Vermont Surety Agreement

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Surety Agreement?

Are you presently in a circumstance where you need documents for either business or personal purposes on a daily basis.

There are numerous legal document templates available online, but finding ones you can rely on is challenging.

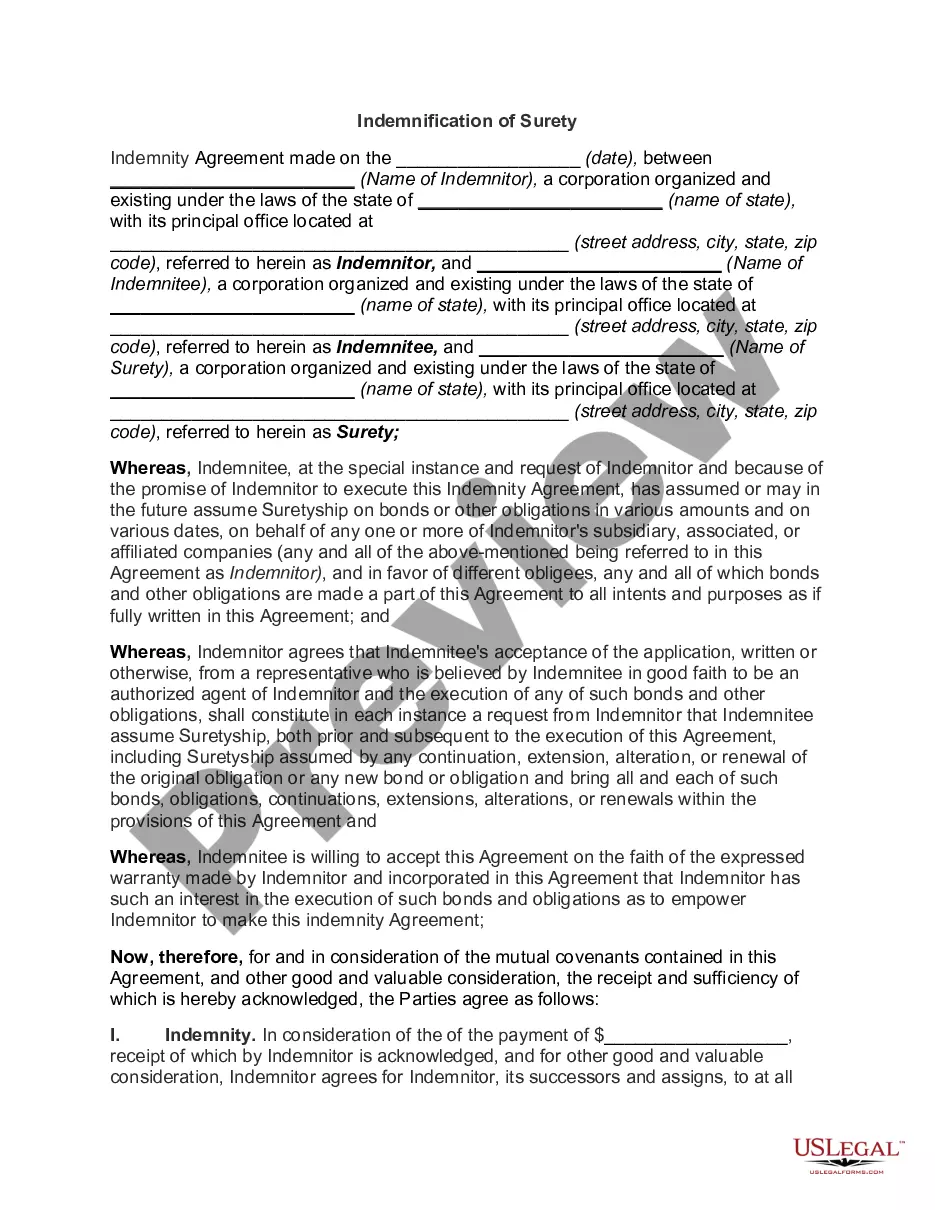

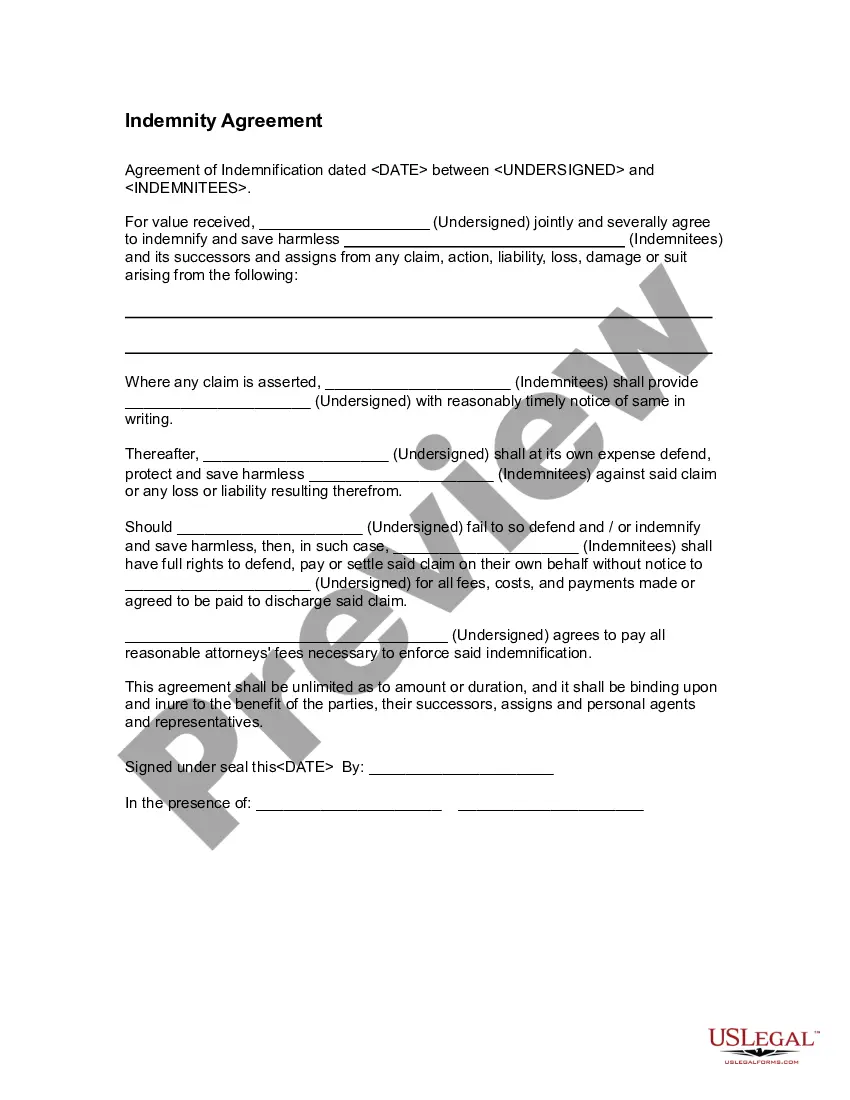

US Legal Forms provides a vast array of form templates, including the Vermont Surety Agreement, created to comply with federal and state regulations.

Once you find the correct form, click Get now.

Choose the payment plan you prefer, provide the required information to create your account, and complete your purchase using PayPal or a credit card.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- After that, you can download the Vermont Surety Agreement template.

- If you do not have an account and wish to start using US Legal Forms, follow these instructions.

- Obtain the form you need and ensure it is for the correct area/state.

- Utilize the Preview button to inspect the form.

- Review the description to confirm you have selected the correct form.

- If the form isn’t what you’re looking for, use the Search section to find the form that meets your needs and specifications.

Form popularity

FAQ

In Mississippi, the maximum surety bond required for a mortgage broker can reach up to $100,000. This bond operates as a Vermont Surety Agreement, providing crucial protection to ensure that mortgage professionals conduct their business ethically. Always verify specific rules and regulations with the Mississippi Department of Banking and Consumer Finance for accurate figures.

In South Carolina, the required surety bond amount for a mortgage lender or broker typically ranges from $25,000 to $50,000, depending on specific licensing requirements. This Vermont Surety Agreement serves as a safeguard for borrowers, ensuring compliance with state regulations. Always consult with local authorities to confirm the exact amount needed for your specific situation.

