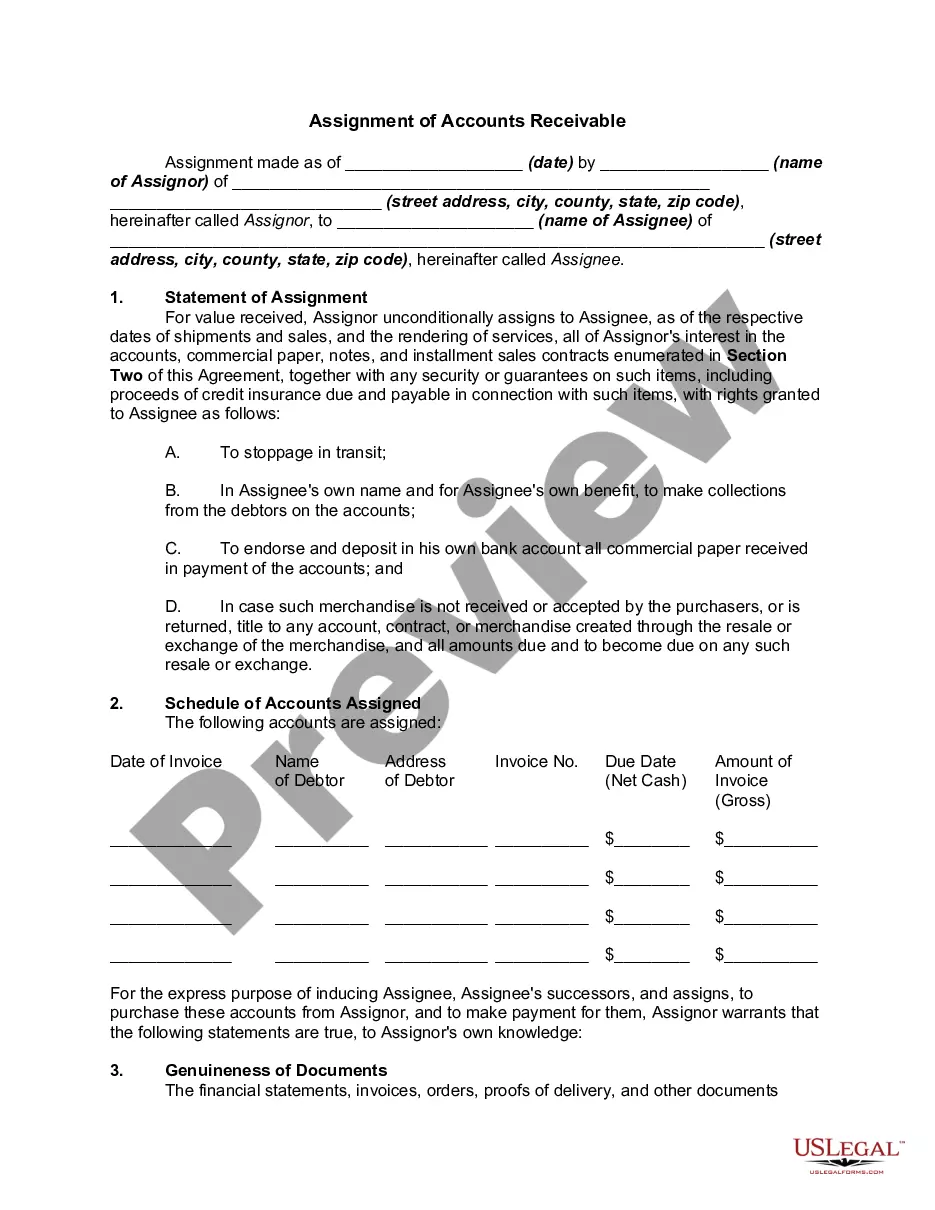

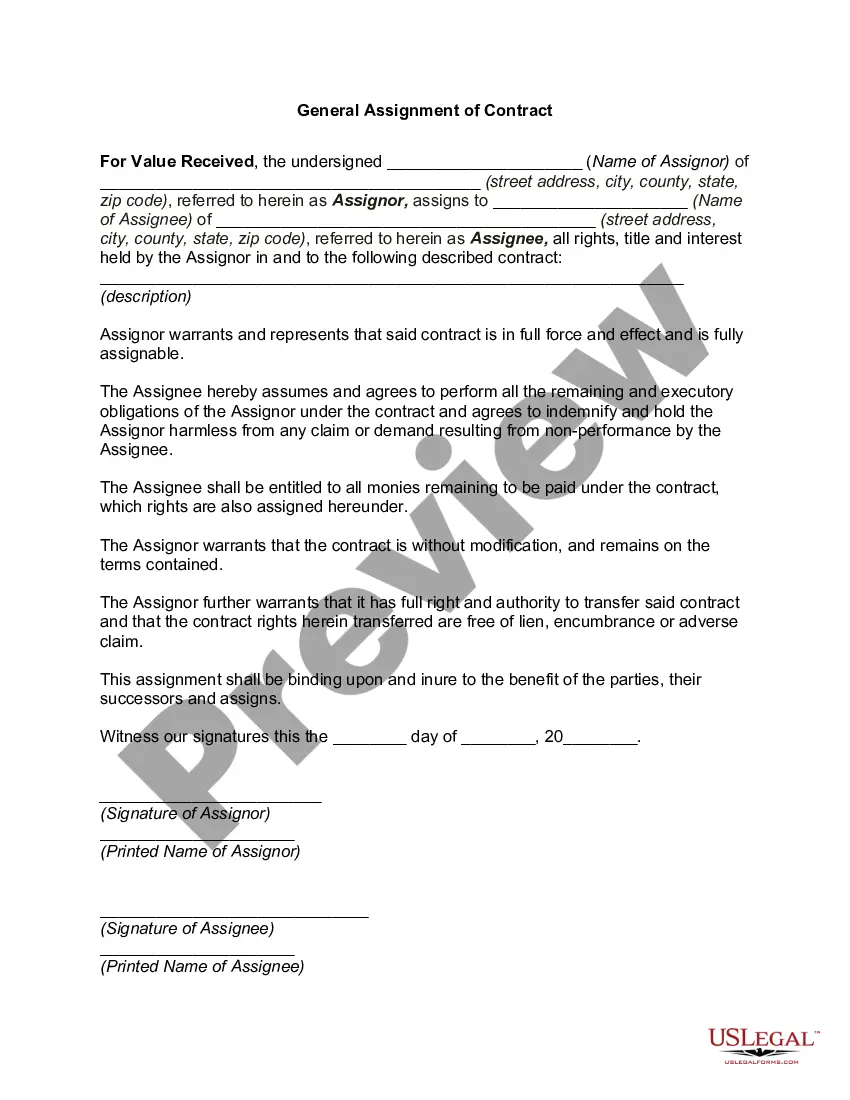

