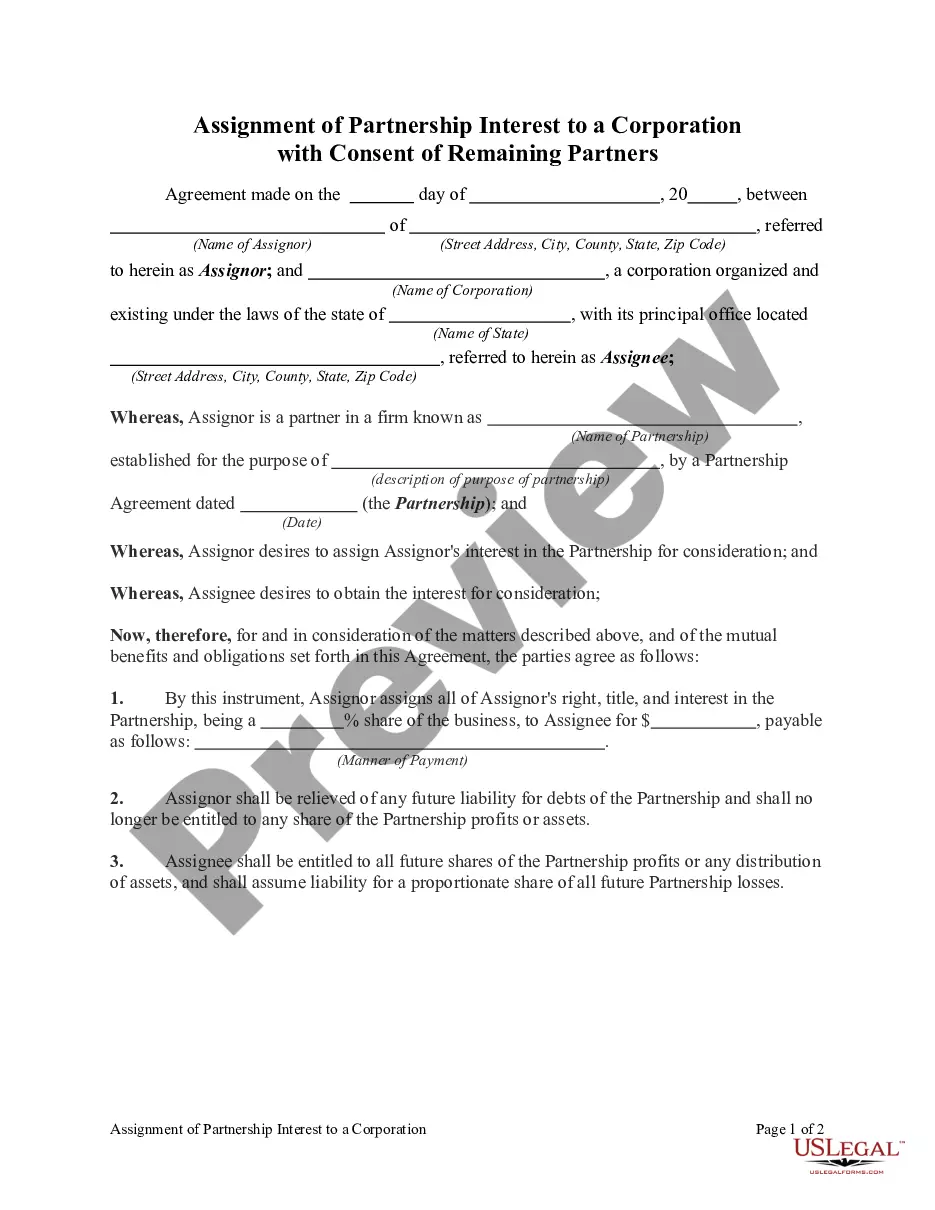

Vermont Assignment of Partnership Interest with Consent of Remaining Partners

Description

How to fill out Assignment Of Partnership Interest With Consent Of Remaining Partners?

Have you ever been in a situation where you require documents for either business or personal reasons nearly every day.

There are numerous legal document templates accessible online, but finding trustworthy ones is not easy.

US Legal Forms offers thousands of document templates, such as the Vermont Assignment of Partnership Interest with Consent of Remaining Partners, designed to comply with state and federal regulations.

Access all the document templates you have purchased in the My documents section. You can obtain another copy of the Vermont Assignment of Partnership Interest with Consent of Remaining Partners at any time, if necessary. Just select the required document to download or print the template.

