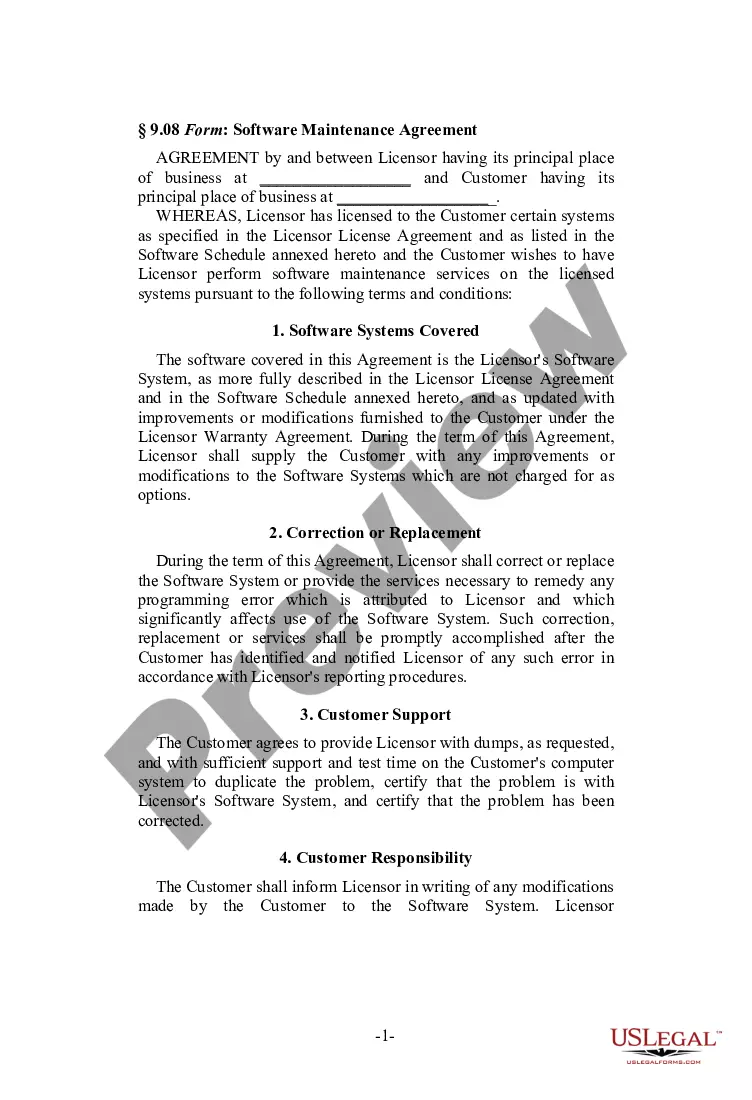

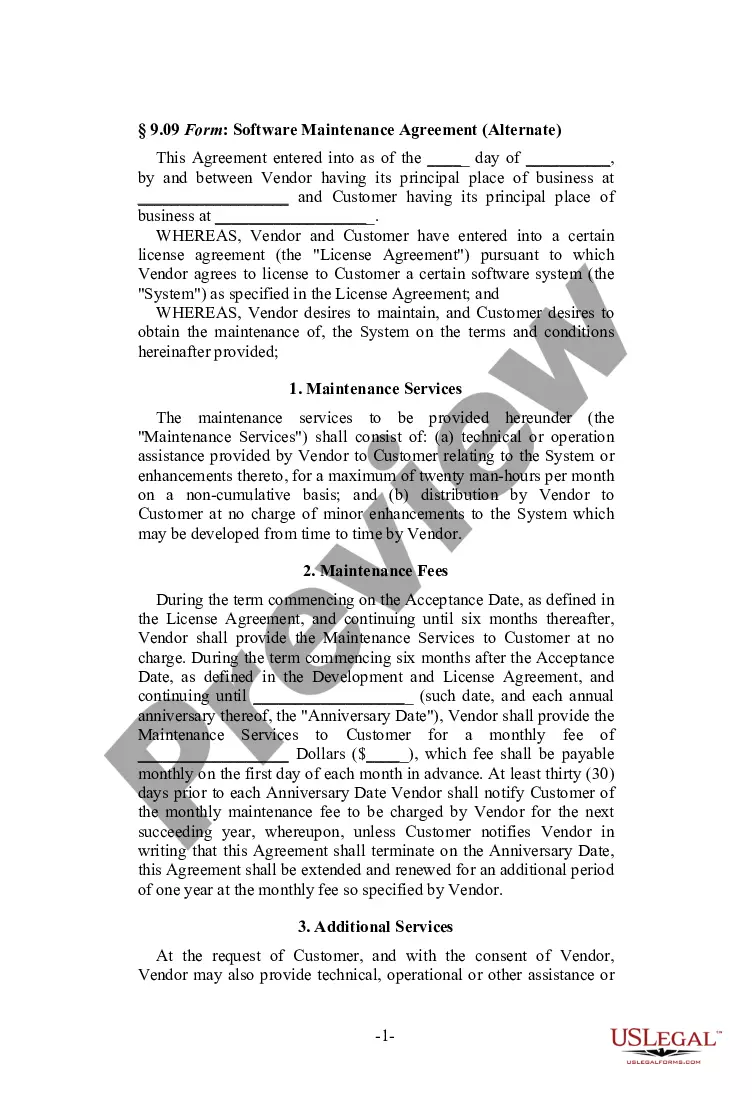

Virginia Software Maintenance Agreement (Alternate)

Description

")

")

")

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Software Maintenance Agreement (Alternate)?

You might spend hours online attempting to locate the legal document template that meets the state and federal criteria you desire.

US Legal Forms provides a vast array of legal documents that are reviewed by experts.

You can download or print the Virginia Software Maintenance Agreement (Alternate) from the service.

To locate another version of the form, utilize the Search field to find the template that suits your needs and preferences.

- If you already have a US Legal Forms account, you can Log In and click on the Download button.

- After that, you can complete, modify, print, or sign the Virginia Software Maintenance Agreement (Alternate).

- Every legal document template you obtain is yours permanently.

- To get another copy of any purchased form, visit the My documents tab and click on the appropriate button.

- If you are using the US Legal Forms website for the first time, follow the simple guidelines below.

- First, ensure you have chosen the correct document template for the county/city of your selection.

- Review the form description to confirm you have selected the right form.

Form popularity

FAQ

To exit a service agreement, you should carefully review the termination clauses within the contract. Most agreements outline specific conditions or notice periods for termination. If you find the terms confusing or need further assistance, consider using the resources available on uslegalforms to help you navigate a Virginia Software Maintenance Agreement (Alternate) smoothly.

