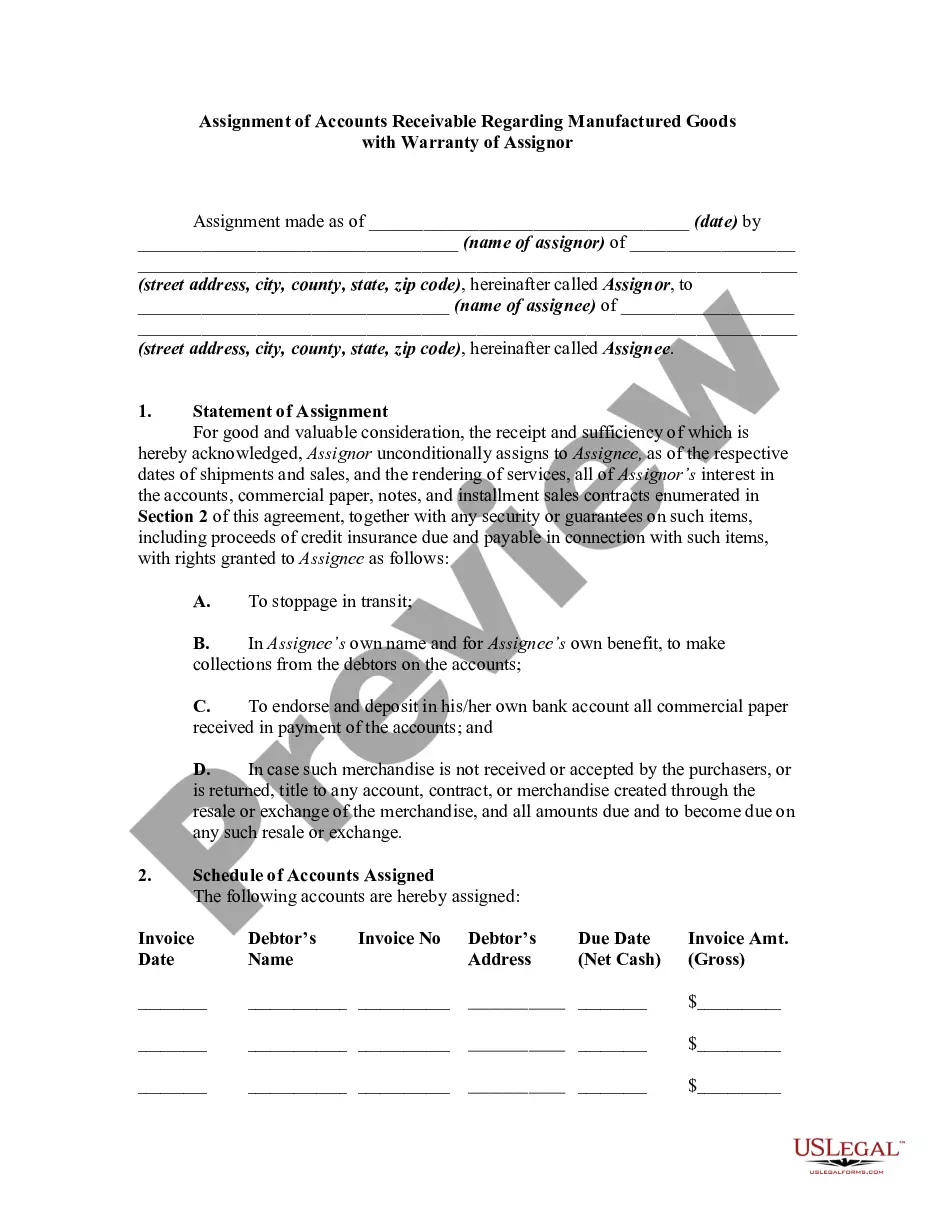

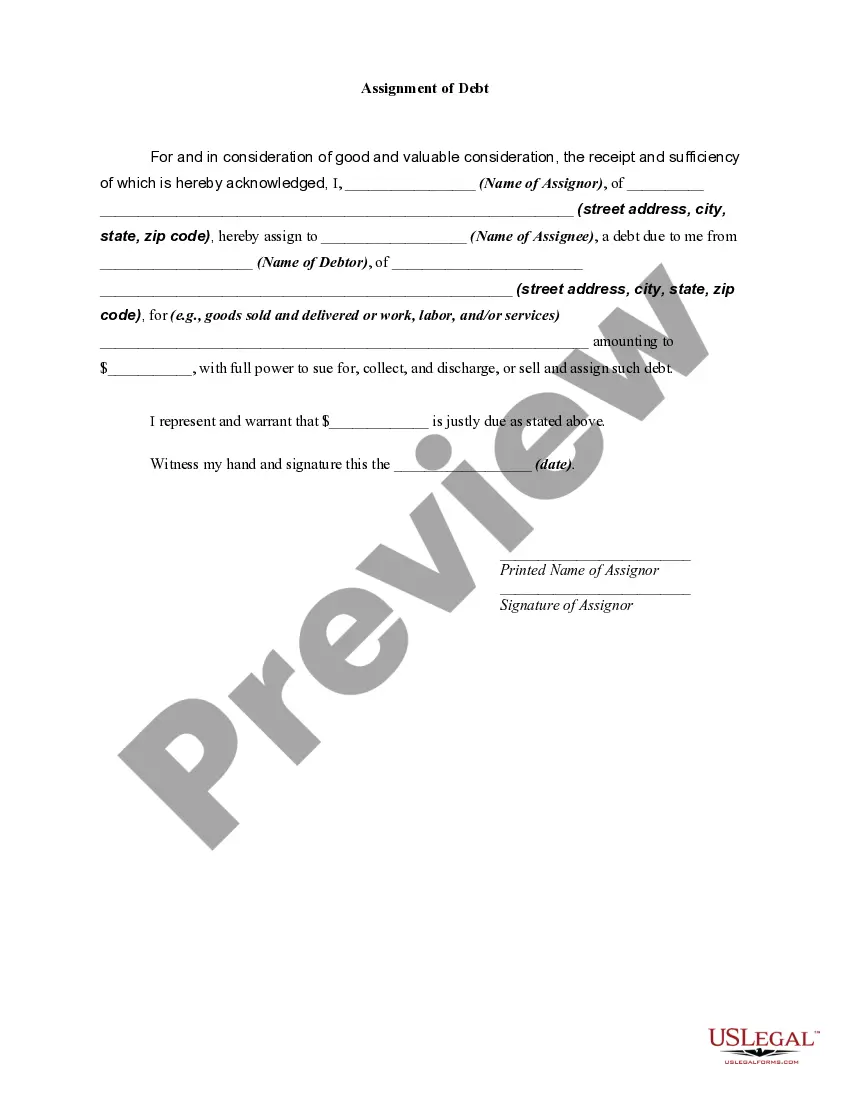

