Qualified Income Miller Trust

The Qualified Income Miller Trust is a specialized legal document designed to help individuals who exceed Medicaid income limits qualify for essential healthcare services. Unlike standard trusts, this trust specifically meets the criteria outlined in federal law and allows individuals to allocate their income to the trust for eligibility purposes. The term "Miller Trust" is commonly used, but it is also known as an Income Cap Trust or Income Assignment Trust, highlighting its unique function in Medicaid planning.

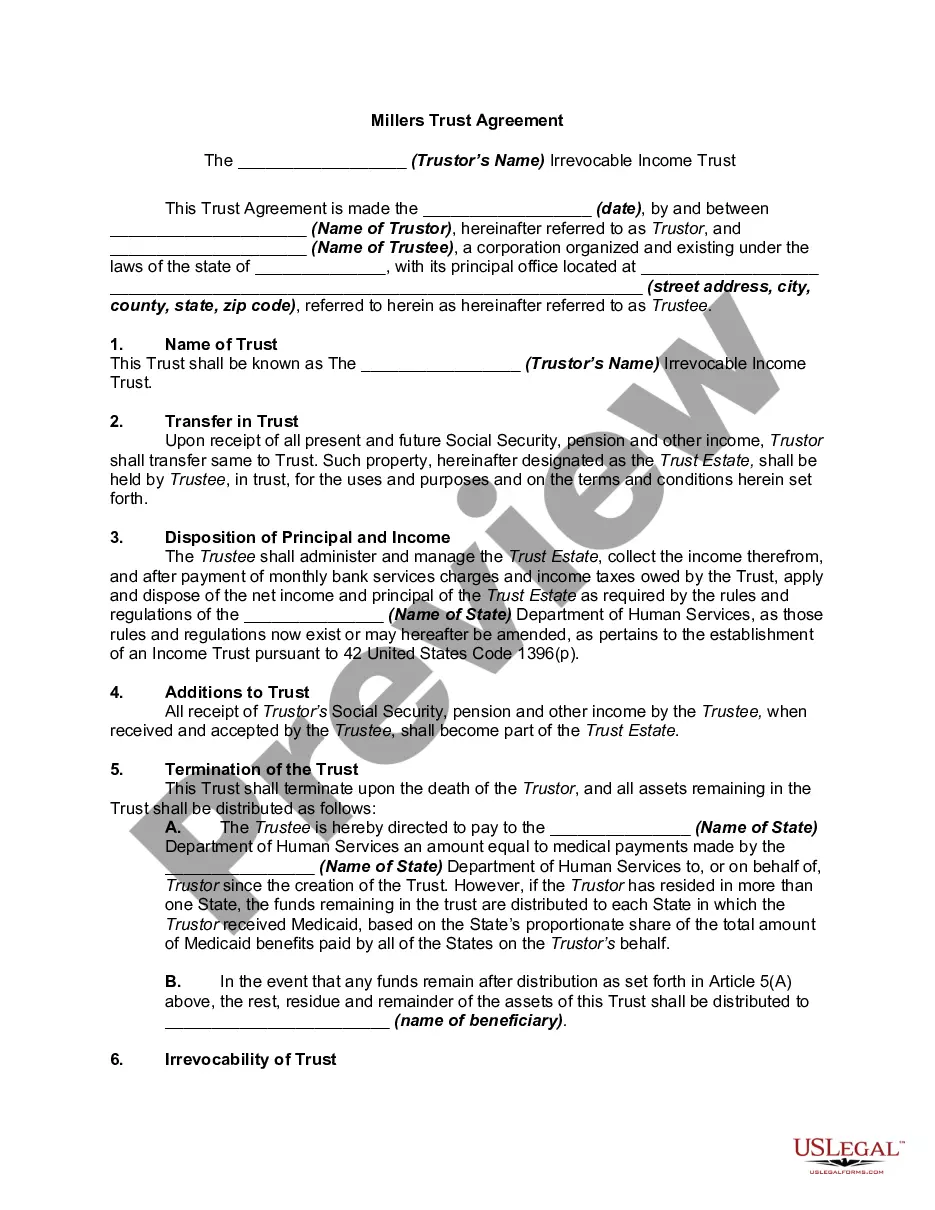

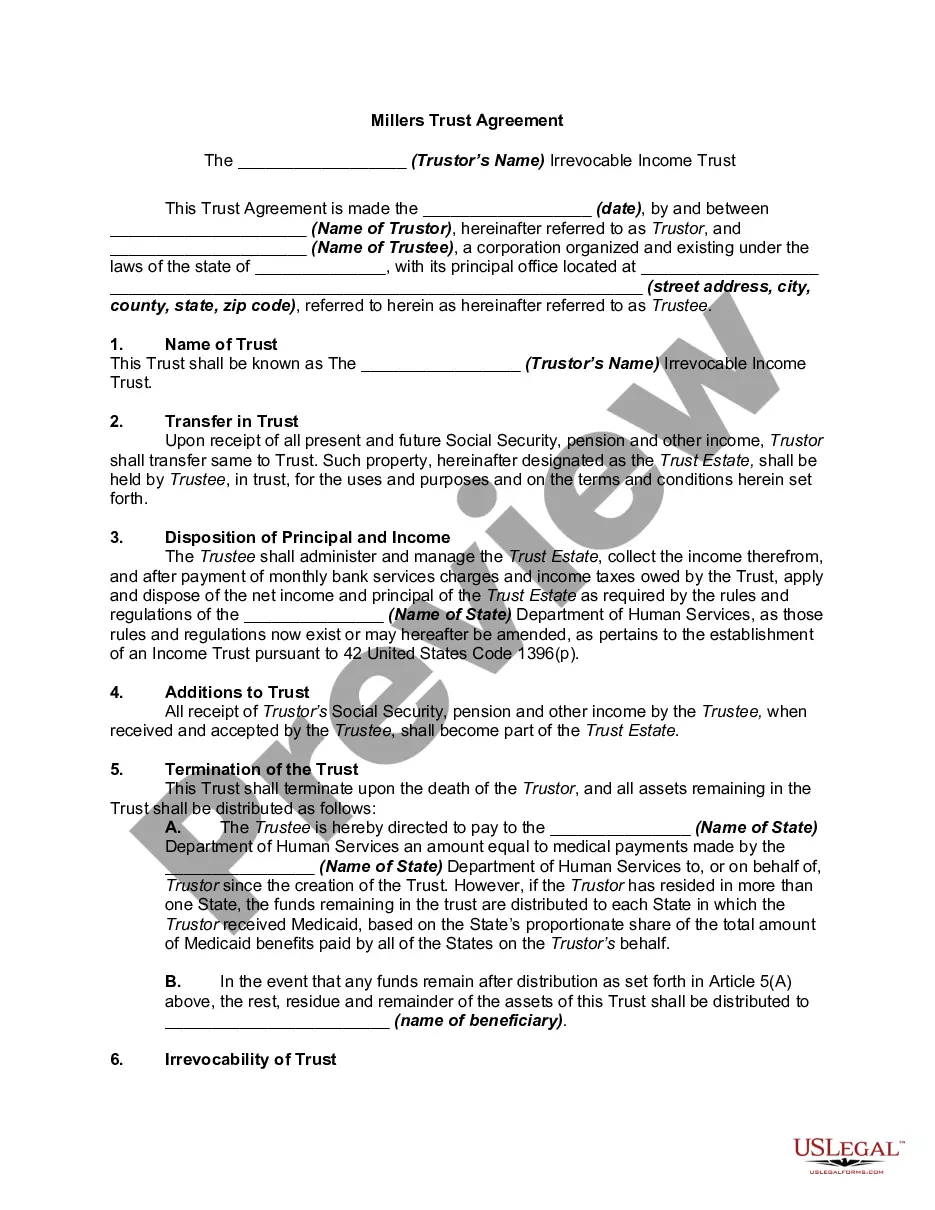

- Name of Trust: Identifies the trust created by the Trustor.

