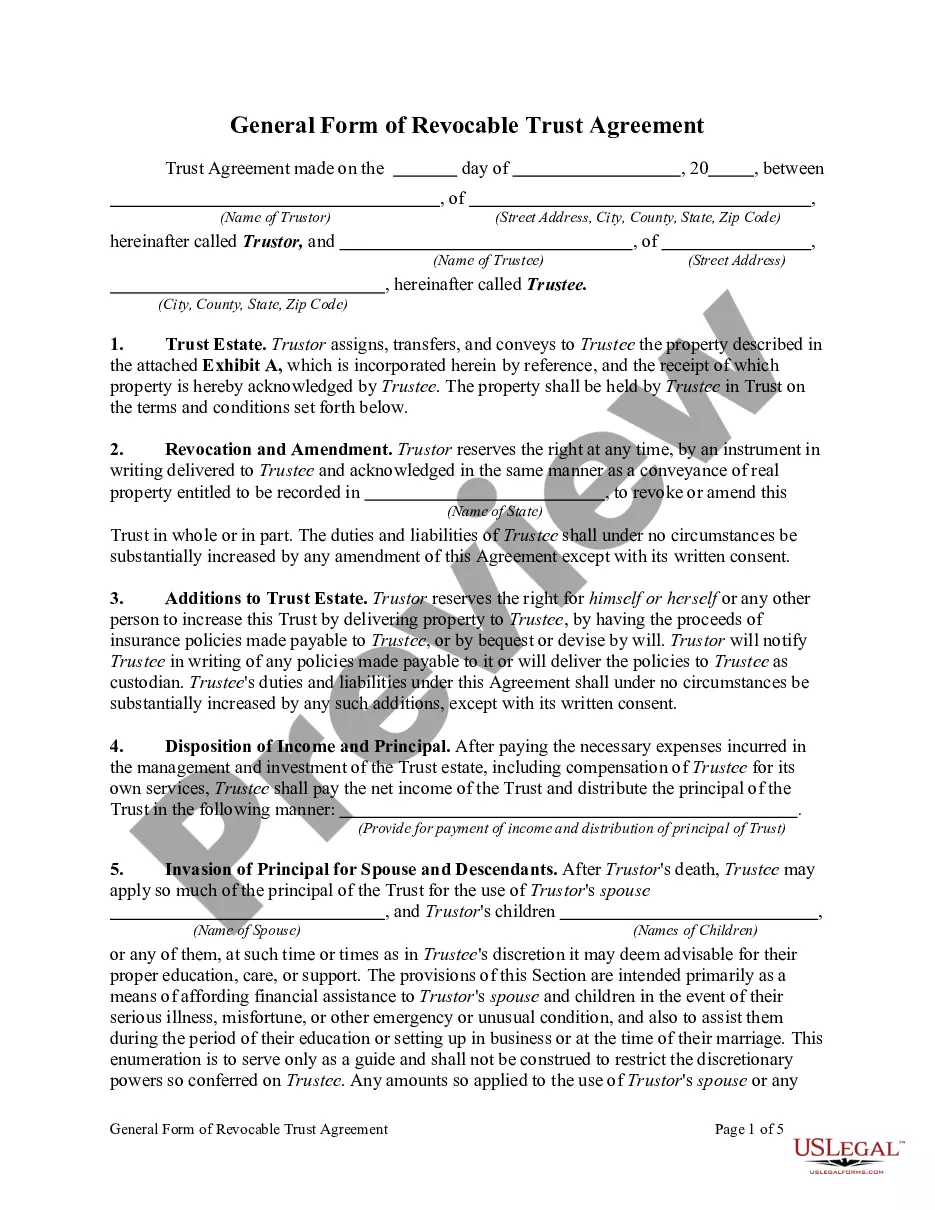

The Revocable Trust Agreement with Husband and Wife as Trustors is a legal document that establishes a revocable living trust. This type of trust allows the trustors, typically a married couple, to manage their assets during their lifetime and specify how they are distributed upon their passing. The key advantage of a revocable trust is that it can be altered or terminated by the trustors at any time, offering flexibility not found in irrevocable trusts. It is crucial for estate planning as it can help avoid probate and manage income during the trustors' lifetimes.

