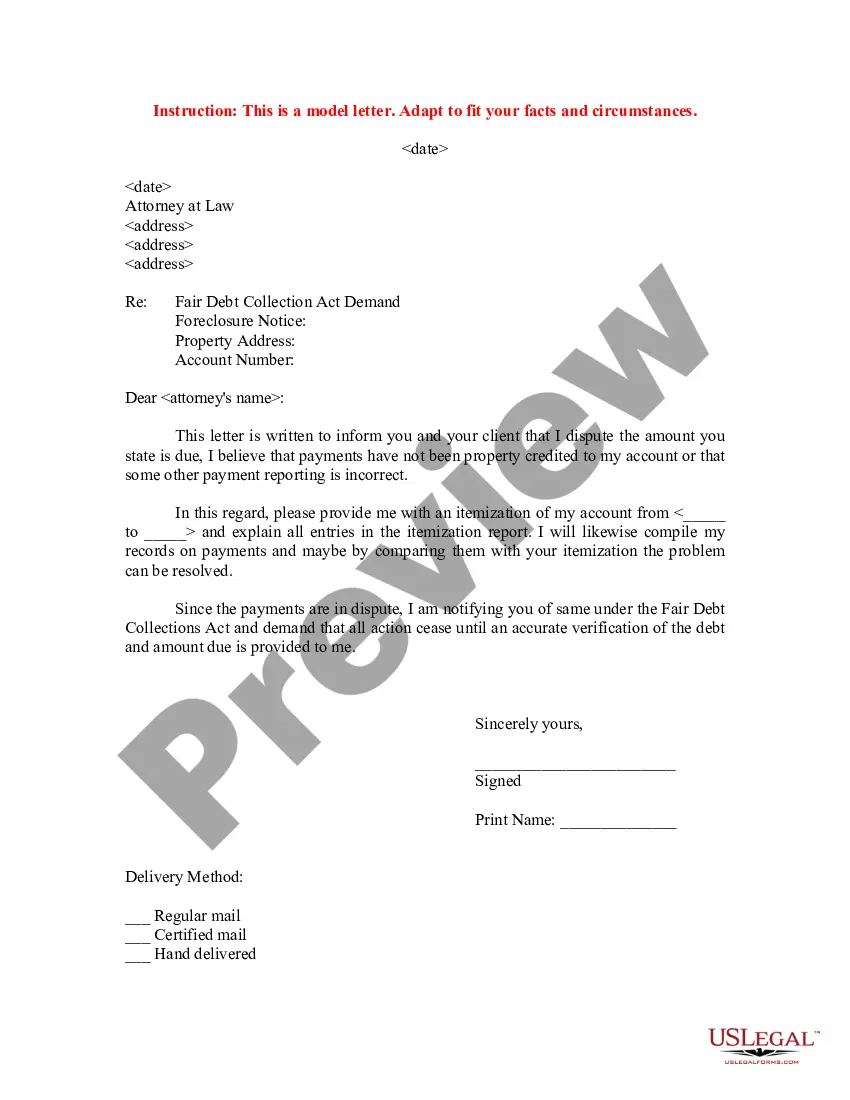

Letter to Foreclosure Attorney - Payment Dispute

Overview of this form

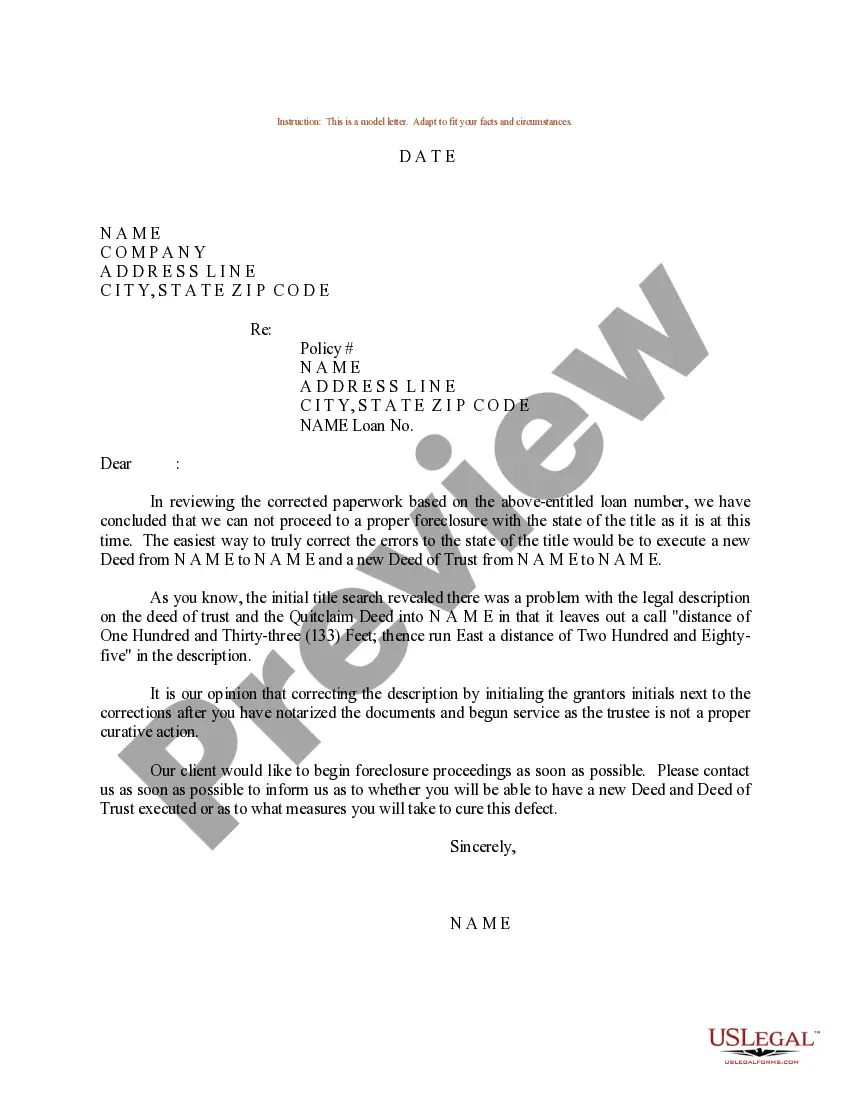

This Letter to Foreclosure Attorney - Payment Dispute is a formal communication used to dispute the amount claimed by a creditor regarding a foreclosure. It serves to request an itemized account of payments and demand clarification on any discrepancies. Unlike other foreclosure-related forms, this letter specifically addresses payment disputes and seeks verification before further action can proceed.

Key parts of this document

- Sender's information: Include your name and address.

- Recipient's details: Specify the attorney's name and address.

- Property address and account number: Essential for identifying the relevant foreclosure account.

- Statement of dispute: Clearly articulate your disagreement with the claimed amount.

- Request for itemization: Ask for a detailed breakdown of payments made and their application.

- Demand that actions cease: Indicate that all legal actions must be paused until proper verification is provided.

When to use this form

Consider using this form if you receive a foreclosure notice and believe that the amount listed is incorrect. This situation may arise if you suspect errors in payment processing or if you feel that your payments have not been accurately credited. By sending this letter, you can formally dispute the claim and seek clarification, which can prevent any further actions from the creditor until the issue is resolved.

Who can use this document

- Homeowners facing foreclosure who believe their payment records are inaccurate.

- Individuals who wish to formally dispute a claimed debt in the foreclosure process.

- Anyone seeking verification of a debt before allowing further legal proceedings to continue.

Steps to complete this form

- Fill in your name and address at the top of the letter.

- Write the attorney's name and address beneath your information.

- Include the property address and account number to specify the dispute.

- Clearly state your dispute regarding the payment amount, highlighting concerns about miscredited payments.

- Request an itemized account from a specified start date to an end date.

- Sign the letter and choose your preferred delivery method (regular mail, certified mail, or hand delivery).

Does this document require notarization?

Notarization is generally not required for this form. However, certain states or situations might demand it. You can complete notarization online through US Legal Forms, powered by Notarize, using a verified video call available anytime.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to provide accurate account and property details.

- Not specifying the dates for the request of the itemization.

- Overlooking to include your signature or printed name.

- Not using a clear and respectful tone, which can hinder communication.

Benefits of completing this form online

- Access the form 24/7 from any location with internet connectivity.

- Easily editable to cater to personal details and situation specifics.

- Reliable templates drafted by licensed attorneys, ensuring legal compliance.