- Transfer in Trust: Details the income types to be transferred into the trust.

- Disposition of Principal and Income: Outlines how assets will be managed and distributed according to state Medicaid rules.

- Termination of the Trust: Specifies conditions under which the trust concludes and how assets are distributed afterward.

- Irrevocability of Trust: States that the trust cannot be revoked, ensuring it serves its intended purpose.

- Powers of Trustee: Defines the management rights of the trustee over the trust assets.

This form is necessary when an individual requires Medicaid assistance but has income above the allowable limits. By establishing a Qualified Income Miller Trust, they can legally divert excess income into the trust, thereby qualifying for Medicaid benefits while ensuring their personal income needs are managed appropriately.

Eligibility for this Form:

- Individuals seeking to qualify for Medicaid services despite having a higher income.

- Families planning for long-term care costs for an elderly relative.

- Trustors who need to manage income for someone who is disabled or requires nursing home care.

Steps to Complete this Form:

- Identify the Trustor and Trustee, entering their full names and addresses.

- Specify the name of the trust according to the Trustor's preference.

- Detail the income types that will be transferred to the trust, ensuring all relevant sources are included.

- Outline how the trust's principal and income will be managed and distributed after the Trustor's death.

- Indicate if there are any additional provisions required by state law, especially regarding Medicaid repayment.

This form does not typically require notarization unless specified by local law. However, it is advisable to verify any state-specific requirements that may necessitate notarization for added legal validity.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

- Failing to identify all sources of income to be transferred to the trust.

- Not understanding state-specific requirements that affect trust operation.

- Neglecting to consult with a financial advisor or attorney regarding the trust's implications.

- Convenient online access to the trust form, facilitating quicker preparation.

- Editability allows for personalized details tailored to specific circumstances.

- Reliability of documents drafted by licensed attorneys, ensuring legal compliance.

Quick recap

- The Qualified Income Miller Trust aids those with excess income to qualify for Medicaid services.

- Careful completion and compliance with state regulations is crucial for legal validity.

- Using this trust can protect assets while enabling access to essential medical care.

Looking for another form?

Form popularity

FAQ

Once a Qualified Income Trust (QIT) has been prepared and signed, the Trustee must establish and maintain a separate bank account in the name of the QIT. The account can be established at any banking institution. Prior to going the bank to open the account, it is a good idea to call your bank and make an appointment.

Therefore, as an irrevocable trust, the QIT is required to have a separate Federal Employer or Tax Identification Number (EIN). The Trustee will use the EIN to open a trust bank account and to file any fiduciary income tax return required to be filed for the QIT.

Some Medicaid professionals include the cost of establishing this type of trust as a package deal with other Medicaid planning services. However, on average, solely setting up a QIT runs approximately $400 to $500, but may run as high as $1,000 or $2,000.

The Miller trust can pay the Medicaid recipient a small personal needs allowance, and the trust can also be used to pay the recipient's spouse a monthly allowance.If there is any money left in the trust when the recipient dies, Medicaid has a right to the money to recover the cost of care.

What Is A Qualified Income Trust (QIT)? If an individual's income is over the limit to qualify for Medicaid long-term care services (including nursing home care), a Qualified Income Trust (QIT) allows an individual to become eligible by placing income into an account each month that the individual needs Medicaid.

A qualified trust is a stock bonus, pension, or profit-sharing plan established by an employer for their employees. A qualified trust is tax-advantaged as long as it meets IRS requirements.

Payments. Miller trusts can be used to pay for a small monthly allowance, Medicare premiums and medical expenses that are not covered by Medicaid or Medicare. In any event, the Miller trust can only be used to pay for the applicant's allowable expenses.