Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Las Vegas Nevada Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency

Description

Form popularity

FAQ

Consumer reporting agencies must include all key factors that adversely affect a consumer’s credit score in the disclosures provided to the consumer. Typically, there are five primary factors that contribute to a credit score, including payment history, amounts owed, length of credit history, new credit, and types of credit used. By understanding these factors, especially in the case of a Las Vegas Nevada Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency, consumers can better manage their credit profiles. This knowledge equips you to take actionable steps toward improving your credit standing.

When notifying a consumer of an adverse action, vague reasons such as 'insufficient credit history' or 'not meeting our criteria' are typically not acceptable. Creditors must provide specific details that allow consumers to understand why credit was denied. This requirement is especially important in the context of a Las Vegas Nevada Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency, as clarity in communication can aid consumers in rectifying issues affecting their credit. Thus, knowing the specifics can guide your next steps.

Disclosure of use of information from an outside source refers to informing consumers when a creditor uses information obtained from sources other than a consumer reporting agency to make a credit decision. This practice enhances consumer awareness and allows for better understanding of credit evaluations. The Las Vegas Nevada Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency is relevant here, as it highlights how external information impacts credit assessments. Understanding this can help you evaluate the fairness of your credit experience.

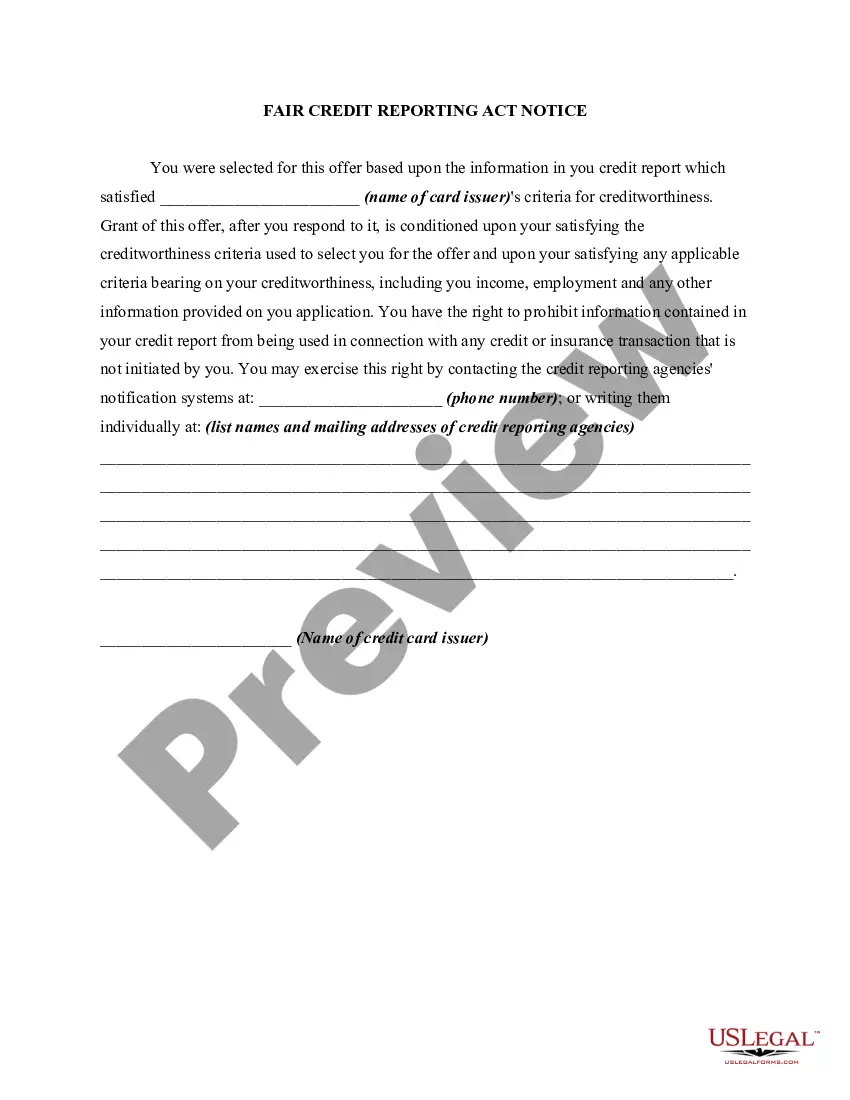

Under the Fair Credit Reporting Act (FCRA), creditors must inform consumers when their credit is denied due to information in a consumer report. This law protects consumers by ensuring transparency in the credit decision-making process. Specifically, it mandates that borrowers receive a notice of the adverse action along with the reasons for the denial. If you experience a Las Vegas Nevada Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency, knowing your rights under the FCRA can empower you to take action.

Banks must ensure that any consumer information they provide to a reporting agency is accurate, complete, and up-to-date. They are also required to notify consumers within a specified timeframe when negative information is reported. Compliance with these requirements safeguards consumer rights and helps maintain the integrity of credit reporting. If you're looking for clarity on these processes, uslegalforms provides valuable insights to ensure compliance and protect your financial information.

The notation 'account information disputed by consumer meets FCRA requirements' indicates that your dispute has been addressed in accordance with the Fair Credit Reporting Act. This means that the credit reporting agency has properly reviewed and processed your dispute. It's essential to keep track of such disputes, as they can impact your credit score. For assistance in understanding your report and managing disputes, platforms like uslegalforms can offer supportive guidance.

An FCRA dispute is a formal statement made by a consumer, contesting inaccuracies on their credit report based on FCRA guidelines. This process allows you to challenge misleading or incorrect information reported by a credit agency. Filing an FCRA dispute is important to protect your financial health and maintain a good credit score. To streamline this process, consider using uslegalforms which provides structured resources for submitting and tracking disputes effectively.

You must notify a consumer when you furnish negative information to a consumer reporting agency within 30 days of reporting that negative information. This requirement ensures transparency and gives consumers the opportunity to address inaccuracies in their credit report. Understanding these obligations is vital, especially if you are a lender or creditor. Should you need assistance with compliance, uslegalforms offers tools to help manage these notifications properly.

The phrase 'consumer meets FCRA requirements' refers to the guidelines stipulated in the Fair Credit Reporting Act that protect consumer rights regarding credit reporting. When your report is marked this way, it indicates that the agency has acknowledged your status and your rights as a consumer. Comprehending these requirements can empower you during disputes and help maintain the integrity of your credit profile. If you face confusion, resources on platforms like uslegalforms are available to guide you.

When Credit Karma indicates that account information disputed by the consumer meets Fair Credit Reporting Act (FCRA) requirements, it means your dispute has been officially recognized. The FCRA obligates credit reporting agencies to address consumer disputes and ensure that the information remains accurate. This designation ensures that your rights are protected as you navigate through potential inaccuracies on your report. Additionally, platforms like uslegalforms can help you understand and exercise your rights effectively.