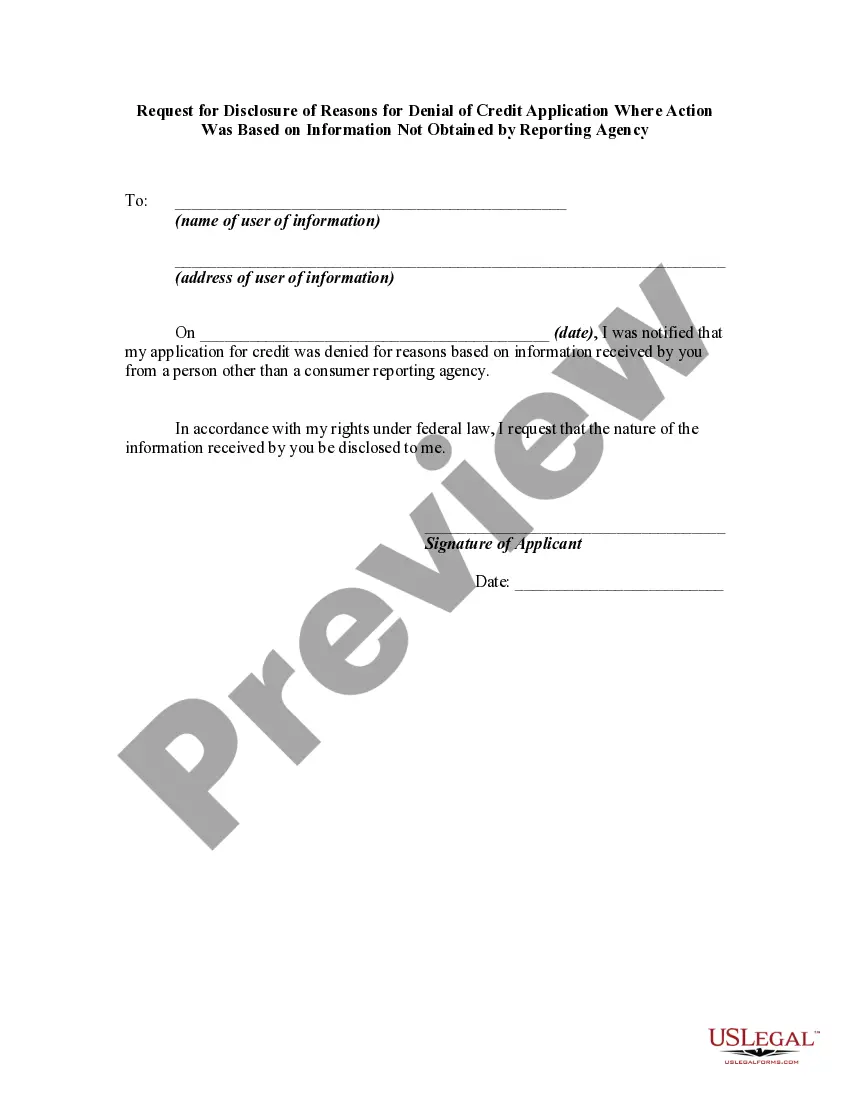

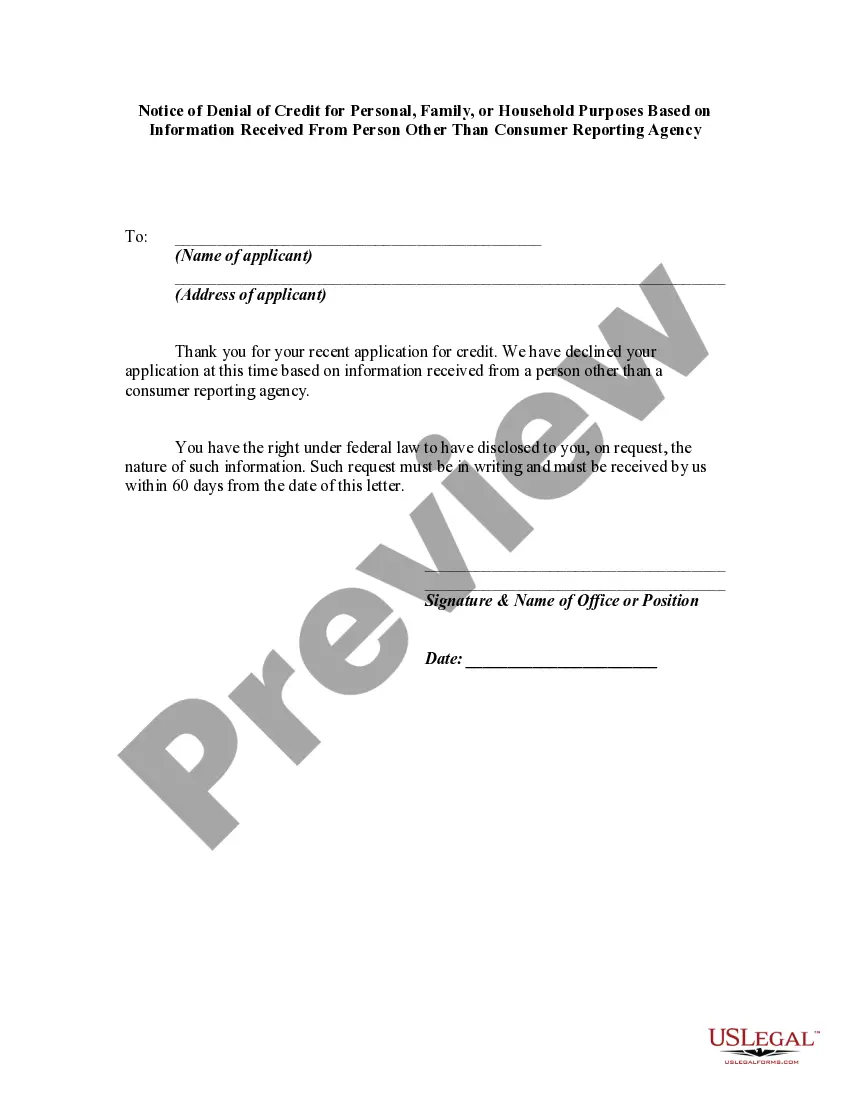

Notice of Denial of Credit, Insurance, or Employment Based on Information Received From Consumer Reporting Agency

Understanding this form

The Notice of Denial of Credit, Insurance, or Employment Based on Information Received From Consumer Reporting Agency is a legal document that informs an applicant when their request for credit, insurance, or employment has been denied due to negative information in their consumer report. Under the federal Equal Credit Opportunity Act, this notice is a crucial requirement that ensures transparency in the decision-making process for creditors, insurers, and employers. It helps applicants understand the reasons for the denial and their rights regarding the information used in the decision.

What’s included in this form

- Name and address of the applicant

- Type of application (credit, insurance, or employment)

- Name of the consumer reporting agency used

- Address of the consumer reporting agency

- Statement of rights regarding consumer report information

- Signature of the official who prepared the notice

- Date of the notice

When this form is needed

This form should be used when a creditor, insurer, or employer declines an application for credit, insurance, or employment based on information obtained from a consumer reporting agency. It is essential to provide this notice to comply with federal regulations, ensuring that the applicant is aware of the denial and has access to the relevant information about their consumer report.

Intended users of this form

- Lenders or financial institutions denying credit applications

- Insurance companies declining coverage applications

- Employers who decide against hiring an applicant based on consumer report findings

- Compliance officers ensuring adherence to the Equal Credit Opportunity Act

How to complete this form

- Fill in the name and address of the applicant.

- Specify the type of application (credit, insurance, or employment) and the position applied for, if applicable.

- Indicate the name and address of the consumer reporting agency that provided the negative information.

- Include a statement informing the applicant of their rights to access their consumer report.

- Sign and date the notice to finalize it.

Does this document require notarization?

Notarization is not commonly needed for this form. However, certain documents or local rules may make it necessary. Our notarization service, powered by Notarize, allows you to finalize it securely online anytime, day or night.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Avoid these common issues

- Failing to include the applicant's full name and correct address.

- Not specifying the type of application denied.

- Leaving out the name or address of the consumer reporting agency.

- Neglecting to inform the applicant of their rights to dispute the report.

- Not signing or dating the form, which can make it invalid.

Why use this form online

- Conveniently fill out and download the form from any location.