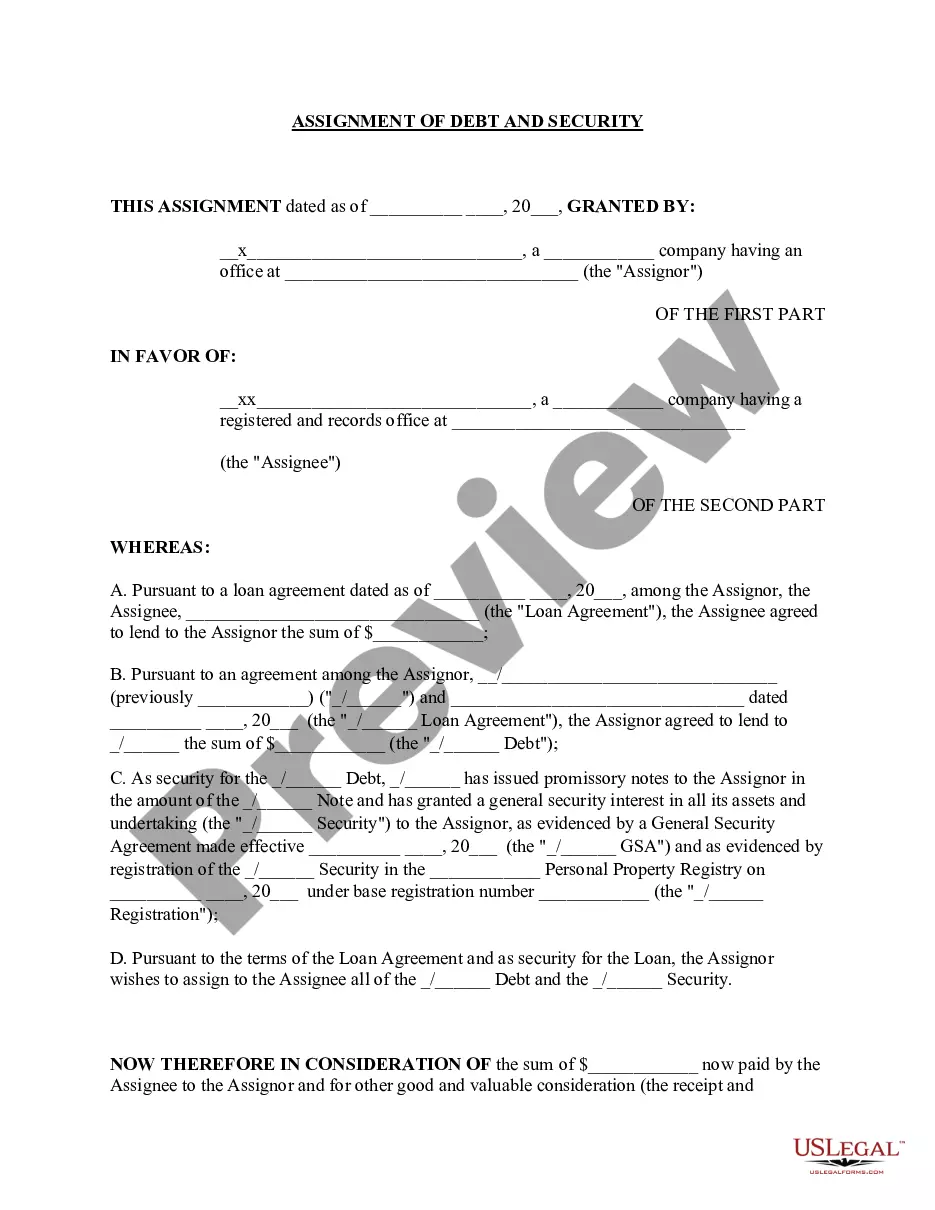