Form components explained

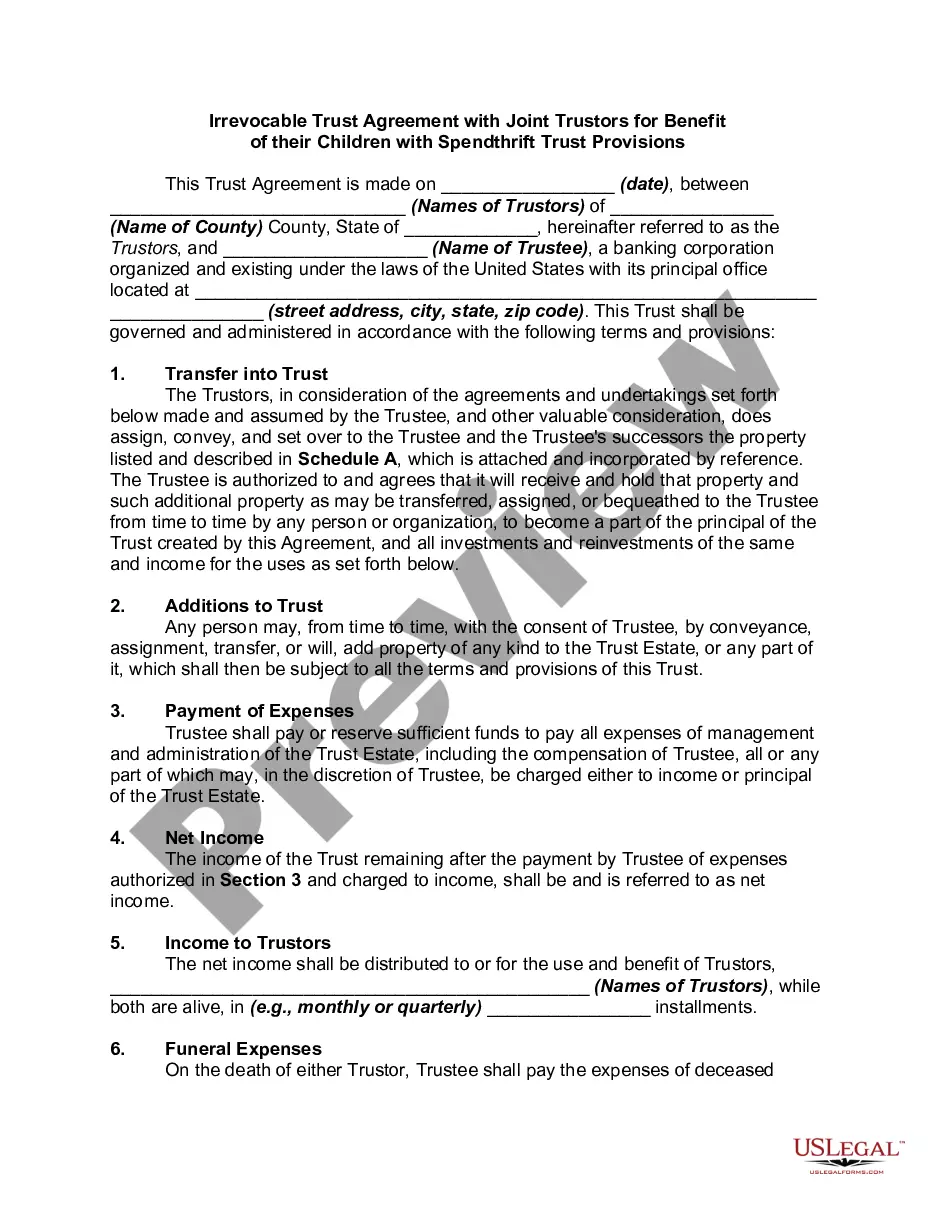

- Identification of the Trustors and Trustee.

- Transfer of property into the trust.

- Provision for amendments and revocations by the Trustors.

- Distribution of income to Trustors during their lifetimes.

- Instructions for trust termination and property distribution to beneficiaries.

- Provisions for payment of expenses and taxes related to the trust.

When to use this document

This form is typically used when a married couple wishes to establish a revocable living trust to manage their assets. It is beneficial for those looking to ensure a smooth transfer of assets after death, provide for their financial needs during their lifetime, specify how their assets will be distributed to their children or other beneficiaries, and potentially avoid the complications of probate court.

Who this form is for

- Married couples who want to manage their assets collectively.

- Individuals seeking to establish a flexible estate plan.

- Those with children or dependents they want to provide for after passing.

- Individuals concerned about the probate process after death.

Instructions for completing this form

- Identify the Trustors by entering their names and the county and state of residence.

- Designate the Trustee by providing the corporate name and location.

- Transfer assets into the trust by detailing properties in the attached Schedule A.

- Specify how income will be distributed to the Trustors during their lifetimes.

- Indicate how the trust will be managed and terminated after the surviving Trustor passes away.

- Ensure all signatures are completed and consider notarization as per local laws.

Notarization guidance

This form does not typically require notarization unless specified by local law. It is advisable to check your stateâs requirements to ensure validity.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to transfer assets into the trust after its creation.

- Not specifying clear instructions for distribution of assets after death.

- Neglecting to update the trust as financial situations or family dynamics change.

- Overlooking required signatures or notarization where applicable.

Advantages of online completion

- Convenience of immediate access to legal documents without needing to visit a lawyer.

- Editability allows you to customize the form to fit your specific needs.

- Reliability in using professionally drafted templates designed to comply with current laws.

- A Revocable Trust Agreement allows for flexible management of married couples' assets.

- This form helps avoid probate, making asset transfer smoother after death.

- Consult state laws to ensure compliance and validity of the trust.

Looking for another form?

Form popularity

FAQ

This Revocable Trust Agreement With Husband and Wife as Trustors forms a revocable living trust for a married couple. It lets both spouses manage assets during life, amend or revoke the trust as needed, and specify how income is paid to them while they live. It also provides for transferring property into the trust and distributing assets to heirs after death, potentially avoiding probate.

Yes. This form is designed for married couples to act as trustors in a revocable living trust. It names both spouses as trustors and covers how income is distributed to them during their lifetimes, how property is transferred into the trust, and how the trust may be amended or revoked, with assets eventually distributed to beneficiaries.

This form is drafted for a joint revocable trust with both spouses as trustors. If you prefer separate trusts, you would typically use individual documents. A joined trust can simplify management and streamline how assets are funded and distributed, but may not fit every family situation. An attorney can tailor the approach.

For many married couples, a revocable living trust is a flexible option. This form provides joint trustors, lifetime income distributions to the trustors, and a clear path for transferring assets into the trust and distributing them to beneficiaries, all while allowing amendments or revocation if plans change.

Common mistakes include failing to properly identify the trustors and trustee, not transferring property into the trust, and lacking clear instructions for amendments and revocation. This form lists identification, transfer of property, and amendment provisions to help prevent these issues and ensure assets are managed and distributed as intended.

This document is tailored for a married couple who both serve as trustors and specifies income to be paid to the trustors during lifetimes, plus explicit provisions for amendments, revocations, and distributions to beneficiaries. A broader 'joint revocable trust' may not include the same explicit income-to-trustor language or be drafted with these specific provisions.