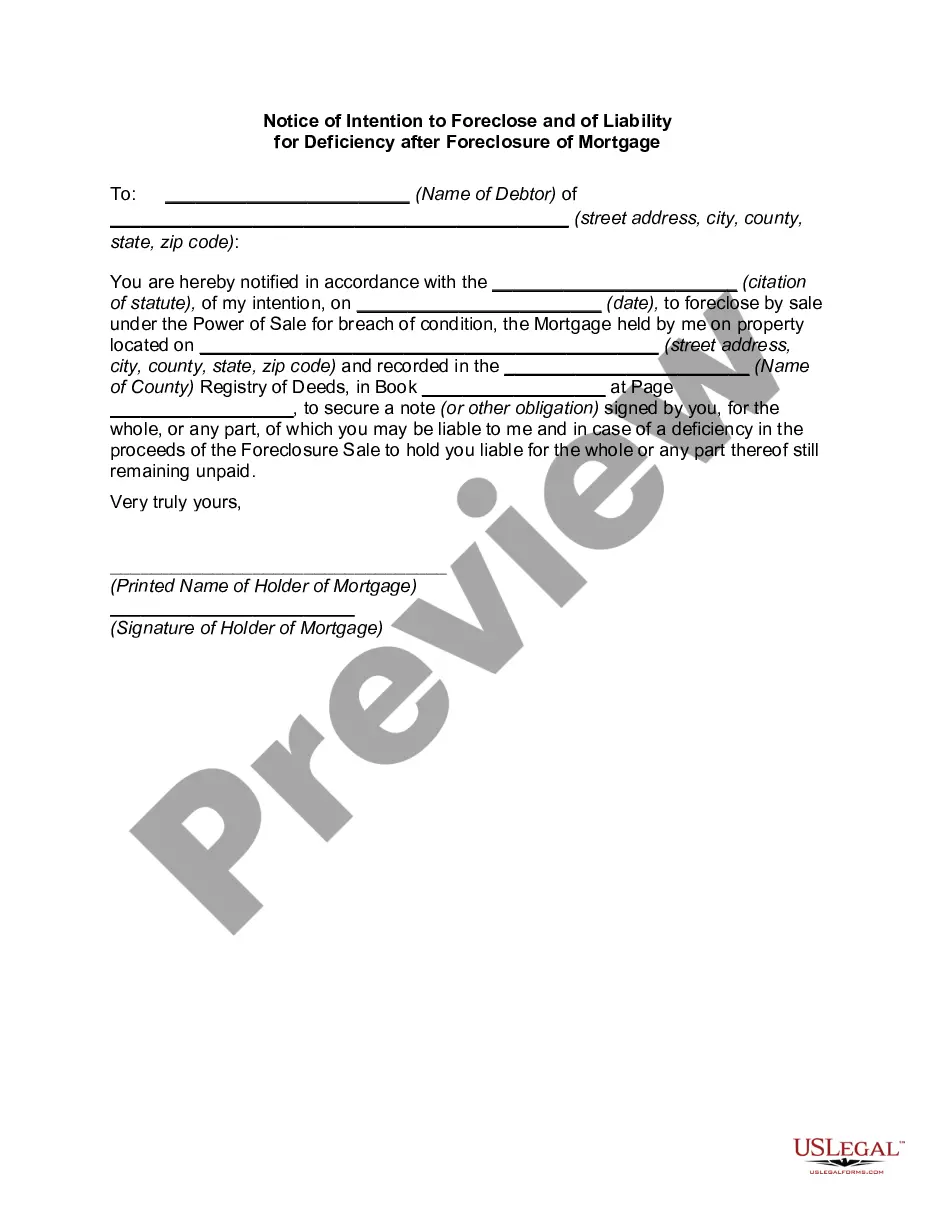

Notice and Demand to Mortgagor regarding Intent to Foreclose

What this document covers

The Notice and Demand to Mortgagor regarding Intent to Foreclose is a legal document that informs a borrower (mortgagor) of a lender's (mortgagee's) intention to initiate foreclosure proceedings on a property due to missed payments. This form is crucial in states that require such notices to ensure proper communication between the lender and borrower, allowing homeowners the opportunity to address past due amounts and explore alternatives to foreclosure. It differs from other foreclosure documents in that it specifically details payment obligations and options available to the borrower before legal action is taken.

