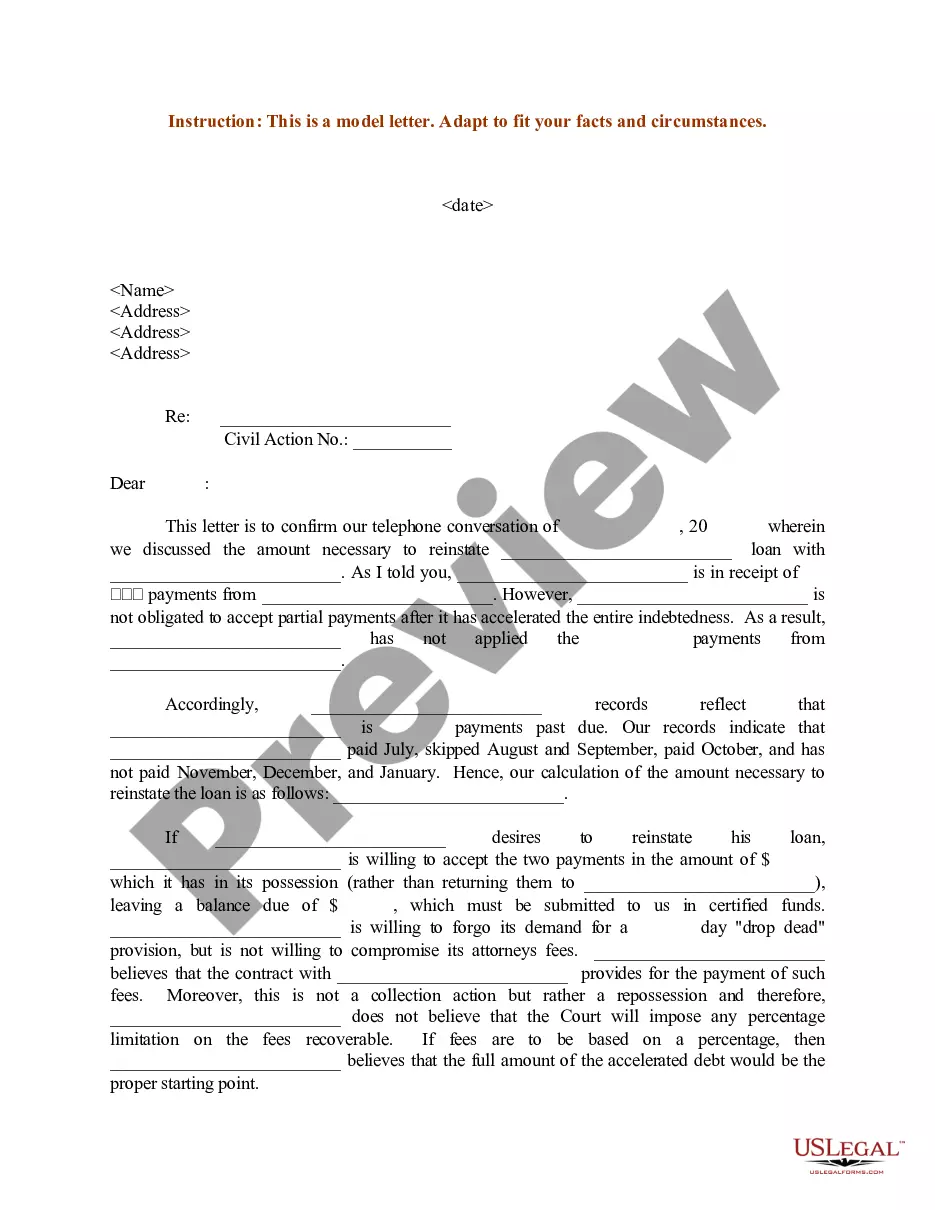

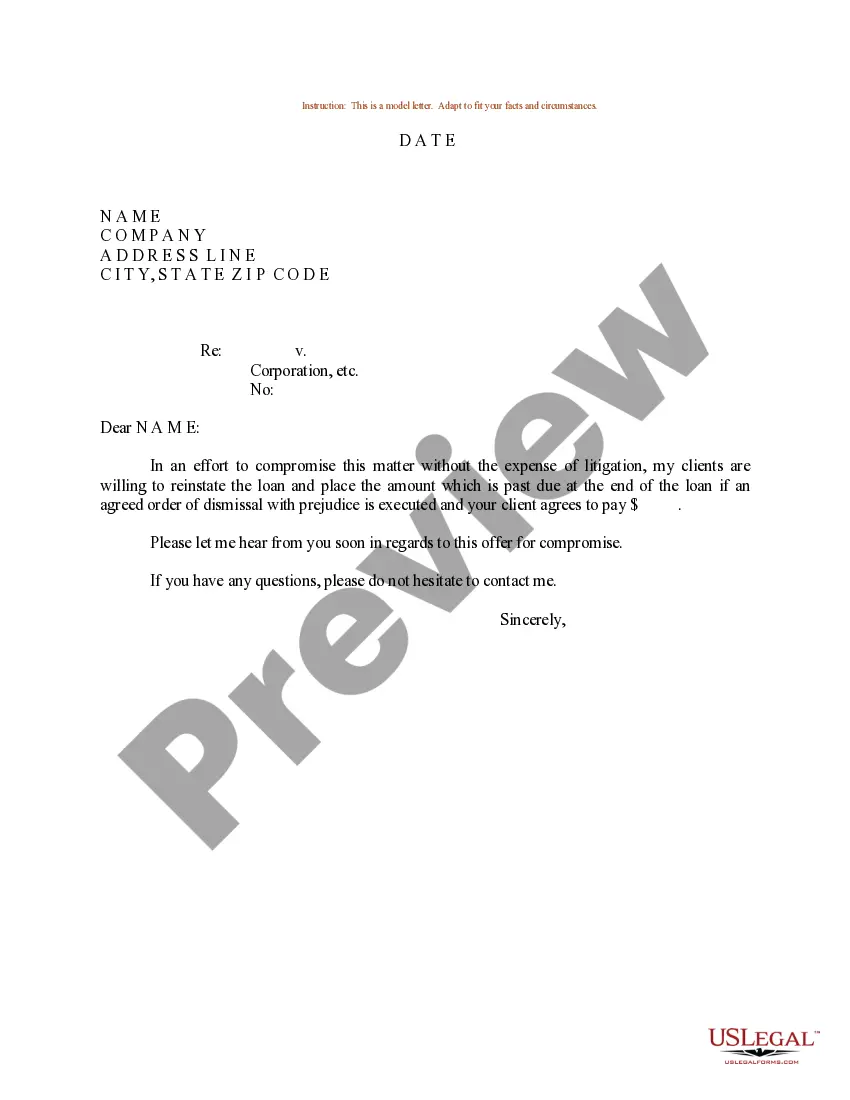

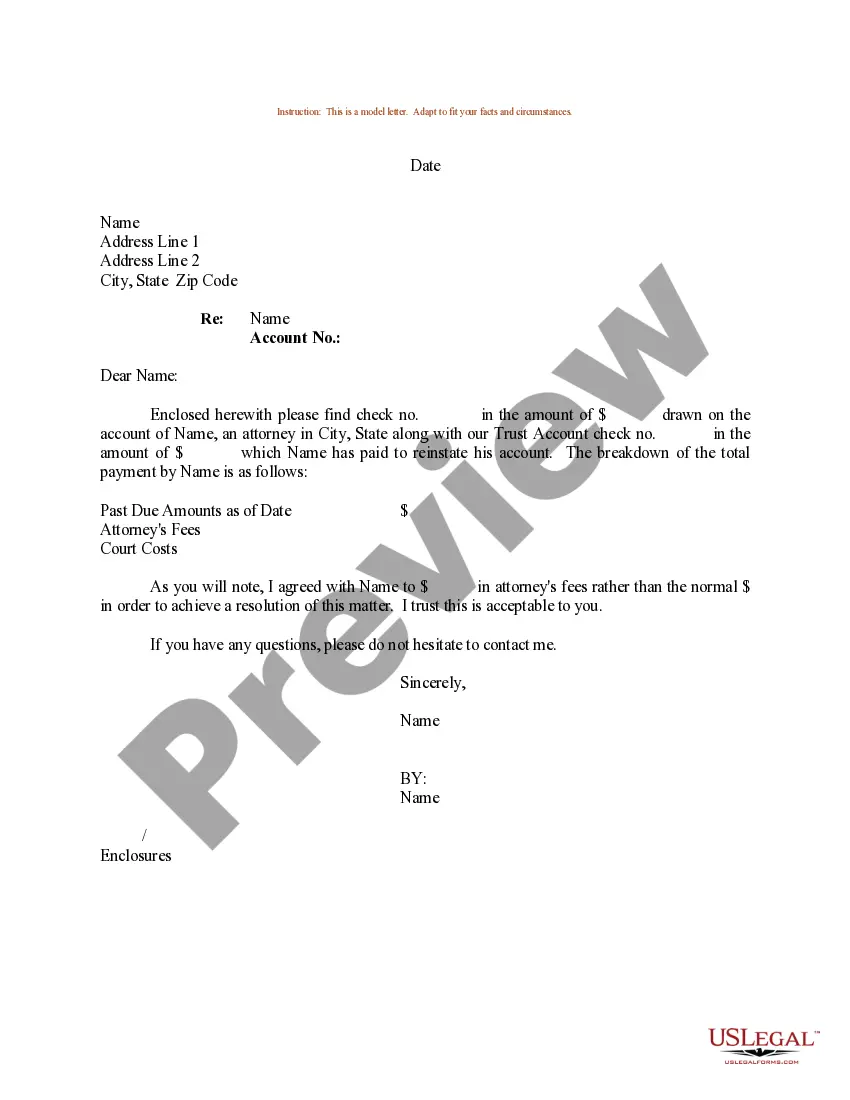

Vermont Sample Letter for Insufficient Amount to Reinstate Loan

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Sample Letter For Insufficient Amount To Reinstate Loan?