- Ensures compliance with federal legal requirements easily.

- Editable fields allow for quick updates if needed.

- Access to customized state-specific language if required.

Legal use & context

- This form serves as a formal notification and is a requirement under federal law.

- Failure to provide this notice may result in legal consequences for the denying party.

- It helps maintain fairness and transparency in lending and hiring practices.

Quick recap

- The notice must be issued for any adverse actions based on a consumer report.

- It is essential for compliance with the Equal Credit Opportunity Act.

- Providing this notice informs the applicant of their rights and the basis for the decision.

Looking for another form?

Form popularity

FAQ

Review your credit reports. Investigate the error(s). Submit your dispute online, by phone or by mail. Wait for results, which usually arrive within two weeks (but up to 45 days). Complain to a regulatory agency, if necessary.

Tell the credit reporting company, in writing, what information you think is inaccurate. Tell the information provider (that is, the person, company, or organization that provides information about you to a credit reporting company), in writing, that you dispute an item in your credit report.

A 609 letter is a method of requesting the removal of negative information (even if it's accurate) from your credit report, thanks to the legal specifications of section 609 of the Fair Credit Reporting Act.

Yes, you might be able to sue a company for false credit reporting. However, before you seek a civil remedy through the courts, you should properly exercise your rights under the law.

If you identify an error on your credit report, you should start by disputing that information with the credit reporting company (Experian, Equifax, and/or Transunion). You should explain in writing what you think is wrong, why, and include copies of documents that support your dispute.

Common violations of the FCRA include: Creditors give reporting agencies inaccurate financial information about you. Reporting agencies mixing up one person's information with another's because of similar (or same) last name or social security number. Agencies fail to follow guidelines for handling disputes.

Highlights: Checking your credit history and credit scores can help you better understand your current credit position. Regularly checking your credit reports can help you be more aware of what lenders may see. Checking your credit reports can also help you detect any inaccurate or incomplete information.

Section 609 refers to a section of the Fair Credit Reporting Act (FCRA) that addresses your rights to request copies of your own credit reports and associated information that appears on your credit reports.And if the disputed information cannot be verified or confirmed, then it must be removed.

There's no evidence to suggest a 609 letter is more or less effective than the usual process of disputing an error on your credit reportit's just another method of doing so. If the dispute is valid, the credit bureaus will remove the negative item.