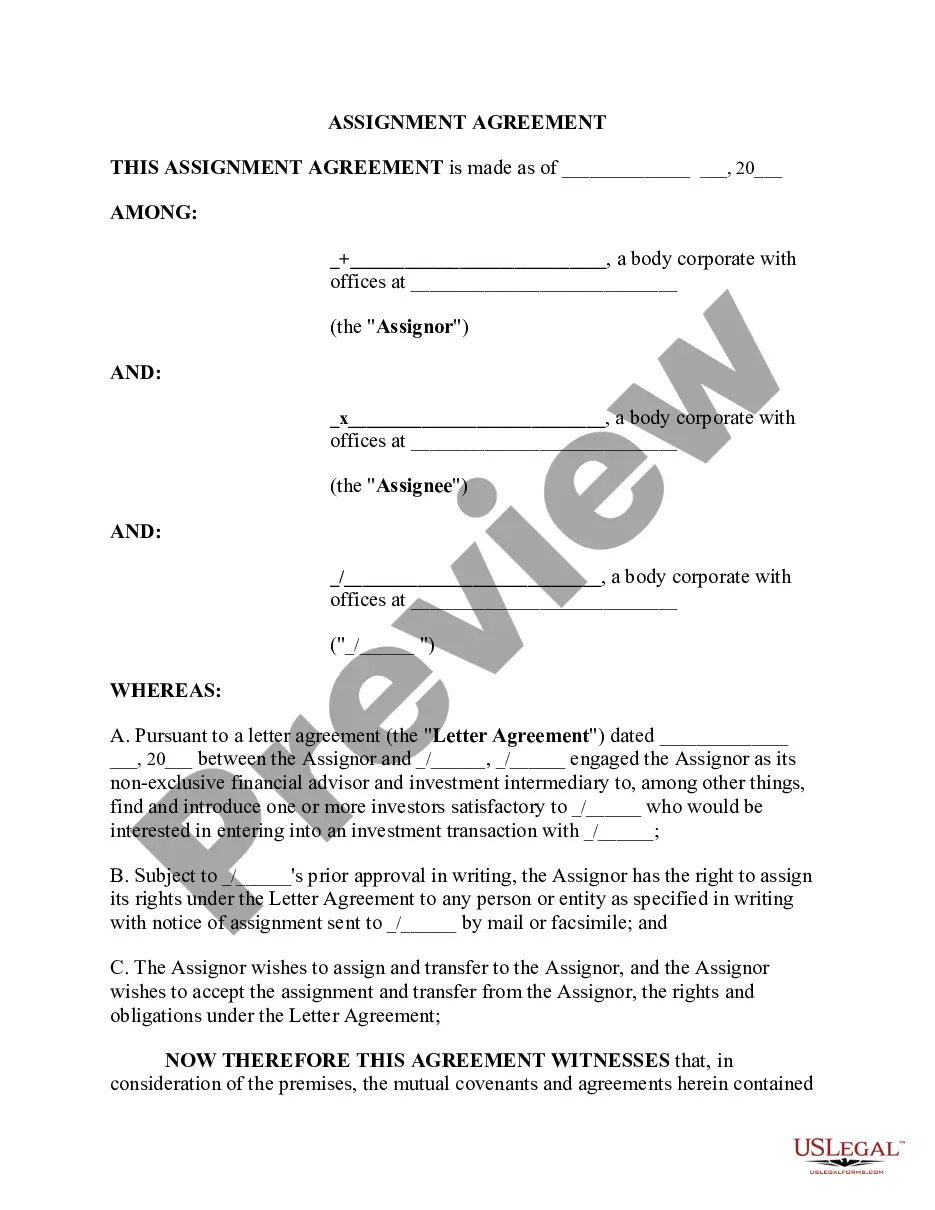

Assignment of Debt

What is this form?