US Legal Forms - one of the largest collections of legal documents in the USA - provides a selection of legal form templates you can download or create.

By utilizing the website, you will access thousands of forms for business and personal purposes, sorted by categories, states, or keywords.

You can find the latest versions of forms such as the Vermont Sample Letter for Insufficient Amount to Reinstate Loan in moments.

If the form doesn’t meet your needs, use the Search area at the top of the screen to find the one that does.

Once you are satisfied with the form, confirm your choice by clicking the Get now button. Then, select your preferred pricing plan and provide your details to register for an account.

- If you already have a subscription, Log In and download the Vermont Sample Letter for Insufficient Amount to Reinstate Loan from the US Legal Forms library.

- The Download button will appear on every form you view.

- You can access all previously saved forms from the My documents tab of your account.

- If you wish to use US Legal Forms for the first time, here are simple instructions to get started.

- Ensure you have selected the correct form for the city/state. Click on the Preview button to check the form's content.

- Check the form summary to confirm you have chosen the right form.

Form popularity

FAQ

An example of a personal hardship could be losing a job unexpectedly, which may strain your finances significantly. This situation often leads to difficulties in making loan payments or meeting other financial commitments. By explaining your personal hardships in a clear manner, you can request leniency from your lender. Incorporating the Vermont Sample Letter for Insufficient Amount to Reinstate Loan can guide you in crafting a compelling narrative.

A general proof of hardship letter serves to inform lenders about your financial difficulties. This letter outlines your current circumstances, such as unexpected medical expenses or job loss. It provides the lender a clear picture of your situation, allowing them to evaluate your request for assistance. Using the Vermont Sample Letter for Insufficient Amount to Reinstate Loan can help you format your letter for clarity and impact.

To write a successful hardship letter, start by clearly explaining your situation. Include details about your financial challenges and emphasize why you cannot meet your loan payments. It’s important to remain honest and straightforward. Utilizing the Vermont Sample Letter for Insufficient Amount to Reinstate Loan, you can structure your message effectively, ensuring it resonates with lenders.

Rule 4.2 of the Florida Rules of Professional Conduct also prohibits communication with a person represented by an attorney in a matter without permission from the lawyer. This rule shares similarities with Vermont's standards and emphasizes the importance of ethical communication in legal situations. As you consider writing a Vermont sample letter for insufficient amount to reinstate loan, being aware of these rules helps ensure that your letter complies with legal standards.

Rule of Evidence 402 in Vermont states that irrelevant evidence is not admissible in court. This rule ensures that only pertinent information is considered in legal proceedings, thus streamlining the judicial process. When drafting a Vermont sample letter for insufficient amount to reinstate loan, focusing on relevant facts is crucial for clarity and effectiveness.

Rule 4.2 in South Carolina, similar to Vermont, restricts communication with a person who is represented in a matter by a lawyer without that lawyer's consent. This rule underscores the need for careful communication in legal dealings. If you are looking for guidance on legal matters, tools like a Vermont sample letter for insufficient amount to reinstate loan can help you structure your communications appropriately.

Rule of Professional Conduct 1.7 in Vermont addresses conflicts of interest between clients. It states that a lawyer cannot represent a client if it creates a conflict with another client's interest without informed consent. This rule is vital for anyone seeking to draft a Vermont sample letter for insufficient amount to reinstate loan, as understanding potential conflicts can steer you in the right direction.

The attorney-client privilege in Vermont protects confidential communications between a client and their attorney for legal advice. This privilege encourages open, honest discussions, allowing clients to reveal sensitive information without fear of disclosure. Knowing this privilege's scope may be helpful if you're getting a Vermont sample letter for insufficient amount to reinstate loan.

Rule of Professional Conduct 4.2 in Vermont prohibits communication with a person who is represented by another lawyer in a matter unless consent is obtained from that lawyer. This rule aims to protect the client’s interests and maintains the integrity of the legal process. Legal professionals often refer to the implications of this rule when advising clients drafting a Vermont sample letter for insufficient amount to reinstate loan.

The judicial code of conduct in Vermont outlines the ethical responsibilities of judges to maintain integrity, impartiality, and independence. This code ensures that judges act in a manner that fosters public confidence in the legal system. Understanding this code can guide those needing to draft a Vermont sample letter for insufficient amount to reinstate loan.