Wyoming Crummey Trust Agreement for Benefit of Child with Parents as Trustors

Description

How to fill out Crummey Trust Agreement For Benefit Of Child With Parents As Trustors?

If you need to be thorough, download, or print valid document templates, utilize US Legal Forms, the largest selection of legitimate forms available on the web.

Employ the site's straightforward and user-friendly search to find the documents you require.

A range of templates for business and personal purposes are organized by categories and states, or keywords.

Step 4. Once you locate the form you need, click the Buy Now button. Choose your desired pricing plan and enter your information to create an account.

Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the transaction.

- Use US Legal Forms to access the Wyoming Crummey Trust Agreement for the Benefit of Child with Parents as Trustors with just a few clicks.

- If you are currently a client of US Legal Forms, Log In to your account and then click the Download button to obtain the Wyoming Crummey Trust Agreement for the Benefit of Child with Parents as Trustors.

- You can also access forms you've previously saved from the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the steps outlined below.

- Step 1. Ensure you've selected the form for the correct city/state.

- Step 2. Use the Preview option to review the contents of the form. Don't forget to read all the details.

- Step 3. If you are not satisfied with the form, use the Search box at the top of the screen to find other options in the legitimate form category.

Form popularity

FAQ

While the Wyoming Crummey Trust Agreement for Benefit of Child with Parents as Trustors provides significant benefits, it also has potential downsides. One major concern is that the child may withdraw funds in the early years, which can reduce the long-term growth of the trust. Additionally, navigating the tax implications and ongoing management requirements can be complex. It's advisable to consult with professionals, like those at uslegalforms, to ensure that a Crummey Trust aligns with your family’s goals.

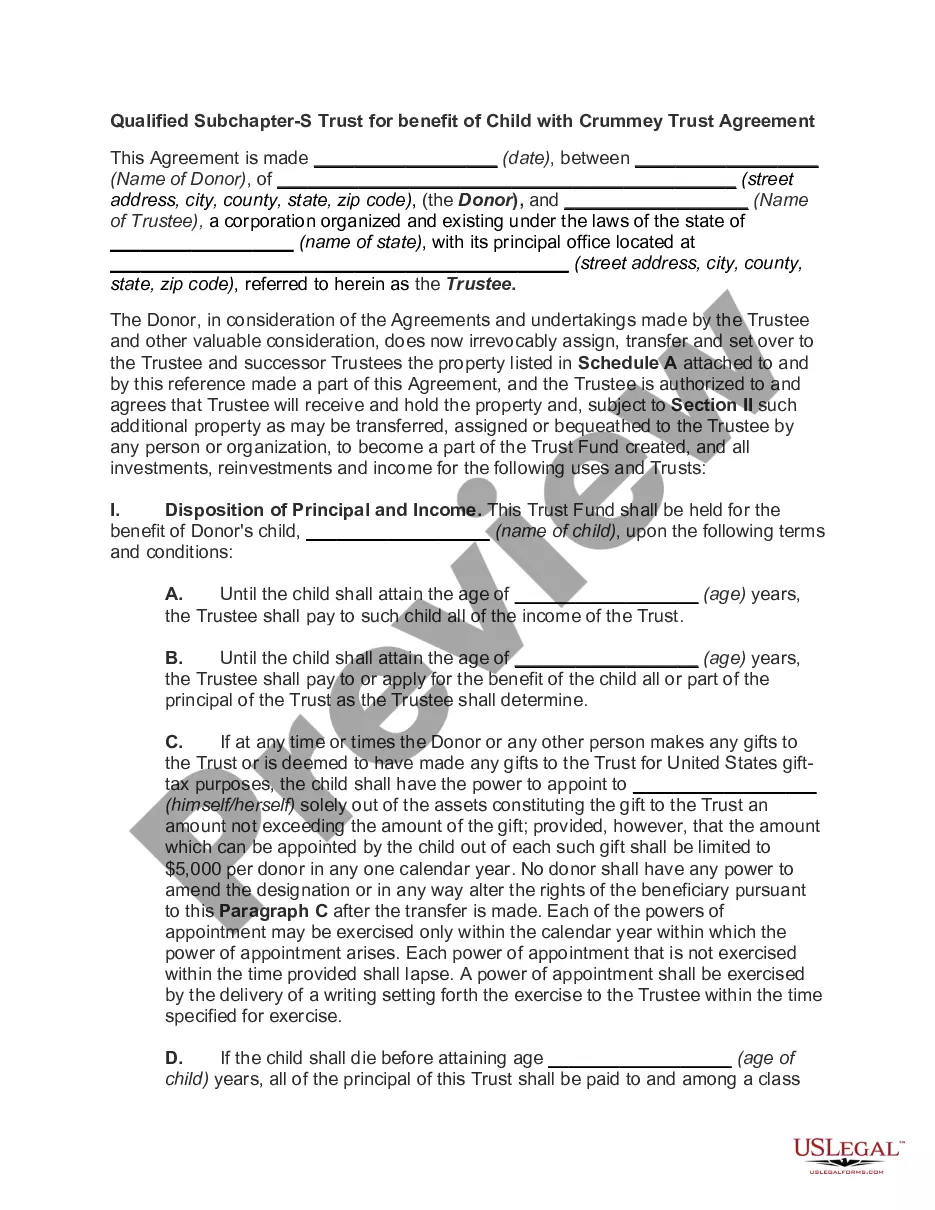

A Wyoming Crummey Trust Agreement for Benefit of Child with Parents as Trustors functions by allowing the grantor to make gifts to the trust, which benefits the child. The child has the right to withdraw contributions for a limited time, which qualifies the gifts for the annual exclusion from gift tax. This strategy effectively reduces the grantor's taxable estate while ensuring that the child receives financial support. The trust also enables asset management according to the grantor's wishes.

A Crummey Trust allows you to take advantage of the gift tax exclusions and simultaneously minimize your estate taxes. You do not have to provide an opportunity for the beneficiary to withdraw the entire balance of the trust until a certain age. A Crummey trust can have multiple beneficiaries.

A Section 2503c trust is a type of minor's trust established for a beneficiary under the age of 21 which allows parents, grandparents, and other donors to make tax-free gifts to the trust up to the annual gift tax exclusion amount and the generation skipping transfer tax exclusion amount.

Crummey trusts are typically used by parents to provide their children with lifetime gifts while sheltering their money from gift taxes as long as the gift's value is equal to or less than the permitted annual exclusion amount.

Crummey power is a technique that enables a person to receive a gift that is not eligible for a gift-tax exclusion and change it into a gift that is, in fact, eligible. Individuals often apply Crummey power to contributions in an irrevocable trust.

So can a trustee also be a beneficiary? The short answer is yes, but the trustee will have to be exceedingly careful to never engage in any actions that would constitute a breach of trust, including placing their personal interests above those of the other beneficiaries.

Under the doctrine of merger, if the sole trustee and the sole beneficiary are occupied by the same person, there is no division of property interests between legal and equitable title. Therefore, this would make the trust legally invalid because the two types of title have merged.

The trustee manages assets of Crummey trusts, and you set terms that determine when distributions should be made. A Crummey Trust is generally more flexible and advantageous than a 529 college savings account. Multiple beneficiaries can be included in the trust, including beneficiaries over 21.

A Hanging Crummey power allows the withdrawal right to lapse only for the amount that IRC § 2514(e) protects from treatment of release, which is the gift amount less the greater of $5,000 or 5% of the value of the property out of which the withdrawal right could have been satisfied.