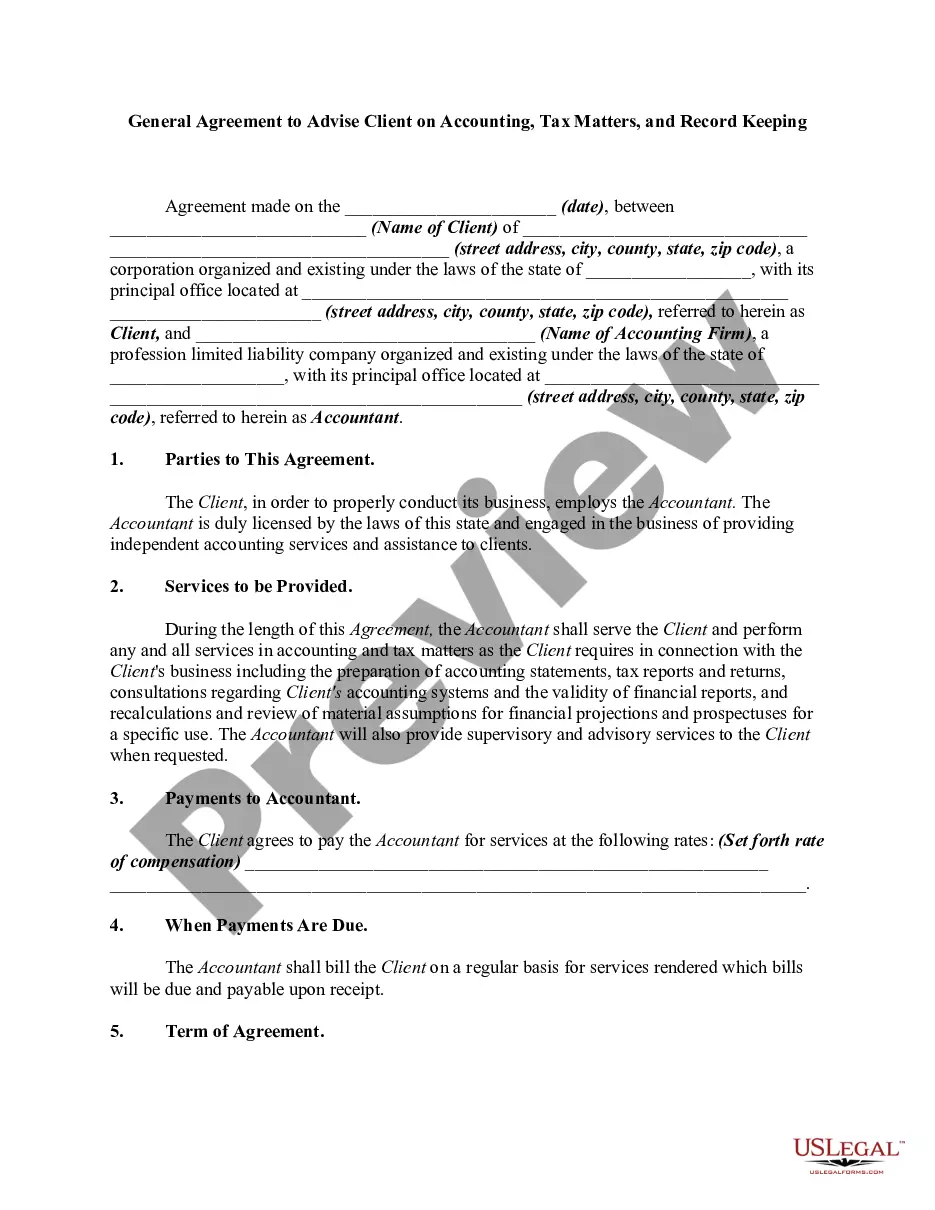

General Consultant Agreement to Advise Client on Accounting, Tax Matters, and Record Keeping

What is this form?

The General Consultant Agreement to Advise Client on Accounting, Tax Matters, and Record Keeping is a legal document that outlines the terms between a client and an accounting firm. This form ensures clarity of services to be rendered, fees, and responsibilities. It provides a written record to prevent misunderstandings, especially as accounting services can be complex and technical in nature. While not strictly required, having this agreement in writing promotes professionalism and accountability in the consulting relationship.