The Assignment of Debt is a legal document that allows a person (the Assignor) to transfer their rights to collect a debt owed to them by another party (the Debtor) to a third party (the Assignee). This form is essential for ensuring that the debt collection rights are officially communicated and recognized, differing from other debt collection methods by creating a formal assignment rather than simply informing the debtor of a change in collection agents.

Main sections of this form

- Name and address of the Assignor (the party assigning the debt).

- Name and address of the Assignee (the party receiving the debt assignment).

- Name and address of the Debtor (the party who owes the debt).

- Description of the debt being assigned (services rendered or goods sold).

- Amount of debt due to the Assignor.

- Date of assignment and signatures of the parties involved.

When to use this document

This form should be used when a creditor wishes to assign their rights to collect a debt to another individual or entity. Common scenarios include businesses transferring receivables to a collection agency, individuals selling debts for cash, or when partners in a business decide to assign debts owed to one of them to other partners. It helps ensure that the assignment is legally recognized and enforceable.

Who needs this form

- Individuals or businesses wishing to assign debts for collection.

- Debt collectors or collection agencies acquiring rights to collect debts.

- Partners in a business who need to allocate debt rights among themselves.

- Anyone wanting to formally document a transfer of debt ownership.

Completing this form step by step

- Identify the Assignor by entering their name and contact details.

- Enter the name and address of the Assignee to whom the debt is assigned.

- Specify the name and address of the Debtor (the individual or entity owing the debt).

- Provide a clear description of the debt and the amount owed.

- Sign and date the form at the bottom to finalize the assignment.

Does this form need to be notarized?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Forgetting to include the full address of any party involved.

- Not providing a clear and specific description of the debt.

- Failing to date the document after signing it.

- Not having all parties sign the assignment form.

Why use this form online

- Convenient access to legal forms that can be completed anytime, anywhere.

- Editable forms allow you to customize the document to meet your specific needs.

- Reliable templates drafted by licensed attorneys, ensuring legal compliance.

Legal use & context

- The Assignment of Debt is a legally binding document once executed correctly.

- It allows the Assignee to pursue collection of the debt as if they were the original creditor.

- Ensure compliance with any applicable state and federal laws regarding debt assignments.

What to keep in mind

- The Assignment of Debt is essential for legally transferring debt collection rights from one party to another.

- Ensure that all relevant details about the parties involved and the debt itself are clearly documented.

- Consider the benefits of online forms for ease of use and accessibility.

Looking for another form?

Form popularity

FAQ

When you sign a credit agreement there will have been a clause within the fine print. This will have stated that they are able to assign their rights to a third party. As you have signed for this, they do not need to ask your permission to 'sell' the debt and you are unfortunately unable to dispute it.

Offer a specific dollar amount that is roughly 30% of your outstanding account balance. The lender will probably counter with a higher percentage or dollar amount. If anything above 50% is suggested, consider trying to settle with a different creditor or simply put the money in savings to help pay future monthly bills.

The Debt Settlement Agreement is a contract signed between a creditor and debtor to re-negotiate or compromise on a debt. This is usually in the case when an individual wants to make a final payment for a debt that is owed.

It is not uncommon for a creditor (assignor) to transfer their right to receive payment of a debt (assignment) to a third party (assignee).The assignee of the debt can issue to the debtor company a statutory demand for the payment of the debt if the debt exceeds the statutory minimum, which is currently $2,000.

A Notice of Assignment is used to inform debtors that a third party has 'purchased' their debt. The new company (assignee) takes over collection procedures, but can sometimes hire a debt collection agency to recover the money on their behalf. There are two types of debt assignment: Legal Assignment.

Original creditor and collection agent's company name. Date the letter was written. Your name. Your account number. Outstanding balance owed on the account (optional) Amount agreed to as settlement. Terms and amounts of payments to be made (if not a lump-sum)

Your debt settlement proposal letter must be formal and clearly state your intentions, as well as what you expect from your creditors. You should also include all the key information your creditor will need to locate your account on their system, which includes: Your full name used on the account. Your full address.

The creditor and/or debt collectors name. The date the letter was drafted. Your name. Your account number.