The relationship between surety and co-surety revolves around shared financial responsibility. A surety offers a guarantee individually, while a co-surety collaborates with others to collectively guarantee an obligation. This cooperative arrangement often mitigates risk for each party involved in a Vermont Surety Agreement, ensuring that the obligation will be fulfilled even if circumstances evolve.

A surety is an individual or entity that takes responsibility for another party's debt or obligation. In contrast, a co-surety shares that responsibility with one or more co-sureties. Each co-surety is jointly liable, which means that if the principal defaults, all parties can be held accountable. Understanding these definitions is crucial when dealing with a Vermont Surety Agreement.

A: Surety bonds provide financial guarantees that contracts and other business deals will be completed according to mutual terms. Surety bonds protect consumers and government entities from fraud and malpractice. When a principal breaks a bond's terms, the harmed party can make a claim on the bond to recover losses.

A surety bond is defined as a three-party agreement that legally binds together a principal who needs the bond, an obligee who requires the bond and a surety company that sells the bond. The bond guarantees the principal will act in accordance with certain laws.

Usually renewal time is one year after purchasing your bond, but depending on the bond type and bond term, your bond might not renew for 2 or 3 years. Some bonds do not renew at all. In some cases, you can get a lower rate for your bond at renewal.

A surety bond is not a typical insurance policy. While the Surety backs the performance of the principal and will pay the penalties resulting from non-performance or under-performance, they do seek to reclaim the funds from the principal. A Surety bond helps make the deal happen.

The three most common types of contract surety bonds are bid bonds, performance bonds, and payment bonds. Bid bonds require that contractors enter into a contract if their bid for a project has been accepted by the obligee.

Someone who assumes direct liability for another's obligation. Financial creditors may require the debtor to find a surety, who then signs the loan agreement along with the debtor.