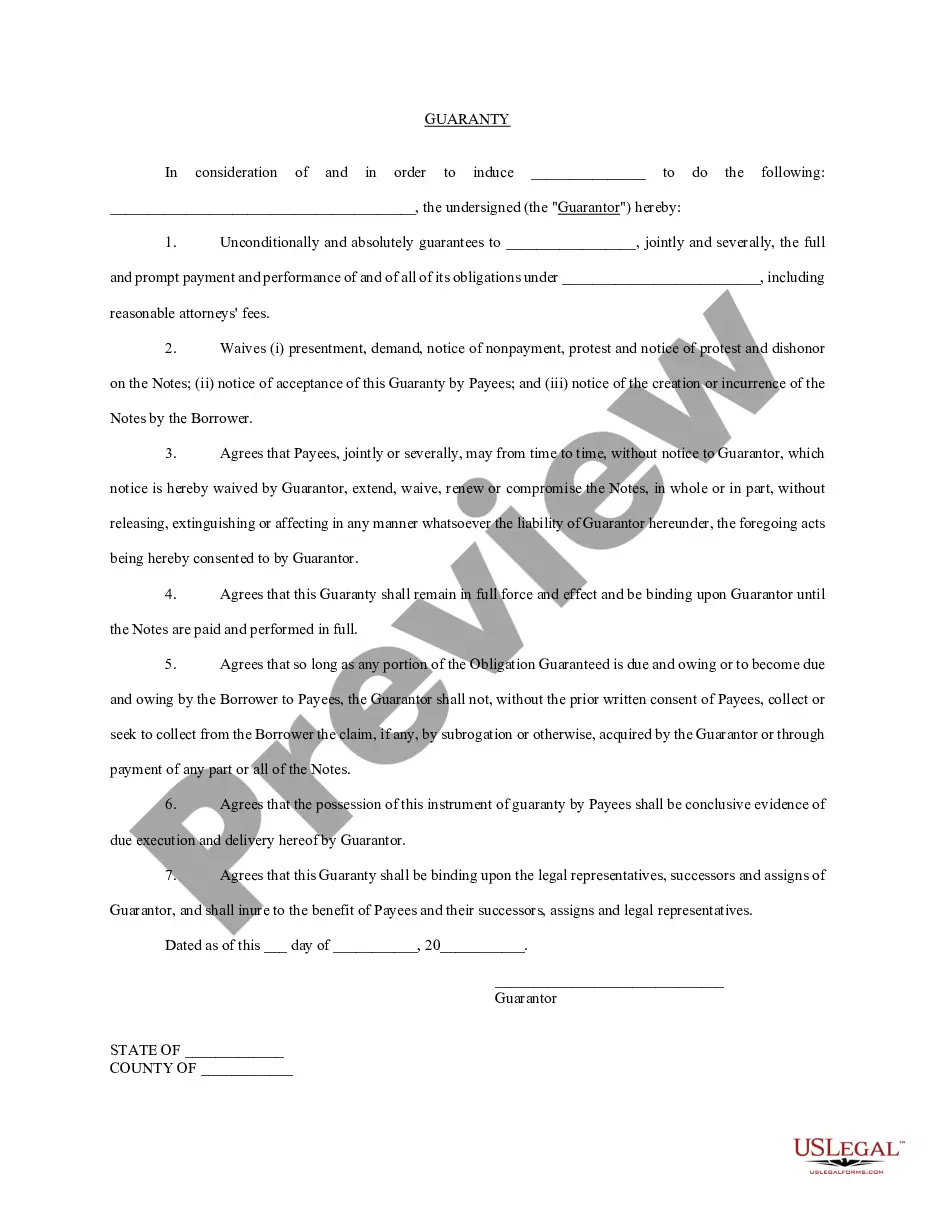

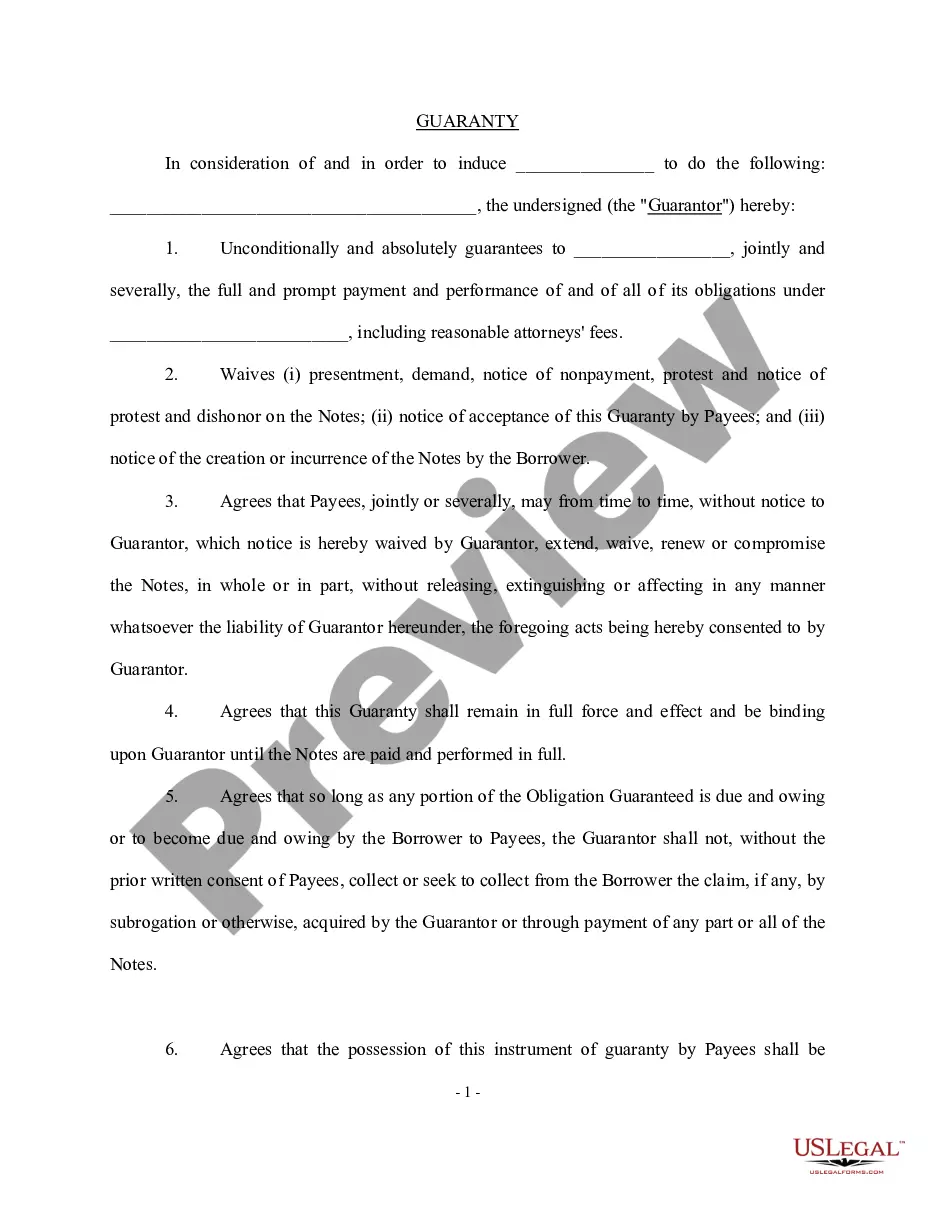

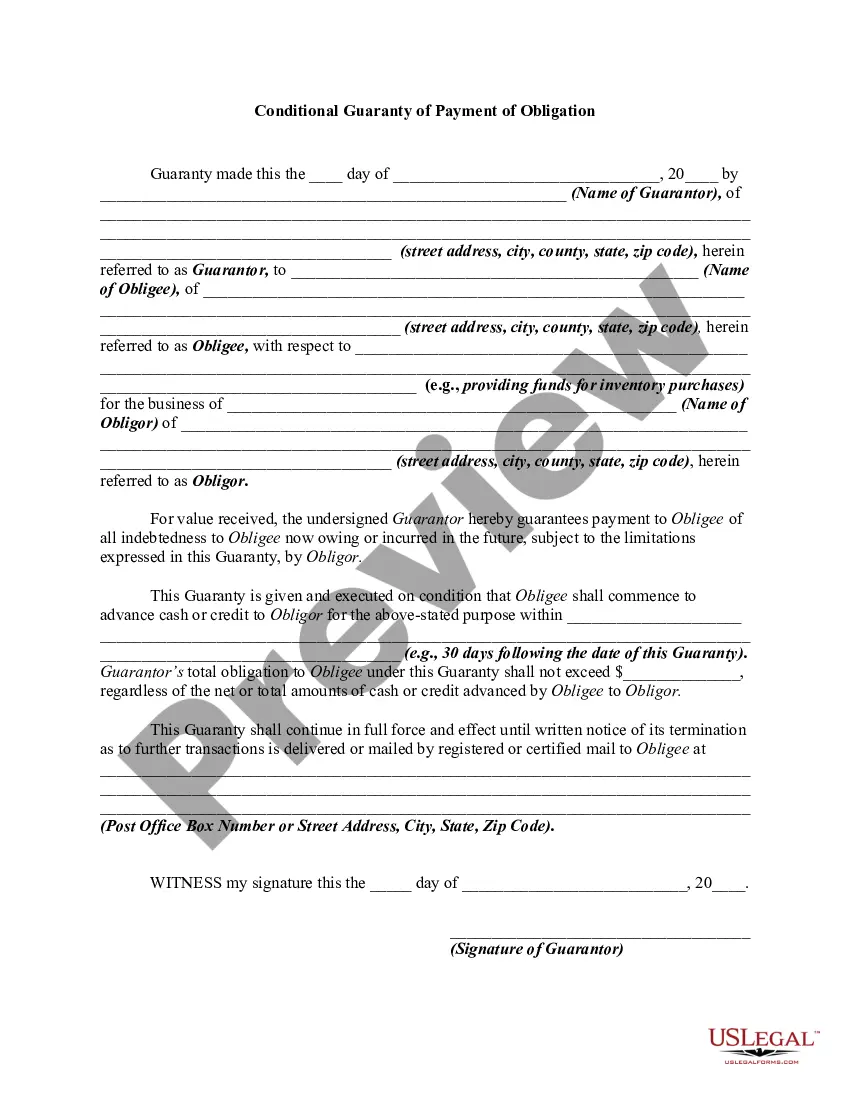