A software maintenance agreement, or SMA, is a legal contract that obligates the software vendor to provide technical support and updates for an existing software product for their customers. It may also extend the expiration date of certain features, such as new releases or upgrades.

Optional maintenance contracts provide prepaid coverage for maintaining a vehicle. These contracts include taxable items and nontaxable repair labor for one price. Examples include: Oil changes.

The Virginia Department of Revenue has maintained a long-standing policy, which is referenced in Virginia Public Document Ruling No. 05-44 , that sales of software delivered electronically do not constitute the sale of tangible personal property and are not subject to sales tax.

The sale of an extended warranty which provides for the provision of labor only may be purchased exempt of the sales and use tax, because such sales are considered nontaxable sales of services in Virginia.

In the state of Virginia, any maintenance contracts that provide only repair labor are considered to be exempt. Any contracts that provide both parts and labor are definitely subject to tax on one-half the total charge for the contract. Contracts which provide only parts are considered to be taxable.

Fees for engineering services to produce an original or master plan and specifications for a particular project are not taxable. However, charges for additional copies of such plans and specifications are subject to the retail sales and use tax.

Charges for services generally are exempt from the retail sales and use tax. However, services provided in connection with sales of tangible personal property are taxable.

The Taxpayer is correct that the sale of software delivered electronically to customers does not constitute the sale of tangible personal property and is generally not subject to Virginia sales and use taxation.

Yes. Retail sales tax applies to a service contract or warranty sold to a consumer (WAC 458-20-257).