Utilize US Legal Forms, one of the most extensive collections of legal documents, to save time and avoid errors. The service provides properly crafted legal document templates that you can use for various purposes. Create an account on US Legal Forms and start simplifying your life.

- If you are familiar with the US Legal Forms website and possess an account, simply Log In.

- After logging in, you can retrieve the Vermont Assignment of Partnership Interest with Consent of Remaining Partners template.

- If you do not have an account and wish to start using US Legal Forms, follow these instructions.

- Obtain the document you need and ensure it is suitable for your specific city/region.

- Utilize the Review button to examine the document.

- Check the summary to confirm you have selected the appropriate document.

- If the document does not meet your expectations, use the Search field to find a document that meets your needs.

- Once you find the correct document, click Purchase now.

- Select the payment plan you prefer, provide the required data to create your account, and pay for your order using your PayPal or credit card.

- Choose a convenient file format and download your copy.

Form popularity

FAQ

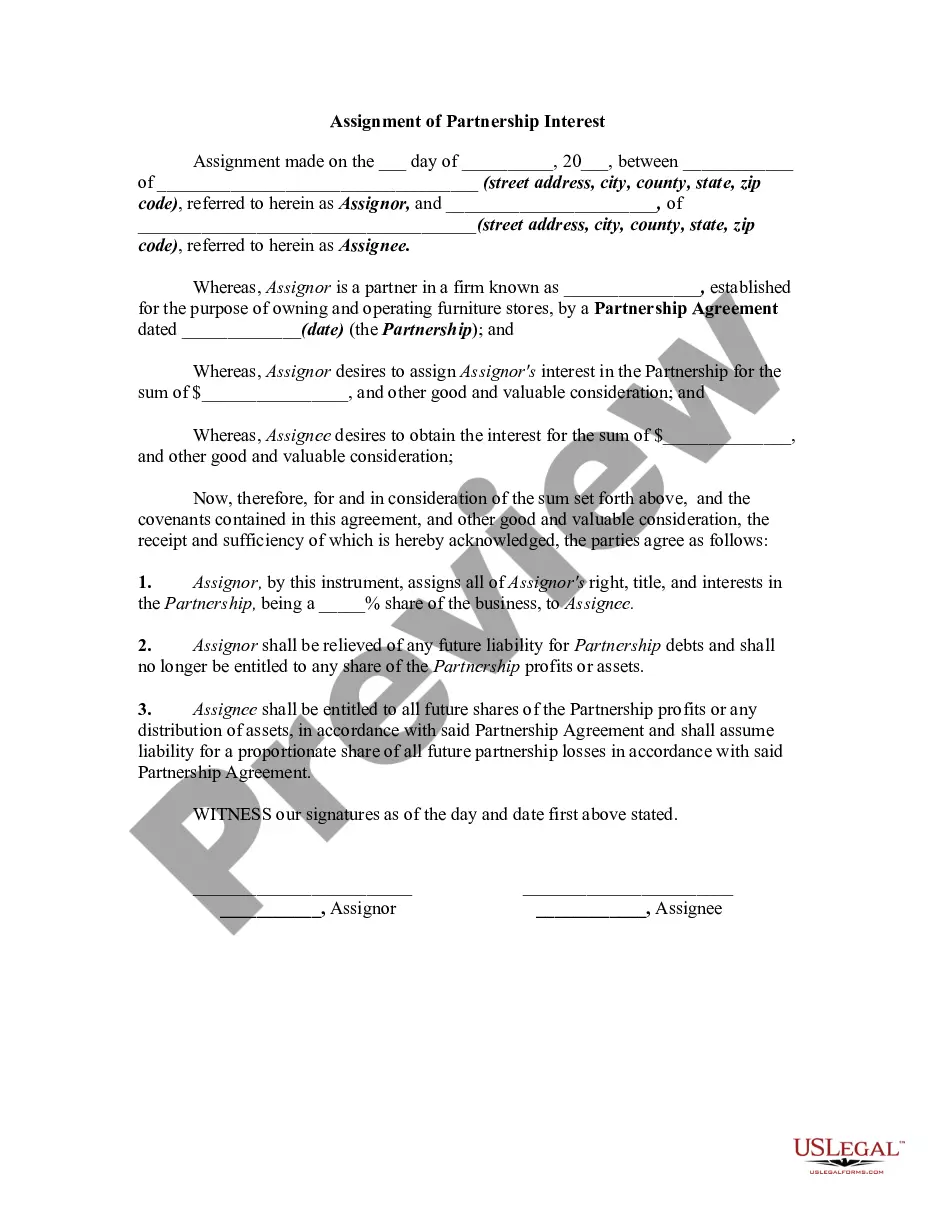

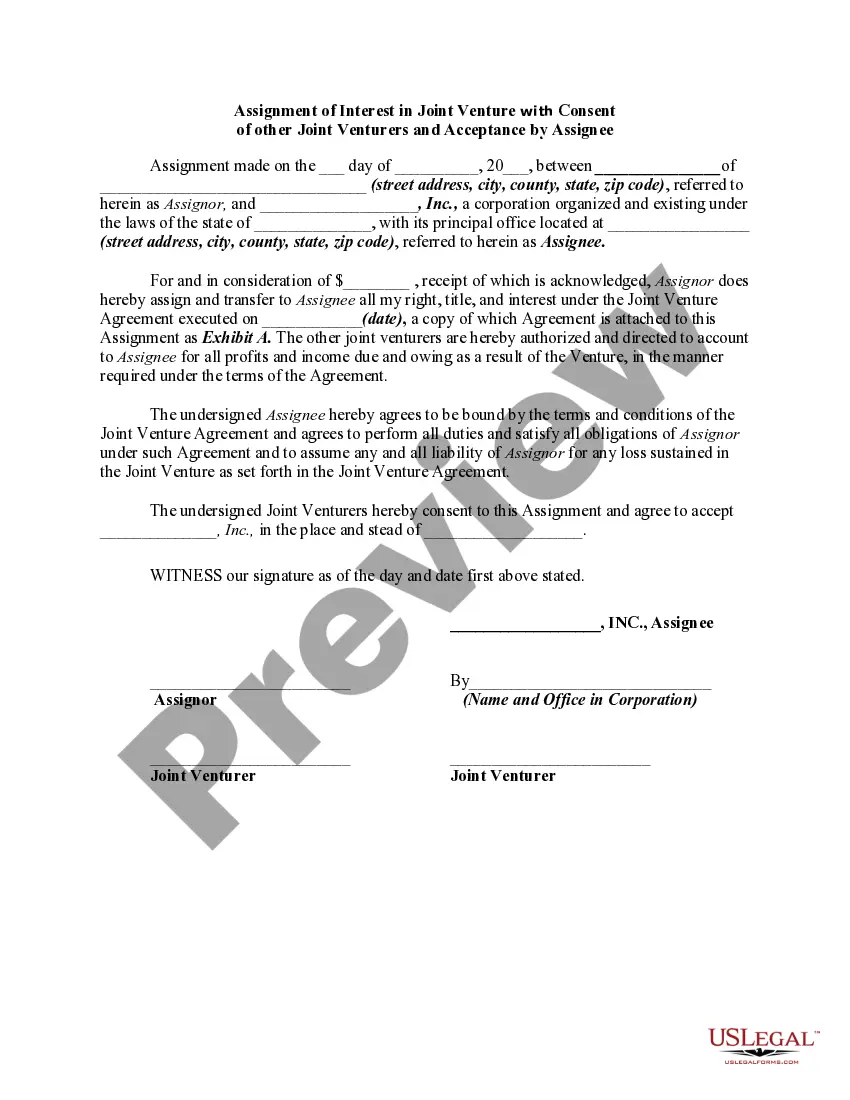

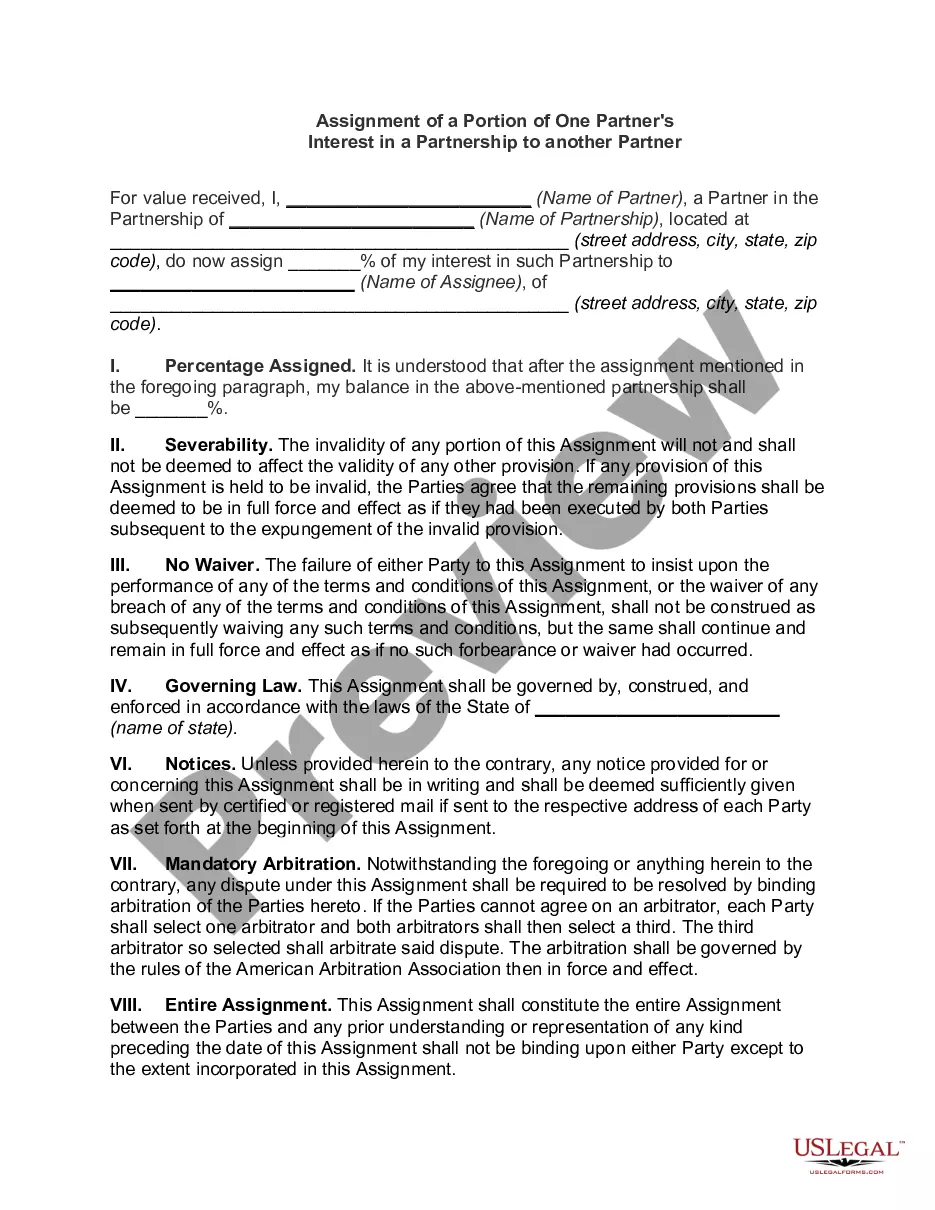

However, the assignee does not become a partner without the consent of the other partners. Without this consent, the assignee is only entitled to receive the assignor's share of the profits of the partnership and the assignor's interest when the partnership dissolves.

Partners are required to mandatorily obtain the consent of all the partners in case the partner is willing to transfer his/her rights and interest to another person. The partners have to work within his/her assigned authority.

Limited partners cannot incur obligations on behalf of the partnership, participate in daily operations, or manage the operation. Because limited partners do not manage the business, they are not personally liable for the partnership's debts.

(a) A limited partner's interest in the partnership is personal property and is assignable. (b) A substituted limited partner is a person admitted to all the rights of a limited partner who has died or has assigned his interest in a partnership.

In a General Partnership, all partners are financially obligated to any debts incurred by the partnership. When a partner leaves, the partnership dissolves and the partners equally split debts and assets.

The gift of a partnership interest generally does not result in the recognition of gain or loss by the donor or the donee. A gift is, however, subject to gift tax unless the gift qualifies for the annual gift tax exclusion or reduces the donor's lifetime gift tax applicable exclusion amount.

Transfer of limited partnership interest is allowed as long as the general partner consents to the arrangement and it is done in concert with the established partnership agreement. A common example of a limited partnership is the family limited partnership, which is often created to administer a family business.

No partner is entitled to remuneration for acting in the partnership business, except that a surviving partner is entitled to reasonable compensation for his services in winding up the partnership affairs. No person can become a member of a partnership without the consent of all the partners.

An Assignment of Partnership Interest occurs when a partner sells their stake in a partnership to a third party. The assignment document records the details of the transfer to the new partner.