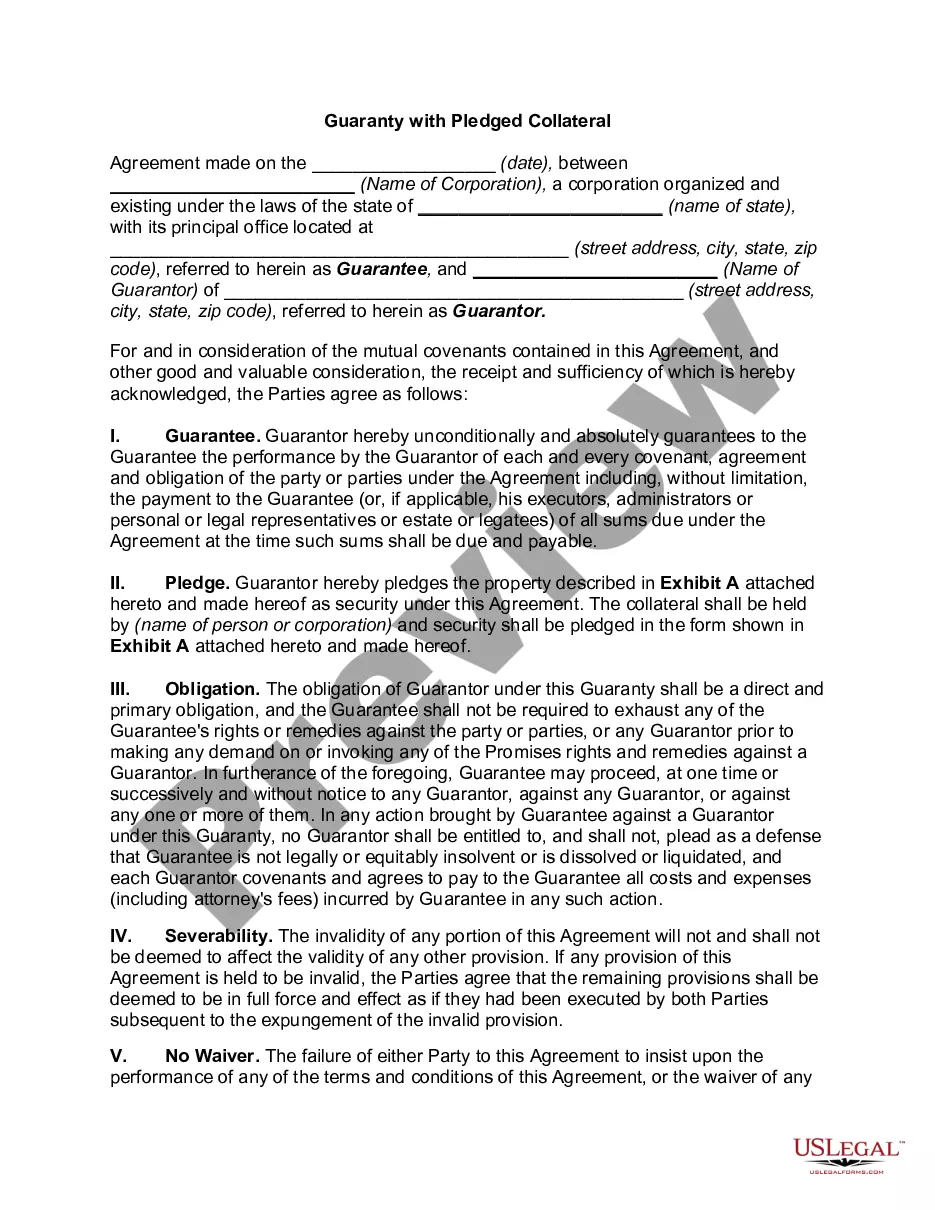

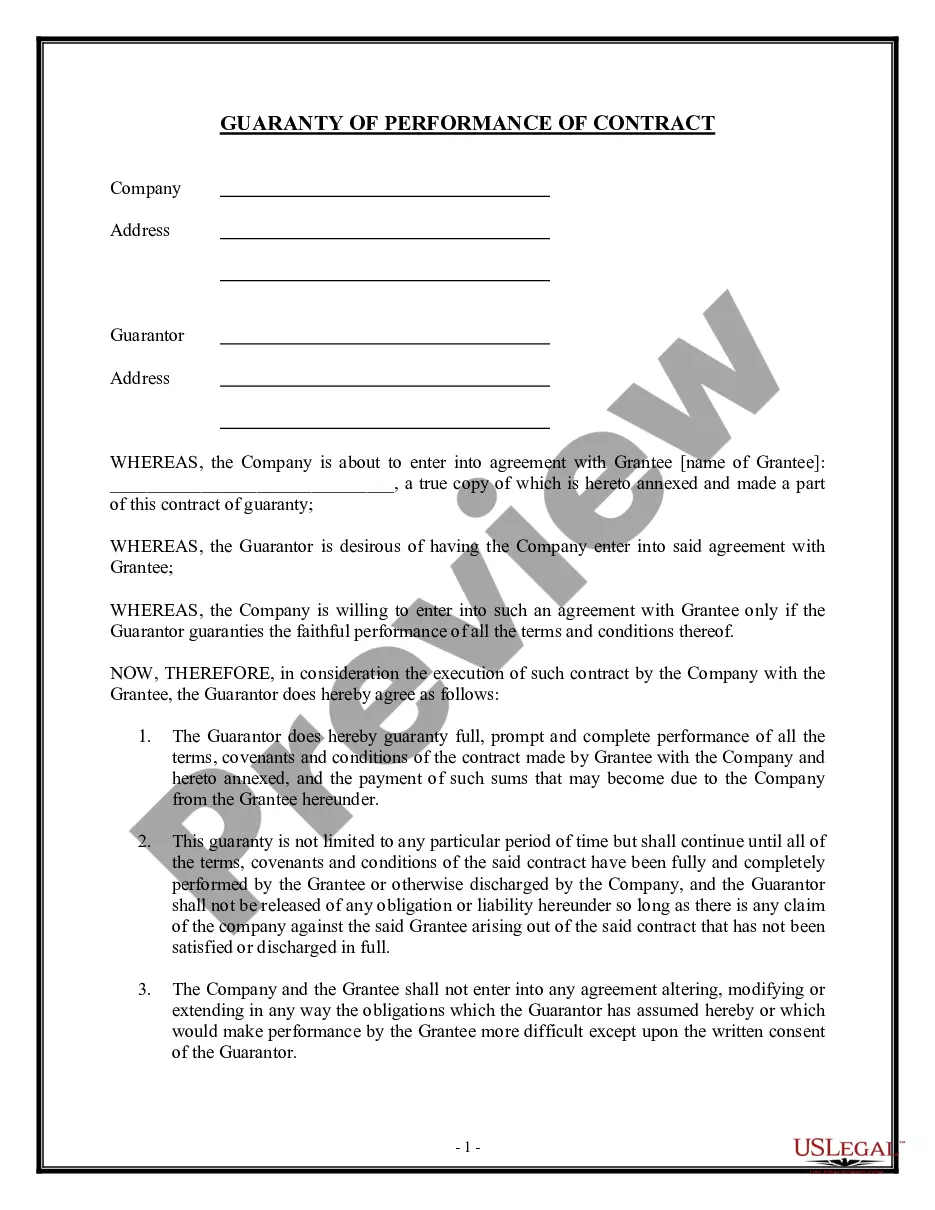

A guaranty is a contract under which one person agrees to pay a debt or perform a duty if the other person who is bound to pay the debt or perform the duty fails to do so. A guaranty of the payment of a debt is different from a guaranty of the collection of the debt. A guaranty of payment is absolute while a guaranty of collection is conditional.

