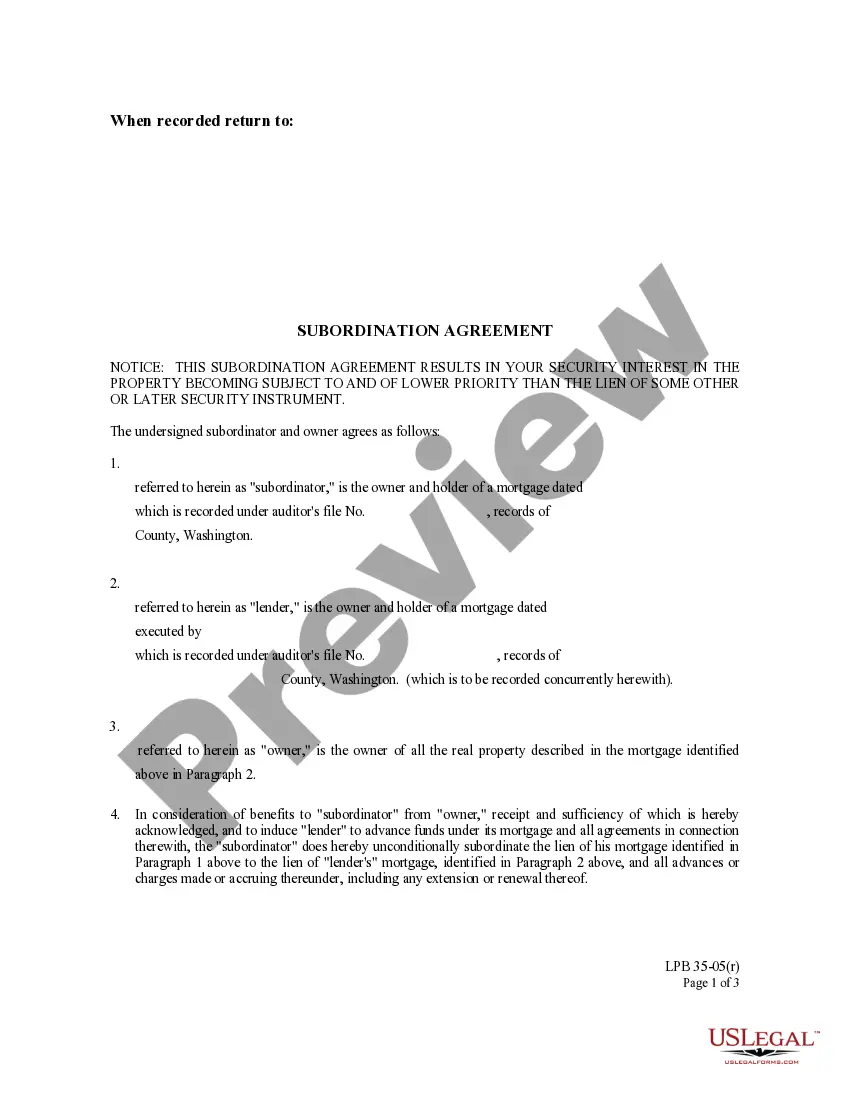

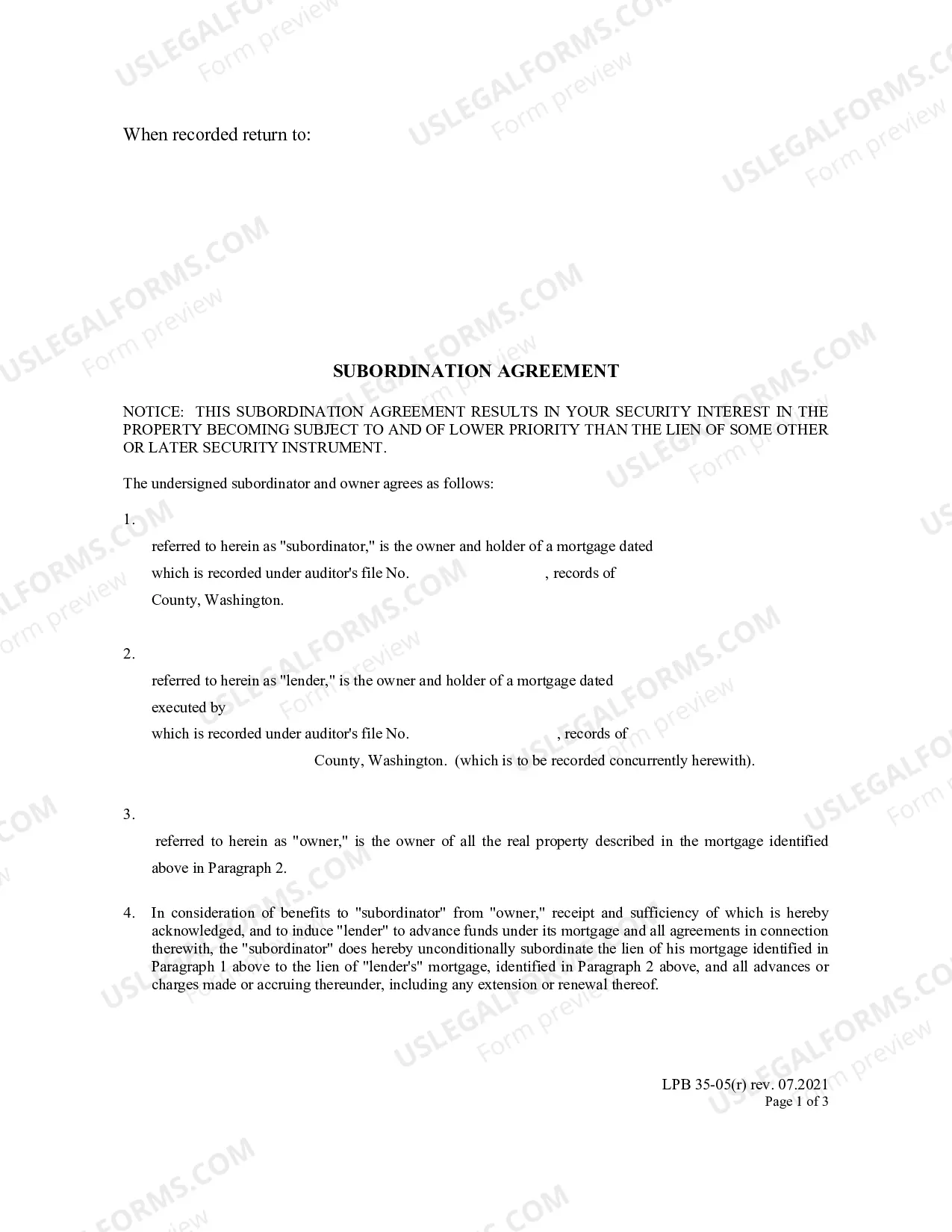

A Washington Subordination Agreement (WSA) is a legal document used in the state of Washington to transfer the rights of a mortgage from one lender to another. It is also known as a subordination agreement or subordination of mortgage. This agreement assigns priority of interest in the existing mortgage to the new lender, meaning that the new lender has priority to receive payments in the event of a foreclosure. It also includes a clause that states that the new lender cannot seek payment from the borrower until the existing mortgage is paid in full. There are three types of Washington Subordination Agreement: 1) Traditional WSA, 2) Short Form WSA, and 3) FHA/VA Subordination Agreement. Traditional WSA is the most comprehensive and complex form, as it is used to transfer mortgages that are not backed by the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA). It includes detailed information about the rights and responsibilities of all parties involved in the transfer of the mortgage. Short Form WSA is a simpler version of the Traditional WSA, and is used for mortgages that are backed by the FHA or VA. It is less comprehensive and includes fewer details about the rights and responsibilities of the parties involved. FHA/VA Subordination Agreement is used specifically for mortgages backed by the FHA or VA, and is the most basic form of Washington Subordination Agreement. It only includes the necessary information to transfer the rights of the mortgage and does not include any additional clauses or details.

Washington Subordination Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Washington Subordination Agreement?

Dealing with legal paperwork requires attention, precision, and using well-drafted templates. US Legal Forms has been helping people countrywide do just that for 25 years, so when you pick your Washington Subordination Agreement template from our library, you can be sure it complies with federal and state laws.

Working with our service is simple and quick. To obtain the necessary paperwork, all you’ll need is an account with a valid subscription. Here’s a quick guide for you to obtain your Washington Subordination Agreement within minutes:

- Make sure to carefully check the form content and its correspondence with general and legal requirements by previewing it or reading its description.

- Search for an alternative official blank if the previously opened one doesn’t match your situation or state regulations (the tab for that is on the top page corner).

- Log in to your account and download the Washington Subordination Agreement in the format you need. If it’s your first experience with our service, click Buy now to continue.