Main sections of this form

- Identification of parties: Names and addresses of the Client and the Accountant.

- Services to be provided: Details about the specific accounting and tax services to be offered.

- Payment terms: The compensation structure and when payments are due.

- Agreement term: Start and end dates for the consulting arrangement.

- Termination clause: Conditions under which either party can terminate the agreement.

- Governing law: Specification of the state law that governs the agreement.

When to use this document

This General Consultant Agreement is essential for situations where a client engages an accountant for specialized services, such as tax preparation, financial reporting, or record-keeping. It is particularly useful when the scope of work is extensive or when there is potential for complex interactions between the client and the accountant, thus ensuring all expectations and obligations are documented and agreed upon upfront.

Who this form is for

This form is suitable for:

- Businesses seeking professional accounting assistance.

- Accountants or accounting firms providing consulting services.

- Any client requiring clear terms regarding accounting and tax-related services.

How to prepare this document

- Identify the parties by entering the Client's and Accountant's names and addresses.

- List the specific services to be provided by the Accountant.

- Specify the payment rates and terms for the services rendered.

- Enter the start and end dates for the duration of the agreement.

- Sign and date the document to finalize the agreement.

Does this document require notarization?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to clearly define the scope of services, leading to potential disputes.

- Not including payment terms, which can create confusion over compensation.

- Neglecting to specify the governing law, which is crucial for legal enforceability.

- Forgetting to document the termination process, risking misunderstandings if the relationship changes.

Why complete this form online

- Convenient access: Download and complete your agreement from anywhere.

- Editability: Easily make changes to suit your specific needs.

- Reliability: Templates are drafted by licensed attorneys, ensuring legal compliance.

Main things to remember

- A General Consultant Agreement formalizes the relationship between the client and accountant.

- It clarifies the services to be provided and the payment structure.

- This form can help prevent misunderstandings and disputes.

Glossary of terms

- Independent contractor: A person or business that provides services to another entity under terms specified in a contract.

- Term of agreement: The period during which the contract is active and enforceable.

- Mandatory arbitration: A requirement that disputes be resolved outside of court in a structured arbitration process.

Looking for another form?

Form popularity

FAQ

Specifically, the provision of bookkeeping services, valuation reports, internal audit outsourcing, actuarial services and financial information design and implementation will not impair independence provided it is reasonable to conclude that the results of the service will not be subject to audit procedures during an

As a general rule, auditor-provided tax services don't raise independence issues, so long as the company's audit committee approves the arrangement.Also, the Public Company Accounting Oversight Board (PCAOB) prohibits auditors from providing tax services under certain circumstances.

Audits typically are performed by an independent, certified accounting firm. There was a time CPA firms were associated strictly with financial maneuvers, but these firms today offer an array of consulting services to their clients.

UNDER THE SEC RULES, CPAs WILL BE ALLOWED TO provide tax-minimization services to audit clients, except for transactions that have no business purpose other than tax avoidance.They also are excluded from the rules that say compensating partners for procuring nonaudit services for the firm impairs their independence.

Bookkeeping. Financial information systems design and implementation. Appraisal or valuation services, fairness opinions, or contribution-in-kind reports. Actuarial services.

The auditing firm analyzes current and prior financial statements to determine not only if finances are in order, but also if the proper reports are being generated. Auditors review cash management procedures, accounting policies and controls, trial balance accounts and relationships with creditors.

Bookkeeping services are permitted, as long as the individuals performing these services are not the same individuals performing the audit.An accountant generally cannot provide bookkeeping services to an SEC audit client.

Non-audit services are any professional services provided by a qualified public accountant during the period of an audit engagement which are not connected to an audit or review of an institution's financial statements.

The SEC rules on audit independence are often organized into five key areas: (A) Prohibited Non-Audit Services; (B) Audit Committee Pre-Approval of Services; (C) Partner Rotation; (D) Conflict of Interest; and (E) Increased Communication and Disclosure.