- Convenience of immediate download and usage without waiting for physical delivery.

Legal use & context

- This letter serves as a formal notice to the creditor, ensuring they acknowledge the dispute.

- It is a proactive measure under the Fair Debt Collection Practices Act, potentially protecting you from unfair collection practices.

- The correct use of this form can help halt any foreclosure proceedings until the dispute is resolved.

Summary of main points

- The Letter to Foreclosure Attorney - Payment Dispute is a vital tool for homeowners disputing erroneous claims of debt.

- Using this form helps ensure clarity in communication and protects against unlawful collection efforts.

- Proper completion and delivery of this letter can facilitate a resolution to the payment dispute.

Looking for another form?

Form popularity

FAQ

Dismissal. When a judge dismisses a foreclosure case, the matter closes and the foreclosure can't proceed. Judges may dismiss foreclosure cases if the lender can't prove it owns your mortgage or if the lender didn't follow the state's foreclosure procedure correctly.

Proving Wrongful Foreclosure If you wish to sue the bank for wrongful foreclosure, you must prove the following: The lender owed you, the borrower, a legal duty. The lender breached that duty. The breach of duty caused your injury or loss (damages)

Reinstatement. Ask the lender to reinstate the loan. Forbearance Agreement. Ask the lender to forgive the debt. Refinance. Sell your home. Short Sale. LLoan modification. Deed in Lieu of Foreclosure. Rescission of loan.

Negotiate With Your Lender. If you are having financial difficulties, the worst thing that you can do is bury your head in the sand. Request a Forbearance. Modify Your Loan. Make a Claim. Get a Housing Counselor. Declare Bankruptcy. Use A Foreclosure Defense Strategy. Make Them Produce The Not.

Name, address, phone number, date, loan number. Short introduction asking for permission to sell your home in a short sale. Hardship details and neighborhood comparables. Assertion that the only other alternative is foreclosure.

In situations where a foreclosure has already occurred, the California Supreme Court held that a borrower has standing to sue for wrongful foreclosure based on an allegedly void assignment of his or her mortgage.

You can stop the foreclosure process by informing your lender that you will pay off the default amount and extra fees. Your lender would prefer to have the money much more than they would have your home, so unless there are extenuating circumstances, this should work.

Wrongful foreclosure can occur when foreclosure processing companies submit documents to courts that have not actually been signed by homeowners and bear a forged signature. This practice not only gives rise to a cause of action for wrongful foreclosure, but can result in significant criminal penalties as well.

A hardship letter should Start by stating the purpose of the letter whether it is a loan modification or a short sale so the lender knows what homeowners want. It should say something like I need to restructure my mortgage and obtain a lower, fixed interest rate2026, in a way that force them to find out why.