Letter to Credit Bureau Requesting the Removal of Inaccurate Information

What is this form?

This Letter to Credit Bureau Requesting the Removal of Inaccurate Information is a formal communication designed to dispute incorrect items on your credit report. Its primary purpose is to notify the credit bureau of inaccuracies that could harm your credit standing, prompting them to investigate and correct the information. This letter is crucial for individuals seeking to maintain or restore their good credit by ensuring the accuracy of their credit history.

What’s included in this form

- Sender's full name and address

- Date of the letter

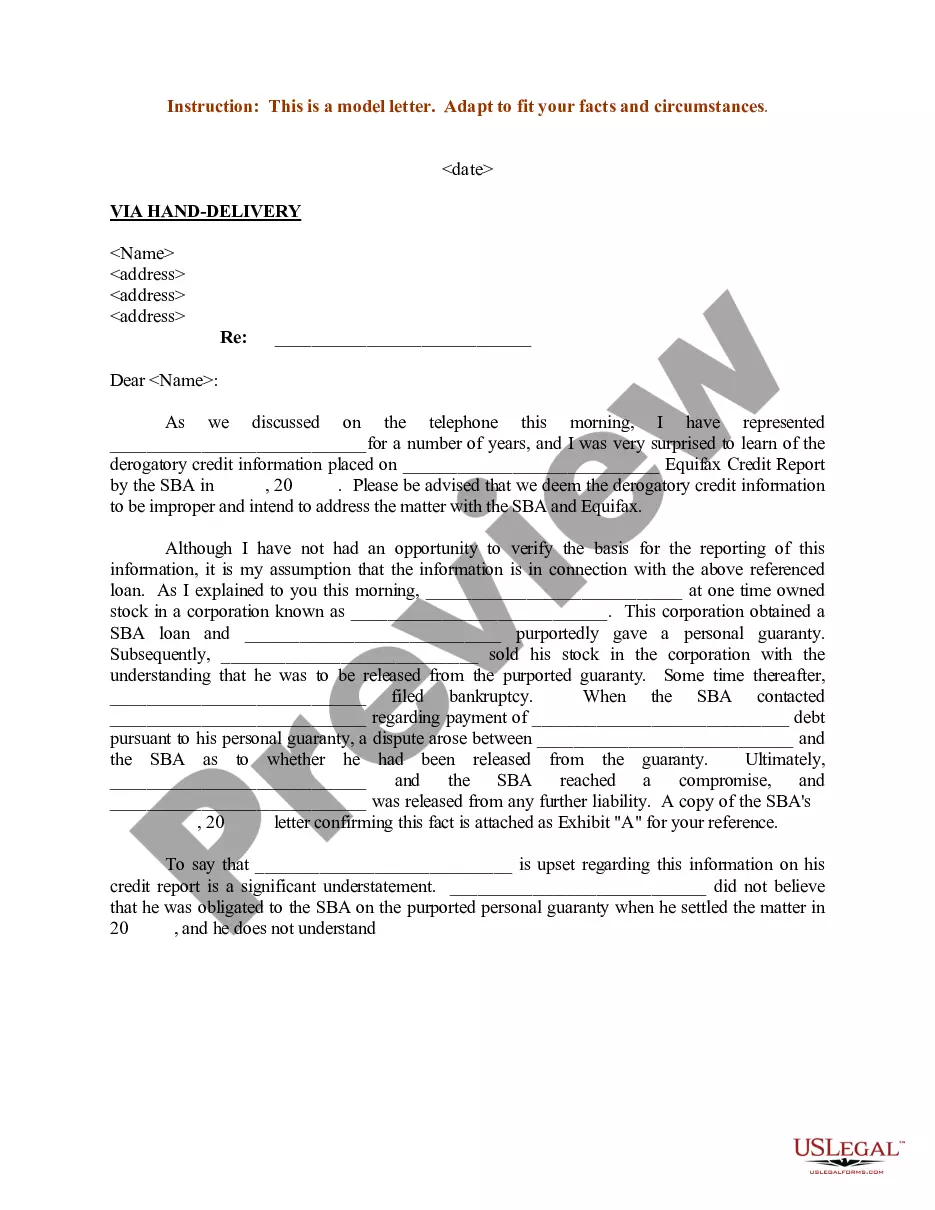

- Name of the credit bureau and contact person

- Specific request for reinvestigation

- Details of the inaccuracies being disputed

- Enclosures such as proof of accuracy (e.g., bank statements)

Situations where this form applies

This form should be used when you identify incorrect information on your credit report that could negatively impact your credit score. You may need to use this letter if you have been denied credit or if you notice discrepancies in your credit history, such as late payments that you believe are inaccurate. It's essential to act promptly to ensure your credit report accurately reflects your financial behavior.

Who should use this form

- Individuals who have errors on their credit report

- Consumers seeking to dispute incorrect items affecting their credit score

- People who have been denied credit due to inaccuracies in their credit history

Instructions for completing this form

- Begin by entering your full name and address at the top of the letter.

- Input the date you are sending the letter.

- Include the name of the credit bureau and the specific contact person if available.

- Clearly outline the inaccuracies you are disputing, providing details of your accounts.

- Attach supporting documentation that verifies your claims, such as bank statements or payment confirmations.

- Sign the letter to authenticate your request before sending it out.

Notarization requirements for this form

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to include sufficient evidence to support your claim.

- Omitting key personal information such as your address or account numbers.

- Not specifying the nature of the inaccuracies clearly and precisely.

- Sending the letter without a signature, which is essential for authenticity.

Benefits of completing this form online

- Convenient access to legal documents at any time without the need for an attorney appointment.

- Editable templates allow you to customize the letter to your specific situation easily.

- Secure downloads ensure your personal information is protected while preparing your forms.

Quick recap

- Accurate credit reporting is essential for your financial health.

- Promptly disputing inaccuracies can alleviate potential harm to your credit score.

- Using a structured letter can help ensure that your dispute is taken seriously by credit bureaus.

Looking for another form?

Form popularity

FAQ

This form is a formal letter used to dispute inaccurate items on your credit report by notifying the credit bureau to reinvestigate and correct the information. It helps you seek to maintain or restore good credit by ensuring your credit history reflects accurate information. The form prompts you to include essential identifying details and supporting documentation.

To write this letter, provide the sender’s full name and address, the date, and the credit bureau’s name and contact person. State a specific reinvestigation request for the disputed item, and clearly describe the inaccuracies. Include supporting enclosures, such as documents proving the item is incorrect, and keep copies for your records. Send the completed letter to the correct bureau.

This form provides a structured way to dispute inaccuracies by submitting a reinvestigation request to the credit bureau. It requires the sender’s information, the bureau contact, a clear description of the inaccuracies, and any enclosures that support the dispute. Using this form helps prompt the bureau to review the items and correct them if warranted.

Enclosures should include documents supporting your claim, such as proof of accuracy (for example, bank statements or correspondence). These enclosures assist the reinvestigation by verifying the inaccuracies you list and providing concrete evidence. Make sure each enclosure is relevant to the item being disputed and keep copies for your records.

This form is intended for individuals who find errors on their credit report, consumers disputing items affecting their credit score, and those who have been denied credit due to inaccuracies. It guides these readers through submitting a reinvestigation request with supporting details to prompt correction.

This form is a standard credit bureau dispute letter that explicitly collects and states a reinvestigation request, including the sender’s information, the bureau contact, a detailed description of inaccuracies, and enclosures. Its structured fields and explicit focus on reinvestigation distinguish it from generic dispute letters.