Key parts of this document

- Name and address of the mortgagor.

- Details of the mortgage including parties involved and date of execution.

- Description of the property subject to foreclosure.

- Statement of the total amount due and the deadline for payment.

- Contact information for the mortgagee and available resources for counseling.

When to use this form

This form should be used when a lender needs to formally notify a borrower that they are in default on their mortgage and that foreclosure actions may be initiated if the overdue amounts are not paid. It is particularly relevant in situations where state laws mandate prior notice before foreclosure proceedings are initiated. This helps ensure that borrowers are informed and have the opportunity to rectify their default status.

Who this form is for

- Lenders or mortgage companies seeking to comply with state foreclosure notice requirements.

- Real estate attorneys representing lenders in foreclosure actions.

- Homeowners at risk of foreclosure who need to understand communication from their lenders.

Completing this form step by step

- Identify the mortgagor by entering their name and address.

- Provide the details of the mortgage, including the name of the mortgagee and the date of the mortgage.

- Clearly describe the property that is subject to foreclosure.

- Specify the total amount due for redemption and the deadline for payment.

- Include contact information for the mortgagee and organizations that can assist the borrower.

- Sign and date the notice to validate its authenticity.

Is notarization required?

Notarization is required for this form to take effect. Our online notarization service, powered by Notarize, lets you verify and sign documents remotely through an encrypted video session, available 24/7.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include accurate property details.

- Not specifying the correct amount due, including all interest and fees.

- Omitting the required contact information for assistance services.

- Not adhering to state-specific notice periods or requirements.

Advantages of online completion

- Convenience of downloading and filling out from any location.

- Editability allows customization to fit specific details of the foreclosure case.

- Access to templates prepared by licensed attorneys, ensuring compliance with legal standards.

- Immediate availability of the form saves time compared to traditional methods of obtaining legal documents.

Legal use & context

This form serves as a formal notification to the borrower, providing a clear record of the lender's intent to foreclose. Its use helps protect both parties by facilitating communication and providing the borrower with an opportunity to address the default before legal action is taken.

What to keep in mind

- The Notice and Demand to Mortgagor regarding Intent to Foreclose is essential for compliance with state requirements.

- Proper completion is necessary to ensure legal validity and effectiveness.

- Utilizing this form can provide borrowers with options for addressing their mortgage defaults.

Looking for another form?

Form popularity

FAQ

Phase 1: Payment Default. Phase 2: Notice of Default. Phase 3: Notice of Trustee's Sale. Phase 4: Trustee's Sale. Phase 5: Real Estate Owned (REO) Phase 6: Eviction. The Bottom Line.

The California foreclosure process can last up to 200 days or longer. Day 1 is when a payment is missed; your loan is officially in default around day 90. After 180 days, you'll receive a notice of trustee sale. About 20 days later, your bank can then set the auction.

When you take out a mortgage, or any other kind of loan, the law requires you to sign a document that signifies your agreement to repay the money. The promissory note represents a binding legal document, enforceable in a court of law.If the note is lost, then the owner of the loan might have a problem.

Lenders will seize the home, which is typically used as collateral for the loan and will put the property up for sale to try and recoup losses. The foreclosure process from beginning to end typically takes a lender about 18 months to foreclose on a property during normal times.

Borrowers may not avoid foreclosure on their property, for example, simply on the basis of a lost promissory note. The lender has a right to "re-establish" the note legally as long as it has not sold or transferred the note to another party.

An intent to foreclose is a notice you receive from your lender advising you that if you do not bring your mortgage current, the lender will file a foreclosure notice against your home.

Foreclosure is what happens when a homeowner fails to pay the mortgage.If the owner can't pay off the outstanding debt, or sell the property via short sale, the property then goes to a foreclosure auction. If the property doesn't sell there, the lending institution takes possession of it.

You can stop the foreclosure process by informing your lender that you will pay off the default amount and extra fees. Your lender would prefer to have the money much more than they would have your home, so unless there are extenuating circumstances, this should work.

The borrower defaults on the loan. The lender issues a notice of default (NOD). A notice of trustee's sale is recorded in the county office. The lender tries to sell the property at a public auction.