Virgin Islands Split-Dollar Life Insurance

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Split-Dollar Life Insurance?

If you wish to full, obtain, or print authorized papers templates, use US Legal Forms, the greatest collection of authorized kinds, which can be found on the web. Make use of the site`s simple and practical search to discover the documents you need. A variety of templates for organization and individual uses are sorted by categories and states, or keywords. Use US Legal Forms to discover the Virgin Islands Split-Dollar Life Insurance within a number of click throughs.

When you are already a US Legal Forms consumer, log in in your account and click the Obtain switch to have the Virgin Islands Split-Dollar Life Insurance. Also you can access kinds you in the past downloaded within the My Forms tab of your own account.

Should you use US Legal Forms initially, refer to the instructions beneath:

- Step 1. Be sure you have selected the shape for that proper area/country.

- Step 2. Use the Preview solution to examine the form`s content material. Don`t forget to read the description.

- Step 3. When you are unhappy with all the kind, utilize the Look for discipline towards the top of the screen to find other versions of your authorized kind format.

- Step 4. After you have found the shape you need, click on the Get now switch. Select the rates program you choose and add your accreditations to sign up for the account.

- Step 5. Process the purchase. You can utilize your credit card or PayPal account to perform the purchase.

- Step 6. Choose the file format of your authorized kind and obtain it on your system.

- Step 7. Total, change and print or indication the Virgin Islands Split-Dollar Life Insurance.

Every single authorized papers format you purchase is your own property forever. You might have acces to each and every kind you downloaded in your acccount. Click on the My Forms segment and select a kind to print or obtain once more.

Compete and obtain, and print the Virgin Islands Split-Dollar Life Insurance with US Legal Forms. There are many specialist and state-particular kinds you can utilize for your organization or individual requirements.

Form popularity

FAQ

Yes, you can designate multiple beneficiaries when you purchase your life insurance policy. When doing so, you will assign each beneficiary a percentage of the death benefit. For example, you could name your two children as equal beneficiaries with 50% allocated to each.

Answer: Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren't includable in gross income and you don't have to report them. However, any interest you receive is taxable and you should report it as interest received.

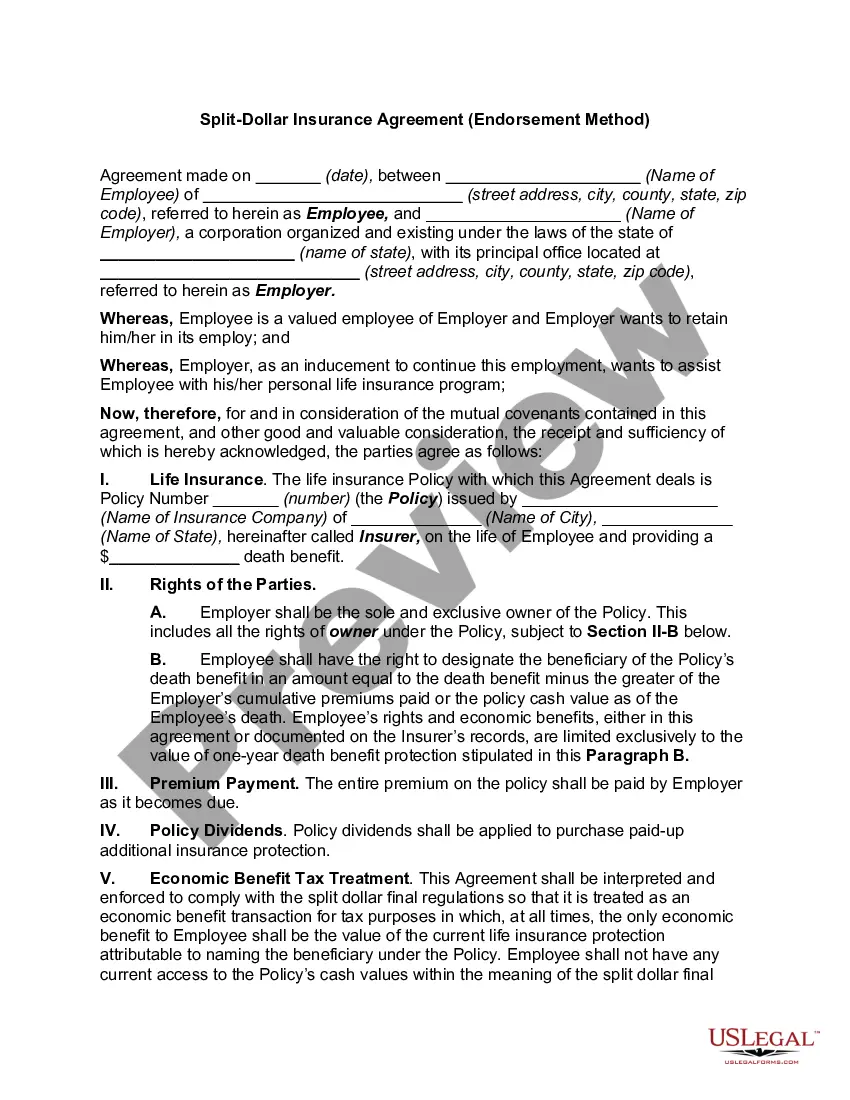

If the employer is the owner of the split-dollar policy, the employer's premium payments are treated as providing taxable economic benefits to the executive. The economic benefits include the executive's interest in the policy's accessible cash value and current life insurance protection.

There is no cost to the employee-participant unless the policy is transferred to them. This endorsement split-dollar plan is most often used to provide a low-cost death benefit to the employee-participant as a fringe benefit or where the employer wishes to own the policy and/or obtain key person protection.

Life insurance policy ownership and beneficiary designation Creating a split-dollar life insurance arrangement requires agreement on which party will own the policy and which will be designated as a beneficiary, in full or in part. These types of policies are available as either employer-owned or employee-owned.

Most often, the premiums are paid by the employer, and the benefits are split between the employer and the family of the deceased.

While split-dollar life insurance arrangements offer numerous advantages, they also come with potential drawbacks, such as complexity, tax considerations, and limited availability. Both employers and employees must carefully weigh the benefits and disadvantages of this type of arrangement before deciding to pursue it.

In collateral assignment split dollar, the policy in the split dollar plan is owned by the insured. In return for its payment of premiums, the insured policyowner assigns the policy to the employer as collateral.

Depending on the insurer, a life insurance payout can typically be distributed in three ways: in the form of a lump sum, via a life insurance annuity, or through a retained asset account. Check with the insurer to see which life insurance payout options they offer.

Split-dollar insurance plans: In an economic benefit arrangement, the employer owns the policy, covers the premiums, and has the authority to grant the rights and benefits. For example, an employer may permit the employee to name their beneficiaries, ensuring that the employee control who receives their death benefits.