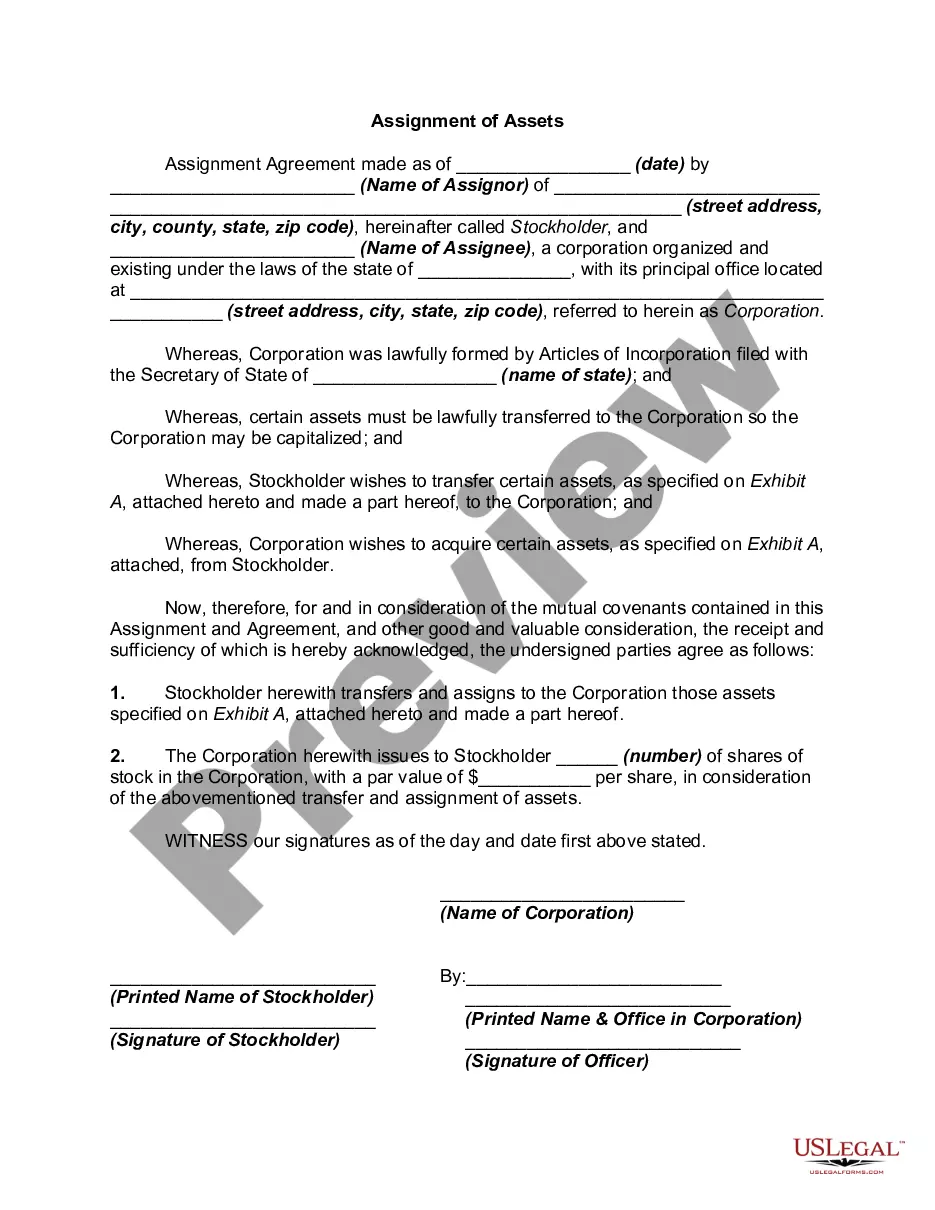

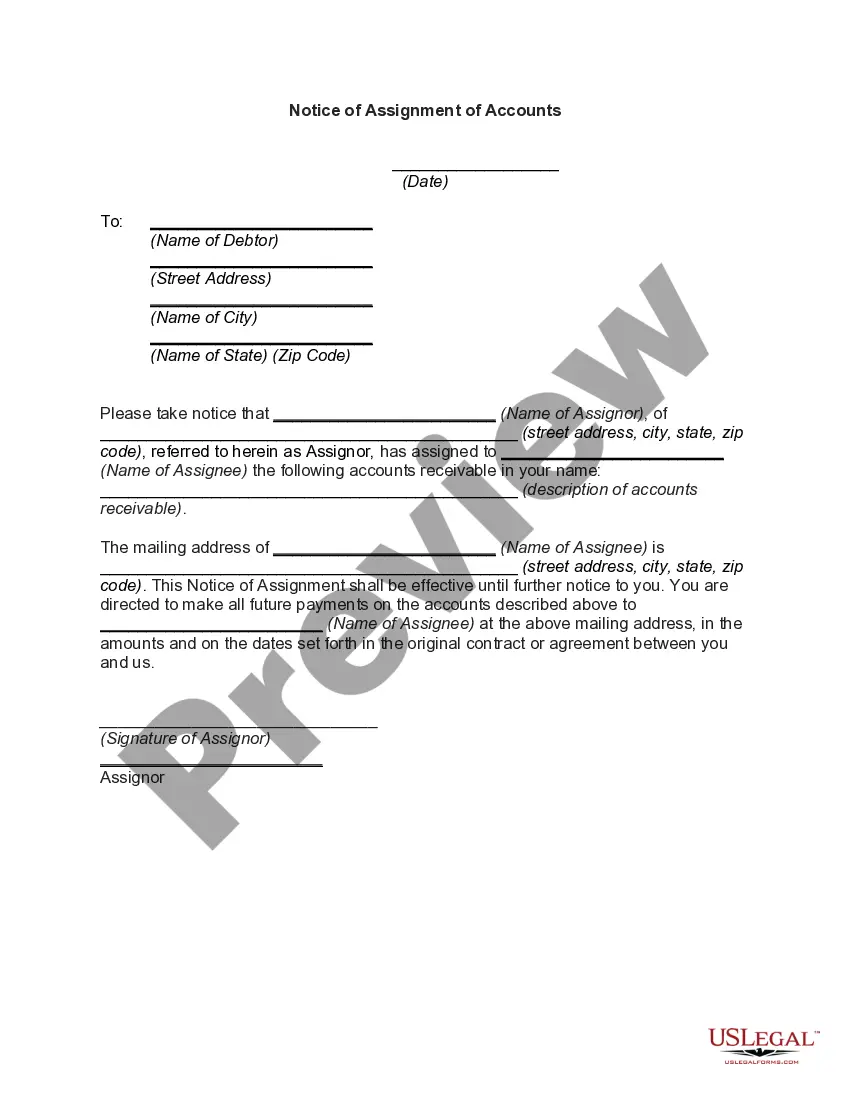

Assignment of Accounts Receivable

What is this form?