Virginia Guaranty of Collection of Promissory Note

Instant download

Description

How to fill out Guaranty Of Collection Of Promissory Note?

If you wish to finalize, acquire, or generate legal document templates, utilize US Legal Forms, the premier collection of legal documents available online.

Employ the site's straightforward and convenient search feature to locate the paperwork you require.

Various templates tailored for business and personal purposes are sorted by categories and states, or keywords.

Step 4. After you have located the form you need, click the Get now button. Choose the pricing plan you prefer and enter your details to register for an account.

Step 5. Complete the transaction. You can use your credit card or PayPal account to finalize the payment.

- Use US Legal Forms to locate the Virginia Guaranty of Collection of Promissory Note with just a few clicks.

- If you are currently a US Legal Forms user, Log In to your account and click the Download button to obtain the Virginia Guaranty of Collection of Promissory Note.

- You can also access forms you previously downloaded in the My documents tab of your account.

- If you are using US Legal Forms for the first time, follow the instructions below.

- Step 1. Ensure you have chosen the form for your correct city/state.

- Step 2. Use the Preview option to review the form's details. Be sure to read the description.

- Step 3. If you are not satisfied with the form, use the Search section at the top of the screen to find alternate versions of the legal form template.

Form popularity

FAQ

Filling out a promissory note requires attention to detail. Start with the date, followed by the names of the lender and borrower, then state the amount and any interest rates. Ensure you highlight that the note adheres to the Virginia Guaranty of Collection of Promissory Note, ensuring your agreement is legally sound.

Filling out a promissory demand note involves entering the principal amount, the names of both parties, and clearly stating that the repayment is required upon demand. Ensure to include any interest rates applicable and the date of signing. This clear format aligns with the principles of the Virginia Guaranty of Collection of Promissory Note, protecting both parties involved.

A typical promissory note format includes the title, the date, the principal amount, and the names of the borrower and lender. It should clearly outline the repayment terms, such as interest rates and due dates. Additionally, including a section on the Virginia Guaranty of Collection of Promissory Note adds an extra layer of security to your financial transaction.

The guaranty of payment or collection refers to a promise that the lender will receive payment as agreed. This legal assurance provides security for the lender, knowing they have recourse if the borrower defaults. In Virginia, understanding the guaranty of collection of promissory notes can bolster your financial agreements, ensuring clarity and protection.

Yes, a promissory note serves as the primary evidence of a debt. It formally records the borrower's commitment to repay the borrowed amount under specified terms. In the context of a Virginia Guaranty of Collection of Promissory Note, this document plays a critical role in legal proceedings, serving as proof of the debt's existence and the conditions attached to it. Therefore, having a clear and valid promissory note is essential for both lenders and borrowers in managing financial obligations.

The guarantee of a promissory note refers to the assurance provided by a guarantor that they will fulfill the payment obligations if the borrower defaults. In a Virginia Guaranty of Collection of Promissory Note, this assurance takes a specific form, outlining the steps the lender must take before turning to the guarantor. This guarantee enhances the lender's security, creating a clear pathway for recourse if needed. Consequently, it is a vital aspect for lenders considering risk management.

The Virginia Guaranty of Collection of Promissory Note primarily differs from a guaranty of payment in that it focuses on the obligation to collect the debt rather than ensuring payment is made. A guaranty of collection protects the lender by stipulating that the lender must first attempt to collect from the borrower before seeking payment from the guarantor. This distinction is crucial for understanding responsibilities in the event of default. Thus, the lender has to exhaust collection efforts on the principal debtor before pursuing the guarantor.

The guaranty of recourse obligations refers to a situation where a guarantor is responsible for fulfilling the borrower's obligations if they fail to do so. This means the lender can pursue the guarantor for payment. Incorporating concepts like the Virginia Guaranty of Collection of Promissory Note can help clarify such responsibilities, ensuring that all parties are aware of their duties and rights.

The rules for promissory notes typically include requirements for clarity and legal compliance. For instance, the note must clearly identify all parties, the amount borrowed, interest terms, and the repayment schedule. Additionally, understanding the Virginia Guaranty of Collection of Promissory Note can guide you in creating a legally sound document that protects all parties involved.

A guaranty of collection is a commitment where a guarantor agrees to ensure payment is collected if the borrower defaults. This type of guaranty protects lenders by providing an extra level of security. By integrating the Virginia Guaranty of Collection of Promissory Note into your agreements, you can enhance the security and enforceability of your financial arrangements.