- Register for an account, select your subscription plan, and pay with your credit card or PayPal account.

- Choose in what format you want to save your form and click Download. Print the blank or add it to a professional PDF editor to submit it paper-free.

All documents are drafted for multi-usage, like the Washington Subordination Agreement you see on this page. If you need them one more time, you can fill them out without re-payment - simply open the My Forms tab in your profile and complete your document any time you need it. Try US Legal Forms and accomplish your business and personal paperwork quickly and in total legal compliance!

Form popularity

FAQ

A subordination clause serves to protect the lender if a homeowner defaults. If this happens, the lender then has the legal standing to repossess the home and cover their loan's outstanding balance first. If other subordinate mortgages are involved, the secondary liens will take a backseat in this process.

The lender may require a subordination agreement to protect its interests in the event that the borrower deposits additional liens on the property, such as if the borrower were to take out a second mortgage.

A subordination agreement prioritizes debts, ranking one behind another for purposes of collecting repayment from a debtor in the event of foreclosure or bankruptcy. A second-in-line creditor collects only when and if the priority creditor has been fully paid.

A Subordination Agreement focuses on creditor priorities and security claims, providing legal certainty to creditors when assessing repayment risk. If a credit event (or default) occurs, a subordination agreement provides a senior lender superior repayment rights than the subordinated lender.

Subordination agreements ensure that a primary lender will be paid in the event the borrower takes on more debt. As with most legal documents, subordination agreements need to be notarized in order to be official in the eyes of the law.

Purpose of a Subordination Agreement A subordination agreement is generally used when there are two mortgages and the mortgagor needs to refinance the first mortgage. It acknowledges that one party's interest or claim is superior to another in case the borrower's assets need to be liquidated to repay debts.

The party that primarily benefits from a subordination clause in real estate is the lender. However, if you decide to pursue a second mortgage, then the subordination clause prioritizes the first lender's repayment and contract rights. The most common application of subordination clauses is when refinancing a property.

- A subordination agreement is an agreement between two lien holders to modify the order of lien priority.