The Assignment of Accounts Receivable is a legal document through which an assignor transfers their rights to collect payment on specific outstanding accounts due from customers to an assignee. This form clarifies the rights and obligations related to the assigned accounts, detailing the various terms of the assignment. It is essential for businesses looking to improve cash flow by transferring receivables for immediate payment, differentiating from other financial instruments by its focus on outstanding customer accounts rather than physical assets or broad loan agreements.

Form components explained

- Statement of Assignment: Specifies the assignment of all rights to the accounts receivable.

- Schedule of Accounts Assigned: Lists the specific accounts being assigned, including details such as debtor name, invoice number, and amount due.

- Warranties and Representations: Assignor confirms the validity and collectability of the accounts, along with other assurances regarding the nature of the assigned accounts.

- Payment Terms: Outlines the payment expectations from customers regarding the assigned accounts.

- Solvency Statement: Assures that both the assignor and the debtors are solvent and free from liens that could affect the assignment.

Common use cases

This form is used when a business owner wishes to sell or assign their accounts receivable to another party, typically for immediate cash flow. It is particularly useful in situations where the owner needs quick access to funds without waiting for customers to pay their invoices. Additionally, businesses may use this form during financial restructuring, or when they need to reduce their accounts receivable workload by delegating collection efforts to another entity.

Who can use this document

This form is intended for:

- Business owners seeking to improve cash flow by selling their receivables.

- Accounts receivable management firms looking to acquire debts for collection.

- Financial institutions that require formal documentation when financing against receivables.

- Any entity managing commercial transactions involving the assignment of debts.

Steps to complete this form

- Identify the parties involved: Fill in the name and address of both the assignor and the assignee.

- Specify the date of the assignment: Write the date on which the assignment is made.

- List the assigned accounts: Complete the schedule with relevant details for each account, including names of debtors, invoice numbers, and amounts.

- Sign the document: Ensure the assignor signs the form to validate the assignment.

- Attach supporting documents: Include any relevant financial statements or invoices if required.

Notarization requirements for this form

This form usually doesn’t need to be notarized. However, local laws or specific transactions may require it. Our online notarization service, powered by Notarize, lets you complete it remotely through a secure video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Not listing all accounts accurately, leading to confusion over which debts are included.

- Failing to sign the document, which invalidates the assignment.

- Omitting necessary supporting documents that prove the validity of the accounts.

- Not reviewing state-specific laws that may affect the enforceability of the assignment.

Why complete this form online

- Convenience: Easily download and fill out the form from any location.

- Editability: Modify the form as needed to fit your specific circumstances and accounts.

- Reliability: Forms are drafted by licensed attorneys ensuring compliance with legal standards.

- Accessibility: Immediate access to your completed documents for efficient account management.

Looking for another form?

Form popularity

FAQ

Sign a Contract and Check Credit. Managing accounts receivable begins before the first invoice goes out the door. Track Accounts Receivable. A key part of this process is to effectively track accounts receivable. Make Payment Easy. Do Your Part. Re-Think Your Billing Approach.

The purpose of assigning accounts receivable is to provide collateral in order to obtain a loan. To illustrate, let's assume that a corporation receives a special order from a new customer whose credit rating is superb.

At the point of delivering the goods or services, the company debits Accounts Receivable and credits Sales Revenues or Service Revenues. When an account receivable is collected 30 days later, the asset account Accounts Receivable is reduced and the asset account Cash is increased.

The simplest definition of accounts receivable is money owed to an entity by its customers. Correspondingly, the amount not yet received is credit and, of course, the amount still owed past the due date is collections.

Account receivable is the amount which the company owes from the customer for selling its goods or services and the journal entry to record such credit sales of goods and services is passed by debiting the accounts receivable account with the corresponding credit to the Sales account.

Assignment of accounts receivable is a lending agreement whereby the borrower assigns accounts receivable to the lending institution.The borrower pays interest and a service charge on the loan and the assigned receivables serve as collateral.

It is not uncommon that companies with cash flow problems or those that have a desire to be paid on expedited terms assign their accounts receivables as collateral for a secured loan or they factor them.In the case of factoring, the contractor sells its accounts receivable to the financial institution or the factor.

The purpose of assigning accounts receivable is to provide collateral in order to obtain a loan. To illustrate, let's assume that a corporation receives a special order from a new customer whose credit rating is superb.